Final Expense vs Burial Insurance: What’s the Difference?

Posted in Types of Life Insurance on November 26, 2025 last updated on November 26, 2025

Posted in Types of Life Insurance on November 26, 2025 last updated on November 26, 2025

If you’re shopping for life insurance to cover your funeral and final expenses, you’ve probably encountered two terms: “final expense insurance” and “burial insurance.” At first glance, they seem different—but are they really? Understanding final expense insurance vs burial insurance is crucial to making the right decision for your family’s financial protection. Before diving into the comparison, it’s important to understand how much life insurance seniors actually need to cover all end-of-life expenses

Here’s the truth: most insurance agents and companies use these terms interchangeably. The difference between final expense and burial insurance is more about marketing language than actual policy differences. However, there ARE important distinctions in how these policies are structured, what they cover, and how much they cost that every senior should understand.

In this comprehensive guide, I’ll explain everything you need to know about final expense vs burial life insurance, break down the subtle differences that do exist, compare actual costs, and help you determine which type of coverage is right for your specific situation. Whether you’re 60 or 85, in perfect health or managing chronic conditions, you’ll learn exactly what you’re buying and how to get the best value.

If you’re specifically concerned about qualifying for coverage with health conditions, you might also want to review our guides on life insurance for seniors with diabetes, heart disease, or other common health conditions that can affect your options.

Let’s clear up the confusion about burial insurance vs final expense insurance once and for all, so you can make an informed decision that protects your family without overpaying.

What Is Final Expense Insurance?

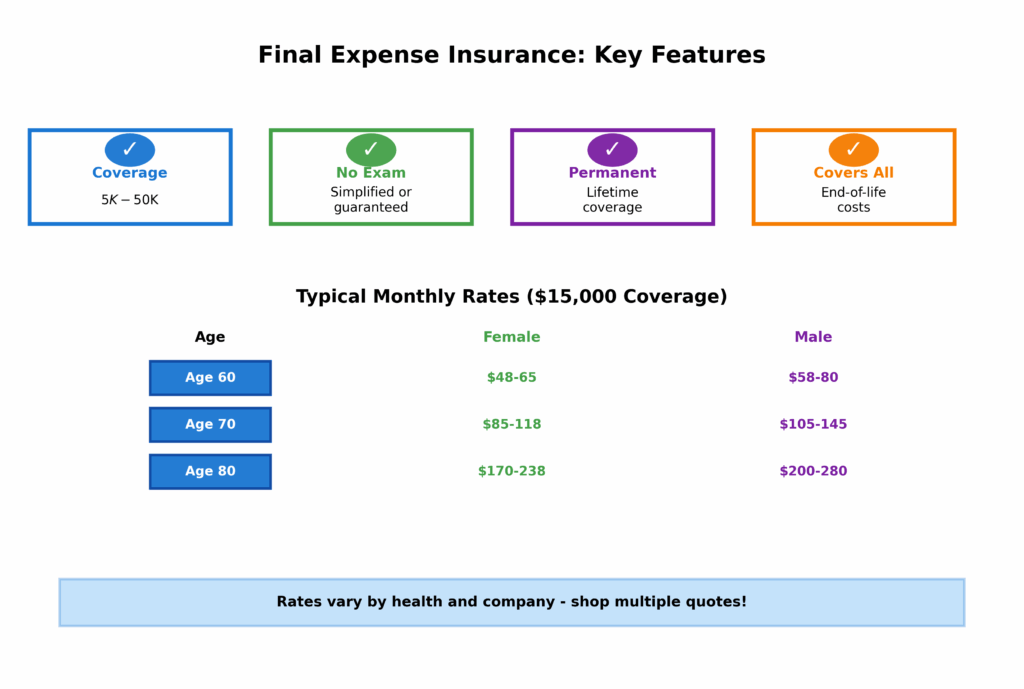

Final expense insurance (also called “final expense life insurance” or “funeral insurance”) is a type of permanent life insurance specifically designed to cover end-of-life costs. These policies are marketed to seniors aged 50-85 who want to ensure their family isn’t burdened with funeral expenses and final bills.

Key Features of Final Expense Insurance:

Coverage Amounts:

- Typically $5,000 to $50,000

- Most common purchase: $10,000-$25,000

- Some companies offer up to $75,000

- Simplified issue policies (health questions only)

- Guaranteed issue policies (no health questions at all)

- Faster approval process

Permanent Coverage:

- Lasts your entire life (doesn’t expire)

- Premiums never increase

- Builds small cash value over time

What Final Expense Insurance Covers:

- Funeral service costs ($2,000-$5,000)

- Burial or cremation ($2,000-$10,000)

- Casket or urn ($1,000-$10,000)

- Cemetery plot and headstone ($2,000-$6,000)

- Final medical bills not covered by insurance

- Outstanding credit card debt or small loans

- Probate and estate settlement costs

- Transportation and travel expenses for family

- Any remaining balance goes to beneficiaries

Typical Applicant: A 70-year-old senior who wants $15,000-$20,000 coverage to handle funeral costs, final medical bills, and avoid burdening adult children with expenses. They may have health conditions that prevent traditional life insurance approval.

Real Final Expense Insurance Rates

Let’s look at actual monthly premiums for final expense insurance:

$15,000 Coverage – Female Non-Smoker:

- Age 60: $45-$65/month

- Age 65: $60-$85/month

- Age 70: $80-$115/month

- Age 75: $115-$165/month

- Age 80: $165-$235/month

$15,000 Coverage – Male Non-Smoker:

- Age 60: $55-$80/month

- Age 65: $75-$105/month

- Age 70: $100-$140/month

- Age 75: $140-$195/month

- Age 80: $195-$275/month

$25,000 Coverage – Female Non-Smoker:

- Age 60: $75-$105/month

- Age 65: $95-$140/month

- Age 70: $130-$185/month

- Age 75: $185-$265/month

- Age 80: $265-$375/month

Rates vary based on health status, smoking status, and insurance company. Guaranteed issue policies typically cost 30-50% more than simplified issue.

What Is Burial Insurance?

Burial insurance (also called “burial life insurance” or “funeral insurance”) is essentially the same product as final expense insurance, but with a name that emphasizes its primary purpose: covering burial and funeral costs. When comparing final expense insurance vs burial insurance, you’ll find they’re structured identically.

Key Features of Burial Insurance:

Coverage Amounts:

- Typically $5,000 to $35,000

- Most common purchase: $10,000-$15,000

- Marketed specifically for funeral/burial costs

No Medical Exam Required:

- Same underwriting as final expense insurance

- Simplified or guaranteed issue options

- Quick approval (often 24-48 hours)

Permanent Coverage:

- Whole life insurance that never expires

- Fixed premiums

- Small cash value accumulation

What Burial Insurance Covers:

- All funeral and burial expenses

- Cemetery costs

- Casket, flowers, obituary

- Memorial service

- Transportation

- Any remaining funds to beneficiaries

Typical Applicant: A 75-year-old senior who specifically wants to ensure funeral and burial costs are covered, with any extra money going to family. They’re primarily concerned with not leaving funeral debt for their children.

Real Burial Insurance Rates

Burial insurance rates are identical to final expense insurance rates because they’re the same product:

$10,000 Coverage – Female Non-Smoker:

- Age 60: $30-$45/month

- Age 65: $40-$55/month

- Age 70: $55-$75/month

- Age 75: $75-$110/month

- Age 80: $110-$155/month

$10,000 Coverage – Male Non-Smoker:

- Age 60: $35-$55/month

- Age 65: $50-$70/month

- Age 70: $65-$95/month

- Age 75: $95-$130/month

- Age 80: $130-$185/month

$20,000 Coverage – Male Non-Smoker:

- Age 60: $70-$110/month

- Age 65: $95-$135/month

- Age 70: $130-$185/month

- Age 75: $185-$255/month

- Age 80: $255-$365/month

Rates are identical to final expense insurance because they’re the same product with different marketing names.

The Real Difference Between Final Expense and Burial Insurance

Now for the truth about what is the difference between final expense and burial insurance: In 99% of cases, there is NO difference. They are the exact same product sold under different names. However, there are a few subtle distinctions that occasionally appear:

Difference #1: Marketing and Branding

Final Expense Insurance:

- Broader marketing term

- Emphasizes covering ALL end-of-life costs

- Implies more comprehensive coverage

- Often marketed with higher coverage amounts ($25,000-$50,000)

Burial Insurance:

- Narrower marketing term

- Focuses specifically on funeral and burial

- More traditional sounding

- Often marketed with lower coverage amounts ($5,000-$15,000)

Reality: Both cover the exact same things. A $15,000 “burial insurance” policy covers your medical bills just like a $15,000 “final expense insurance” policy does.

Difference #2: Coverage Amount Norms

Final Expense Insurance:

- Average policy size: $15,000-$25,000

- Common range: $10,000-$50,000

- Marketed as comprehensive protection

Burial Insurance:

- Average policy size: $10,000-$15,000

- Common range: $5,000-$25,000

- Marketed as funeral-specific coverage

Reality: You can buy any coverage amount from either type. A company offering “burial insurance” will sell you $50,000 if you want it.

Difference #3: Target Demographic

- Marketed to ages 50-85

- Appeals to seniors wanting comprehensive coverage

- Often advertised during daytime TV

- Marketed to ages 65-85

- Appeals to older seniors focused on funerals

- Often advertised in senior-specific publications

Reality: The age ranges and qualifications are identical. Both accept applicants up to age 85 (sometimes 89).

Difference #4: What Companies Call It

Some insurance companies use one term exclusively:

Companies Using “Final Expense”:

- Globe Life

- Mutual of Omaha

- Gerber Life

- Colonial Penn

- Transamerica

Companies Using “Burial Insurance”:

- Many local/regional insurers

- Some direct mail companies

- Smaller insurance agencies

Companies Using Both Terms:

- AARP

- State Farm

- Foresters Financial

- Many independent agents

Reality: The policy documents, coverage, and rates are identical regardless of what the company calls it.

Difference #5: Policy Fine Print (Rare)

In very rare cases, a “burial insurance” policy might have a restriction that funds must be used for funeral/burial expenses. However:

- This is extremely uncommon (less than 1% of policies)

- It’s nearly impossible to enforce

- Most policies pay directly to your named beneficiary with no restrictions

- Beneficiaries can use the money however they choose

Reality: 99% of both final expense and burial insurance policies pay your beneficiary directly with zero restrictions on how the money is used.

Final Expense Insurance vs Burial Insurance: The Real Comparison

Let me break down final expense vs burial life insurance in a clear comparison table:

| Feature | Final Expense Insurance | Burial Insurance |

|---|---|---|

| Coverage Amount | $5,000-$50,000+ | $5,000-$35,000 |

| Purpose | All end-of-life costs | Funeral/burial costs |

| Who It’s For | Ages 50-85 | Ages 65-85 |

| Medical Exam | Not required | Not required |

| Health Questions | Simplified or none | Simplified or none |

| Premium Type | Fixed, never increases | Fixed, never increases |

| Policy Duration | Lifetime (permanent) | Lifetime (permanent) |

| Cash Value | Small amount builds | Small amount builds |

| Approval Time | 24-48 hours typical | 24-48 hours typical |

| What It Covers | Everything | Everything |

| How Paid Out | To beneficiary | To beneficiary |

| Restrictions | None (99% of policies) | None (99% of policies) |

| Average Cost (70F) | $80-$115/month for $15K | $80-$115/month for $15K |

| Companies Offering | Most major insurers | Many insurers |

| Marketing Focus | Comprehensive | Funeral-specific |

The Bottom Line: These are functionally identical products. The “difference” is primarily in marketing and the average coverage amounts people typically buy.

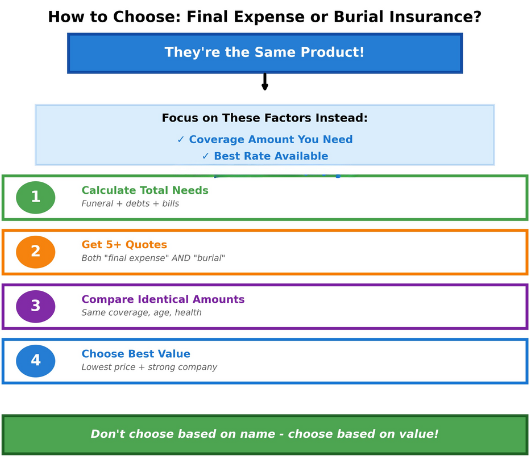

Which One Should You Buy: Final Expense or Burial Insurance?

Since burial insurance vs final expense insurance are essentially the same product, the question isn’t which TYPE to buy—it’s how much coverage you need and which specific POLICY offers the best value. Here’s how to decide:

Buy Whichever Policy Offers:

1. The Best Rate for Your Age and Health

- Get quotes for both “final expense” and “burial” insurance

- Compare identical coverage amounts

- The cheaper option is the winner

- Expect rates to be nearly identical

2. The Coverage Amount You Actually Need

- Calculate your funeral costs: $10,000-$15,000 average

- Add final medical bills: $5,000-$15,000 average

- Add outstanding debts you want covered

- Add estate settlement costs: $5,000-$10,000

- Total = your target coverage amount

3. The Company With Best Financial Strength

- Look for A.M. Best rating of A- or higher

- Verify the company has been in business 20+ years

- Read recent customer reviews

- Ensure they have a track record of paying claims

4. The Policy That Fits Your Budget

- Don’t overpay for coverage you don’t need

- Ensure premiums fit comfortably in your fixed income

- Remember: premiums never increase

- Budget for paying this premium for potentially 10-20+ years

5. The Application Process You’re Comfortable With

- Simplified issue if you can answer health questions

- Guaranteed issue if you have serious health conditions

- Consider waiting periods (guaranteed issue has 2-3 year wait)

- Faster approval with simplified issue (24-48 hours vs instant)

Real-World Decision Examples:

Example 1: Margaret, 72

- Needs: $12,000 for funeral, $3,000 credit card debt = $15,000 total

- Got Quotes: “Final expense” $125/month, “Burial insurance” $120/month

- Decision: Bought the burial insurance (saved $5/month = $60/year)

- Lesson: Same coverage, slightly better rate with burial insurance label

Example 2: Robert, 68

- Needs: $15,000 funeral, $25,000 remaining mortgage = $40,000 total

- Got Quotes: “Burial insurance” only offered up to $25,000, “Final expense” offered $50,000

- Decision: Bought final expense insurance for $40,000

- Lesson: Final expense insurance had higher maximum coverage available

Example 3: Linda, 77

- Needs: $10,000 for funeral only

- Got Quotes: Both offered $10,000 at identical rates ($110/month)

- Decision: Went with final expense because she liked the agent better

- Lesson: When rates are identical, choose based on comfort with company/agent

The Strategy: Don’t focus on the name. Focus on:

- ✓ Coverage amount you need

- ✓ Best rate for that amount

- ✓ Company financial strength

- ✓ Application ease

Costs: Final Expense Insurance vs Burial Insurance Rates

Since these are the same product, the rates are identical when comparing apples to apples. However, rates vary significantly based on several factors. Here’s a comprehensive rate comparison:

Factors Affecting Your Rates (Both Products):

Age:

- Every year of age increases premiums 8-12%

- A 75-year-old pays roughly double what a 65-year-old pays

Gender:

- Females pay 15-30% less than males (same age/coverage)

- Women statistically live longer

Smoking Status:

- Smokers pay 50-100% more than non-smokers

- “Smoker” defined as any tobacco use in past 12-24 months

Health Status:

- Simplified issue: health questions affect rates

- Guaranteed issue: no health questions but 30-50% more expensive

Coverage Amount:

- Rates scale proportionally (double coverage ≈ double premium)

- Some companies offer “sweet spot” pricing at certain amounts

Policy Type:

- Simplified issue: standard rates

- Guaranteed issue: premium rates (no medical questions)

- Graded benefit: varies by company

Comprehensive Rate Table – Both Products

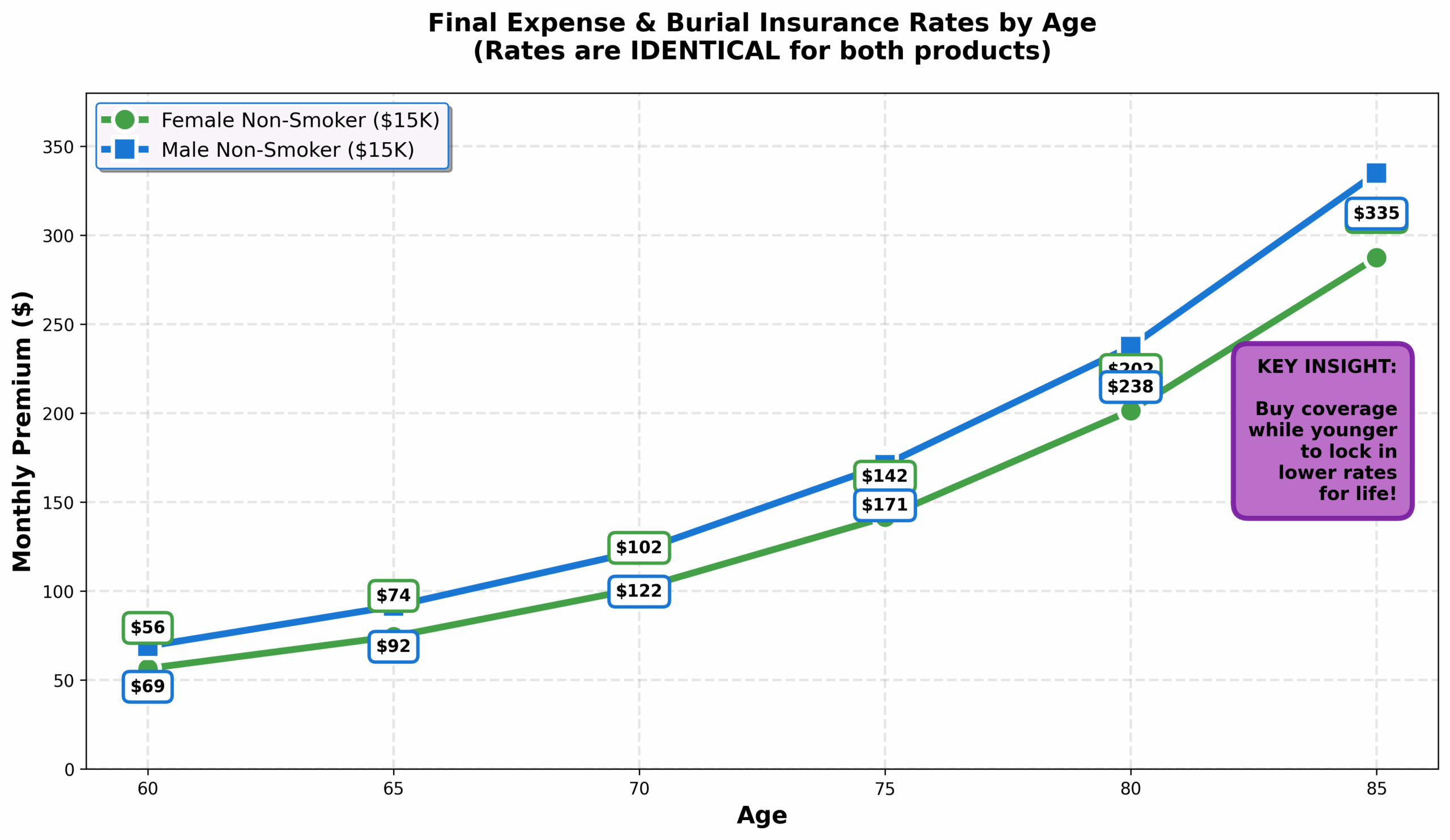

$15,000 Coverage – Non-Smoker, Simplified Issue:

| Age | Female | Male |

|---|---|---|

| 60 | $48-65 | $58-80 |

| 65 | $63-88 | $78-108 |

| 70 | $85-118 | $105-145 |

| 75 | $120-168 | $148-198 |

| 80 | $170-238 | $200-280 |

| 85 | $240-335 | $280-390 |

$15,000 Coverage – Smoker, Simplified Issue:

| Age | Female | Male |

|---|---|---|

| 60 | $85-115 | $105-145 |

| 65 | $115-155 | $140-195 |

| 70 | $155-210 | $190-265 |

| 75 | $215-300 | $265-360 |

| 80 | $305-425 | $360-505 |

| 85 | $430-600 | $505-710 |

$25,000 Coverage – Non-Smoker, Simplified Issue:

| Age | Female | Male |

|---|---|---|

| 60 | $78-105 | $95-130 |

| 65 | $103-143 | $128-178 |

| 70 | $138-193 | $173-238 |

| 75 | $195-275 | $243-325 |

| 80 | $278-390 | $328-460 |

| 85 | $393-550 | $460-640 |

Guaranteed Issue Rates (No Health Questions): Add 30-50% to the simplified issue rates above. For example:

- 70-year-old female, $15,000: $85-118 becomes $110-177

- 75-year-old male, $15,000: $148-198 becomes $192-297

Rate Shopping Strategy:

- Get 5+ Quotes: Rates vary 30-50% between companies for identical coverage

- Compare Identical Coverage: Don’t compare $15K from one company to $20K from another

- Check Both Names: Request quotes for both “final expense” and “burial” insurance

- Verify What’s Included: Ensure you’re comparing simplified issue to simplified issue

- Look Beyond Price: Cheapest isn’t always best if company has poor financial ratings

Common Myths About Final Expense Insurance vs Burial Insurance

Let’s debunk the most common misconceptions about final expense insurance versus burial insurance:

Myth #1: “Burial Insurance Only Covers Funerals”

The Myth: Burial insurance can only be used for funeral and burial expenses, while final expense covers everything.

The Truth: Both policies pay your beneficiary directly with no restrictions (99% of cases). Your beneficiary can use the money for anything: funerals, debts, bills, groceries, vacation—literally anything. The insurance company doesn’t track or control how the money is spent.

Why It Persists: The name “burial insurance” implies restriction, but it’s just marketing.

Myth #2: “Final Expense Insurance Costs More”

The Myth: Because “final expense” sounds more comprehensive, it must be more expensive than “burial insurance.”

The Truth: Rates are identical for the same coverage amount, age, gender, and health status. A $15,000 policy costs the same whether called “final expense” or “burial insurance.”

Why It Persists: People assume fancier names mean higher prices.

Myth #3: “You Need Both Policies”

The Myth: You should buy burial insurance for your funeral AND final expense insurance for other costs.

The Truth: You only need ONE policy with sufficient coverage for everything. Buying both is redundant and wastes money. Calculate your total needs and buy one policy for that amount.

Why It Persists: Aggressive sales tactics and confusion about the difference.

Myth #4: “Burial Insurance Has Lower Maximums”

The Myth: Burial insurance only offers small amounts ($10,000 max) while final expense offers higher limits.

The Truth: Both types typically offer $5,000-$50,000, with some companies going up to $75,000. The name doesn’t restrict the available amounts.

Why It Persists: Marketing tends to show lower amounts for burial insurance.

Myth #5: “Final Expense Insurance Covers More Things”

The Myth: Final expense insurance has broader coverage than burial insurance.

The Truth: Both cover identical items. Both are whole life insurance policies that pay a death benefit to your beneficiary. The death benefit can be used for anything.

Why It Persists: The word “final expense” sounds more comprehensive than “burial.”

Myth #6: “You Can’t Get Burial Insurance With Health Problems”

The Myth: Burial insurance requires good health, but final expense insurance accepts anyone.

The Truth: Both products offer guaranteed issue versions that accept anyone regardless of health, and both offer simplified issue versions with health questions. The acceptance criteria are identical.

Why It Persists: Confusion about policy types (guaranteed issue vs simplified issue).

Myth #7: “One Is Better for Seniors Over 80”

The Myth: Burial insurance is specifically designed for seniors over 80, while final expense is for younger seniors.

The Truth: Both products accept seniors up to age 85 (sometimes 89). Age limits are identical.

Why It Persists: Marketing demographics differ, but products are the same.

How to Get the Best Rate on Either Policy

Whether you’re shopping for final expense or burial insurance, follow these strategies to get the lowest possible rate:

Strategy #1: Shop Multiple Companies (5+ Quotes)

Different companies price the same coverage very differently:

- Company A (70F, $15K): $95/month

- Company B (70F, $15K): $125/month

- Company C (70F, $15K): $88/month

- Savings by shopping: $37/month = $444/year

Action: Get quotes from at least 5 companies before deciding.

Strategy #2: Quit Smoking If Possible

Smoking status dramatically affects rates:

- Non-smoker (70M, $15K): $105/month

- Smoker (70M, $15K): $190/month

- Savings by quitting: $85/month = $1,020/year

Action: If you can quit for 12-24 months, reapply as a non-smoker.

Strategy #3: Buy When You’re Younger

Every year you wait, rates increase:

- Age 68 (F, $15K): $75/month

- Age 70 (F, $15K): $95/month

- Age 72 (F, $15K): $110/month

- Cost of waiting 4 years: $35/month more = $420/year more

Action: Don’t procrastinate. Buy coverage while you’re younger and healthier.

Strategy #4: Choose Simplified Issue Over Guaranteed Issue

If you can answer health questions favorably:

- Simplified issue (70F, $15K): $95/month

- Guaranteed issue (70F, $15K): $142/month

- Savings with simplified: $47/month = $564/year

Action: Try simplified issue first. Only use guaranteed issue if you can’t qualify.

Strategy #5: Buy Only What You Need

Don’t overbuy coverage:

- Actual need: $15,000 (funeral + small debts)

- Agent recommends: $30,000 (“just to be safe”)

- Overpaying: $95/month vs $165/month = $840/year wasted

Action: Calculate your actual needs first. Don’t let agents upsell you.

Strategy #6: Pay Annually If Possible

Many companies offer discounts for annual payment:

- Monthly payment: $100/month × 12 = $1,200/year

- Annual payment: $1,140 (5% discount)

- Savings: $60/year

Action: If you can afford the lump sum, pay annually.

Strategy #7: Work With Independent Agents

Independent agents represent multiple companies:

- Captive agent: Can only quote one company

- Independent agent: Compares 10+ companies

- Result: Independent finds best rate across all options

Action: Use independent agents who can shop multiple companies for you.

Strategy #8: Improve Health Before Applying

For simplified issue policies, better health = better rates:

- Lose weight (obesity adds 10-30% to premiums)

- Control blood pressure (uncontrolled adds 20-40%)

- Manage diabetes (well-controlled is much cheaper)

- Get off oxygen if possible (oxygen use is major factor)

Action: If you have 3-6 months, work on health before applying.

Strategy #9: Consider Group Through Organizations

Some organizations offer group rates:

- AARP membership

- Union membership

- Professional associations

- Veterans groups

Action: Check if any organizations you belong to offer group rates.

Strategy #10: Review Rates Every 2-3 Years

If your health improves or you quit smoking:

- Year 1: Bought guaranteed issue at $150/month (had oxygen)

- Year 3: Off oxygen now, reapplied for simplified issue

- New rate: $98/month

- Savings: $52/month = $624/year for rest of life

Action: If circumstances change favorably, reapply for better rates.

Frequently Asked Questions

What is the main difference between final expense and burial insurance?

The main difference between final expense and burial insurance is marketing terminology, not actual policy differences. Both are whole life insurance products designed to cover end-of-life costs, require no medical exam, offer coverage from $5,000-$50,000, and pay death benefits directly to your beneficiary with no restrictions on usage.

“Final expense insurance” is marketed as comprehensive coverage for all end-of-life costs, while “burial insurance” emphasizes funeral and burial expenses specifically. However, both policies cover identical items: funeral costs, burial or cremation, medical bills, debts, estate settlement costs, and any remaining funds go to beneficiaries.

The rates are identical for the same coverage amount, age, and health status. In 99% of cases, these are the exact same product sold under different names, and you should choose based on price and company reputation rather than which term is used.

Is burial insurance the same as final expense insurance?

Yes, burial insurance vs final expense insurance are essentially the same product. Both are permanent whole life insurance policies with no medical exam required, coverage amounts typically between $5,000-$50,000, fixed premiums that never increase, and death benefits paid directly to beneficiaries with no restrictions.

The only differences are marketing terminology and typical coverage amounts purchased—”burial insurance” is often marketed with lower amounts ($10,000-$15,000) focused specifically on funeral costs, while “final expense insurance” is marketed with higher amounts ($15,000-$25,000) emphasizing comprehensive end-of-life cost coverage.

However, you can purchase any amount from either type, both cover the same expenses, and rates are identical for comparable policies. Insurance companies use these terms interchangeably, and policy documents are typically identical regardless of which name is used. Choose based on coverage amount needed, price, and company reputation, not the terminology.

Can I use burial insurance for things other than funeral costs?

Yes, absolutely. Despite its name, burial insurance pays the death benefit directly to your named beneficiary with no restrictions on how the money is used.

Your beneficiary can use burial insurance funds for funeral costs, outstanding debts, medical bills, mortgage payments, credit cards, everyday living expenses, or anything else they choose. The insurance company does not track, control, or dictate how the money is spent.

This is true for both burial insurance and final expense insurance—both products function identically. In extremely rare cases (less than 1% of policies), a policy might specify funds must be used for burial expenses, but this is almost never enforced and very uncommon. The standard practice is unrestricted payment to beneficiaries.

This flexibility means you can buy “burial insurance” with confidence that your family can use the funds however they need most, whether that’s for funeral costs, paying bills, or anything else.

Which is cheaper: final expense or burial insurance?

Neither final expense insurance vs burial insurance is inherently cheaper because they’re the same product. When comparing identical coverage amounts, age, gender, health status, and policy type (simplified issue vs guaranteed issue), the premiums are the same regardless of whether it’s labeled “final expense” or “burial insurance.”

However, rates vary dramatically between insurance companies—by 30-50% or more—so shopping multiple insurers is critical. For example, a 70-year-old female seeking $15,000 coverage might see quotes ranging from $85/month to $125/month across different companies, but these variations are due to company pricing strategies, not the final expense vs burial insurance terminology.

The best strategy is to request quotes for both terms from multiple companies and compare identical coverage amounts. Factors that DO affect cost include your age (older = more expensive), gender (males pay more), smoking status (smokers pay 50-100% more), health (guaranteed issue costs 30-50% more than simplified issue), and coverage amount.

Do I need both final expense and burial insurance?

No, you absolutely do not need both policies. This is one of the biggest myths in the insurance industry. Final expense insurance vs burial insurance are the same product with different marketing names, so buying both would mean you’re paying for duplicate coverage.

Instead, calculate your total end-of-life costs (funeral $10,000-$15,000, final medical bills, outstanding debts, estate costs) and purchase ONE policy with sufficient coverage for everything.

For example, if your funeral will cost $12,000, you have $5,000 in credit card debt, and you want $8,000 for estate settlement costs, you need $25,000 total coverage—buy one $25,000 policy (called either final expense or burial insurance).

Having two separate policies wastes money on duplicate premiums and creates unnecessary complexity for your beneficiaries.

The only time you might have multiple policies is if you already have an existing small policy and need additional coverage, but even then you’d buy one additional policy, not specific “burial” vs “final expense” products.

What does final expense insurance actually cover?

Final expense insurance covers everything related to your end-of-life costs because it pays your beneficiary an unrestricted death benefit.

Specifically, it can cover: funeral service costs ($2,000-$5,000), burial or cremation expenses ($2,000-$10,000), casket or urn ($1,000-$10,000), cemetery plot and headstone ($2,000-$6,000), flowers and obituaries ($500-$2,000), memorial service and reception, final medical bills not covered by health insurance, outstanding credit card debt, car loans or personal loans, mortgage balance (if you choose enough coverage), probate and estate settlement costs ($5,000-$10,000), attorney fees for estate matters, and any remaining balance goes to your beneficiaries to use however they need.

The insurance company doesn’t dictate or restrict what the money is used for—your beneficiary receives a check and can spend it on anything. This comprehensive coverage is why many seniors prefer final expense insurance over trying to save money separately for these costs.

How much does burial insurance cost per month?

Burial insurance costs depend on your age, gender, health status, smoking status, and coverage amount. For a 70-year-old purchasing $15,000 coverage: a non-smoking female pays $85-$118/month with simplified issue, a non-smoking male pays $105-$145/month with simplified issue, a smoking female pays $155-$210/month, and a smoking male pays $190-$265/month.

Guaranteed issue policies (no health questions) cost 30-50% more than simplified issue. For a 75-year-old purchasing $10,000 coverage: a non-smoking female pays $75-$110/month, while a non-smoking male pays $95-$130/month. Rates increase approximately 8-12% for each year of age.

For $25,000 coverage at age 70: a non-smoking female pays $138-$193/month, while a non-smoking male pays $173-$238/month.

These ranges reflect variations between insurance companies, which is why shopping multiple companies is essential—you might find rates varying by $30-$50/month for identical coverage. Remember that burial insurance vs final expense insurance cost the same for identical coverage.

At what age should I buy final expense insurance?

The best age to buy final expense insurance is as soon as you’re thinking about it, typically between ages 60-70, because premiums increase 8-12% for every year you wait.

A 65-year-old pays significantly less than a 70-year-old for identical coverage—often $30-$50/month difference for $15,000 coverage. Additionally, buying younger means you’re more likely to qualify for simplified issue rather than guaranteed issue, saving 30-50% on premiums.

However, final expense insurance is available and beneficial at any age from 50-85: in your 50s, you lock in the lowest possible rates for life; in your 60s, you still get good rates and likely qualify for simplified issue; in your 70s, rates are higher but still affordable and coverage is important; in your 80s, guaranteed issue ensures you can get coverage regardless of health.

Don’t wait until you’re experiencing health problems or until you’re in your 80s unless necessary, as this results in significantly higher premiums or limited options. The premiums you pay at age 65 stay the same for life, so buying early means decades of lower payments.

Can I get burial insurance if I have health problems?

Yes, you can absolutely get burial insurance even with serious health conditions. Both burial insurance and final expense insurance offer two underwriting options that accommodate health issues: simplified issue policies ask 5-10 basic health questions and accept most conditions as long as they’re well-managed (diabetes, high blood pressure, heart disease, COPD, and even cancer survivors after waiting periods), while guaranteed issue policies ask zero health questions and accept everyone regardless of health conditions—even if you’re on oxygen, have terminal illness, or have been declined by other insurers.

Guaranteed issue policies have two features: they cost 30-50% more than simplified issue because the insurance company takes on more risk, and they include a waiting period (typically 2-3 years) where natural death pays back premiums plus interest rather than full death benefit, though accidental death pays full benefit immediately.

After the waiting period expires, full coverage applies for any cause of death. Many seniors with health conditions start with guaranteed issue for immediate protection, then reapply for simplified issue later if their health improves, securing better rates.

What happens if I outlive my burial insurance policy?

You cannot outlive burial insurance or final expense insurance because both are permanent whole life insurance policies that last your entire lifetime, unlike term life insurance which expires after a set period.

Your burial insurance remains in force as long as you continue paying premiums, regardless of whether you live to age 90, 100, or beyond.

The death benefit will eventually pay out whenever you pass away, whether that’s next year or in 30 years. Additionally, burial insurance builds a small cash value over time that you can borrow against or withdraw if needed in later years, though doing so reduces the death benefit.

Your premiums never increase—the monthly payment you start with remains the same for life, which is particularly valuable as you age on a fixed income.

This permanent coverage is one of the key benefits of burial insurance and final expense insurance compared to term life insurance, which many seniors outlive, leaving them with no coverage when they actually need it most.

Is $10,000 enough for burial insurance?

Whether $10,000 burial insurance is enough depends on your specific end-of-life costs and financial goals. For funeral and burial expenses only, $10,000 typically covers a basic funeral ($7,000-$12,000 average cost nationally), though prices vary significantly by location—urban areas and certain regions cost more.

However, $10,000 might NOT be enough if you have: outstanding debts you want covered (credit cards, car loans, personal loans), a remaining mortgage balance, final medical bills from extended illness, estate settlement and probate costs ($5,000-$10,000 typically), or want to leave any inheritance for family members.

Most financial experts recommend $15,000-$25,000 in coverage to comfortably handle funeral costs plus financial loose ends.

To determine if $10,000 is sufficient for you, calculate: funeral service costs ($2,000-$5,000) + burial/cremation ($2,000-$10,000) + plot and headstone ($2,000-$6,000) + your outstanding debts + estate costs + desired buffer = your total need. If this equals $10,000 or less and you have no other significant expenses, then $10,000 coverage is adequate. If more, consider $15,000-$25,000.

Can my family use burial insurance money for anything?

Yes, your family can use burial insurance money (also called final expense insurance money) for absolutely anything they choose because the death benefit is paid directly to your named beneficiary with no restrictions, requirements, or oversight on how funds are spent.

While the policy is named “burial insurance” and marketed for funeral costs, your beneficiary receives an unrestricted lump sum payment that they can legally use for: funeral and burial expenses, cremation costs, paying off your debts, mortgage or rent payments, credit card bills, medical bills, car loans, everyday living expenses, groceries and utilities, emergency funds, college savings for grandchildren, vacation, investments, or anything else.

The insurance company does not track, monitor, control, or dictate how the money is used, and your beneficiary never has to report or justify their spending. Less than 1% of burial insurance policies have any restrictions requiring funeral use, and even those are rarely enforced.

This unrestricted flexibility is a major benefit and means you can buy burial insurance knowing your family will have complete freedom to use the funds wherever the money is needed most.

Taking Action: Choosing Between Final Expense and Burial Insurance

Now that you fully understand final expense insurance vs burial insurance, it’s time to take action. Here’s your step-by-step roadmap:

This Week:

Step 1: Calculate Your Coverage Needs

- Estimate funeral costs: $10,000-$15,000 average

- List outstanding debts you want covered

- Add final medical expenses estimate

- Include estate settlement costs: $5,000-$10,000

- Add any legacy/inheritance goals

- Total = Your Target Coverage Amount

Step 2: Determine Your Budget

- Review your monthly fixed income

- Decide maximum affordable monthly premium

- Remember: premiums never increase

- Budget for paying this for potentially 20+ years

Step 3: Assess Your Health Status

- Can you answer basic health questions favorably?

- YES → Request simplified issue quotes (lower cost)

- NO → Request guaranteed issue quotes (accepts everyone)

This Month:

Step 4: Get Multiple Quotes

- Contact 5+ insurance companies or independent agents

- Request both “final expense” AND “burial insurance” quotes

- Ask for identical coverage amounts across all quotes

- Get rates for both simplified issue and guaranteed issue

Step 5: Compare Quotes Side-by-Side

Mutual of Omaha: $15,000 Final Expense - $95/month - A+ rated

Transamerica: $15,000 Burial Insurance - $110/month - A rated

AIG: $15,000 Final Expense - $88/month - A- rated

Gerber: $15,000 Burial Insurance - $105/month - A+ rated

Step 6: Check Company Financial Strength

- Verify A.M. Best rating (A- or higher recommended)

- Confirm company has been in business 20+ years

- Read recent customer reviews

- Check complaint ratios with state insurance department

Step 7: Review Policy Details Before buying, verify:

- Coverage amount matches your needs

- Premium fits your budget comfortably

- You understand waiting periods (if guaranteed issue)

- Beneficiary designation is correct

- You know exactly what you’re paying monthly

Before You Buy:

Step 8: Ask These Critical Questions

- Is this simplified issue or guaranteed issue?

- Are there any waiting periods or limitations?

- Does the premium stay the same forever?

- Is there a free look period (usually 30 days)?

- What is the company’s A.M. Best rating?

- How are claims typically processed?

- Can I change beneficiaries later?

Step 9: Make Your Decision Choose based on:

- ✓ Best rate for your needed coverage amount

- ✓ Company with strong financial ratings

- ✓ Policy that fits comfortably in your budget

- ✓ Company and agent you feel comfortable with

Don’t choose based on whether it’s called “final expense” or “burial insurance”—they’re the same product!

Step 10: Complete Your Application

- Fill out application honestly and completely

- Provide accurate health information (if simplified issue)

- Name your beneficiary carefully

- Keep copy of all documents

- Note your free look period end date

Conclusion: Final Expense vs Burial Insurance – The Final Word

After exploring every aspect of final expense insurance vs burial insurance, here’s what you need to remember:

The Core Truth: These are the same product sold under different marketing names. The difference between final expense and burial insurance is branding, not substance. Both are whole life insurance policies that cover your end-of-life costs, require no medical exam, offer permanent coverage with fixed premiums, and pay your beneficiary an unrestricted death benefit.

What Really Matters: Instead of worrying about terminology, focus on:

- Coverage Amount: Calculate your actual needs ($10,000-$25,000 for most seniors)

- Premiums: Shop 5+ companies to find the best rate

- Company Strength: Choose financially stable insurers (A- rating or higher)

- Policy Type: Simplified issue if you qualify, guaranteed issue if needed

- Your Budget: Ensure premiums fit comfortably in your fixed income

Your Next Step: Don’t let confusion about final expense vs burial life insurance delay your planning. Both products accomplish the same critical goal: protecting your family from financial burden when you pass away. Request quotes for BOTH terms from multiple companies, compare identical coverage amounts, and choose the policy that offers the best value from a reputable insurer.

The Peace of Mind: Whether you buy a policy called “final expense insurance,” “burial insurance,” or “funeral insurance,” what matters is having coverage in place. Your family will be grateful you took the time to plan ahead, ensuring they can focus on grieving and celebrating your life rather than worrying about how to pay for your funeral and final expenses.

The difference between these policies is semantic—the difference between having coverage and not having coverage is everything.

Disclaimer: This article provides general educational information about final expense insurance and burial insurance and should not be considered insurance, financial, or legal advice. Insurance products, coverage terms, costs, and availability vary by company, state, and individual circumstances. Premium rates quoted are approximate ranges for illustration purposes and may not reflect actual rates available to you. Actual premiums depend on age, gender, health status, smoking status, coverage amount, state of residence, and specific insurance company underwriting guidelines. Policy features, waiting periods, and restrictions vary by insurer. Always review complete policy documents, ask questions about anything you don’t understand, and compare multiple quotes before purchasing. Consult with licensed insurance professionals regarding your specific situation and needs. This guide is not affiliated with or endorsed by any insurance company mentioned. Information is current as of publication date but insurance products and rates change frequently.