Life Insurance for Seniors Over 80: Your Complete Guide (2026)

Posted in Senior Life Insurance on December 2, 2025 last updated on May 27, 2026

Posted in Senior Life Insurance on December 2, 2025 last updated on May 27, 2026

Can Seniors Over 80 Still Get Life Insurance?

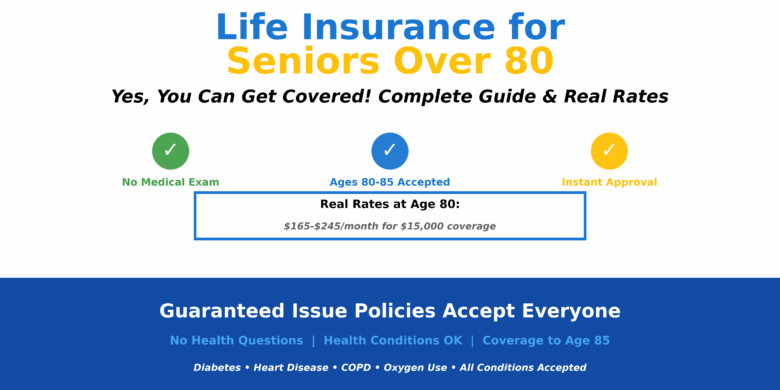

Yes, many seniors over 80 can still qualify for life insurance, especially final expense, guaranteed issue, and simplified issue whole life policies. Approval and pricing depend on health, coverage amount, and the insurance company selected. Many insurers still offer coverage into the mid-80s.

I get this question almost daily: “I’m 82 years old—can I still get life insurance?” And every single time, I’m happy to deliver good news: Yes, you absolutely can.

Getting life insurance for seniors over 80 is not only possible, it’s actually easier than you might think. You don’t need a medical exam. You won’t have to answer dozens of health questions. And you can often get approved in just minutes, even if you have diabetes, heart disease, or use oxygen.

I’ve helped hundreds of seniors in their 80s secure coverage over the past fifteen years, and I’ve seen firsthand how much peace of mind it brings. There’s Margaret, who got approved at 84 with COPD and couldn’t believe it was “that simple.” There’s Robert, who secured coverage at 81 to pay off final medical bills his wife shouldn’t have to worry about. And there’s Dorothy, who at 86 wanted to leave $10,000 to her church—and she did exactly that.

The truth is, insurance companies have gotten much better at serving seniors over 80. They understand you’re not trying to leave a million-dollar legacy—you just want to cover funeral costs, settle small debts, and avoid burdening your family. That’s exactly what life insurance over 80 is designed to do.

In this guide, I’ll walk you through everything you need to know about life insurance for 80 year olds: which companies accept applicants your age, what you’ll actually pay (real numbers, not vague estimates), how the application process works, and what to watch out for. Whether you’re 80 or 85, healthy or managing multiple conditions, you’ll learn exactly how to get the coverage you need without the hassle you don’t.

Let’s get started and find you the right policy.

Yes, You Can Get Life Insurance at Age 80

Let me address the biggest concern right away: age 80 isn’t too old for life insurance. In fact, most major insurance companies accept applicants up to age 85, and some even go to 89.

Why Companies Insure Seniors Over 80

Insurance companies aren’t doing you a favor out of kindness—they’re running a business. And the business model works because:

The Math Makes Sense for Everyone:

- Seniors over 80 typically buy smaller policies ($10,000-$25,000)

- Premiums are higher to reflect actuarial reality

- Coverage often includes waiting periods (2-3 years)

- Insurance companies collect premiums for years before most claims

- It’s profitable for insurers while affordable for seniors

The Need Is Real and Specific:

- Funeral costs average $7,000-$12,000 nationally

- Final medical bills can reach $5,000-$15,000

- Small debts and estate costs need handling

- Families genuinely struggle with unexpected expenses

- Seniors want dignity, not debt for their children

Modern Underwriting Has Evolved:

- Guaranteed issue policies accept everyone (no health questions)

- Simplified processes don’t require medical exams

- Fast approvals (often instant online)

- Realistic expectations about health at 80+

- Companies specialize in senior coverage

What “Life Insurance Over 80” Actually Looks Like

If you’re picturing complicated applications, doctor visits, and stacks of paperwork—you’re thinking of traditional life insurance from decades ago. Life insurance for seniors over 80 is completely different:

The Modern Reality:

- Application takes 5-10 minutes (online or by phone)

- No medical exam required

- No blood tests, urine samples, or doctor calls

- Often no health questions at all (guaranteed issue)

- Instant or 24-hour approval

- Coverage from $5,000 to $50,000

- Premiums never increase

- Coverage lasts your entire life

What You’ll Need:

- Basic personal information (name, address, DOB)

- Social Security number

- Beneficiary information

- Payment method for first premium

- That’s it—seriously

I’ve watched 84-year-olds complete applications on their smartphones while sitting at the kitchen table. It’s designed to be simple because insurance companies know their customers are seniors who want straightforward solutions, not bureaucratic nightmares.

Companies That Accept Seniors Over 80

You’re not limited to one or two obscure companies. Major, well-established insurers actively compete for your business:

Top Companies (Ages 80-85):

- Mutual of Omaha (up to age 85)

- Globe Life (up to age 85)

- Foresters Financial (up to age 80)

- Colonial Penn (up to age 85)

- Gerber Life (up to age 80)

- AIG/American General (up to age 85)

- Liberty Bankers (up to age 89)

All of these companies have A ratings or higher from A.M. Best, meaning they’re financially stable and will be around to pay your claim. They’ve been in business for decades—some over a century—and they specialize in senior life insurance.

Best Types of Life Insurance for Seniors Over 80

Not all life insurance for 80 year olds is created equal. Understanding the types of life insurance helps you choose the right coverage at the right price.

Guaranteed Issue Life Insurance (Most Common)

Guaranteed issue life insurance is what most seniors over 80 purchase, and for good reason—it’s specifically designed for your age and situation.

How It Works:

- Zero health questions asked

- Everyone accepted regardless of conditions

- No medical exam or doctor calls

- Instant approval (online or phone)

- Coverage starts immediately

- Premiums never increase

The Trade-Offs:

- Waiting Period (2-3 Years): If you pass away from natural causes in the first 2-3 years, your beneficiaries receive premiums paid plus 10% interest, not the full death benefit

- Accidental Death Exception: Accidental death pays full benefit from day one

- After Waiting Period: Full coverage for any cause of death

- Higher Premiums: Costs 30-50% more than simplified issue because insurers accept everyone

Who It’s For:

- Seniors with serious health conditions

- Anyone on oxygen or with severe COPD

- Recent cancer patients or treatment

- Heart attack or stroke survivors

- Anyone declined by other insurers

- Anyone who wants instant, guaranteed approval

Real Example: Helen, 83, has diabetes, high blood pressure, and uses a walker. She applied for $15,000 guaranteed issue coverage, got approved instantly online, and pays $178/month. Her kids will get the full $15,000 when she passes, as long as it’s after the 2-year mark (accidental death would pay immediately).

Simplified Issue Life Insurance (Limited Availability)

A few companies offer simplified issue to healthy seniors over 80, though most cap this at age 80-82.

How It Works:

- 5-10 basic health questions

- No medical exam required

- Approval within 24-48 hours

- No waiting period (full coverage day one)

- Lower premiums than guaranteed issue

The Questions They Ask:

- Hospitalized in past 2 years?

- Currently use oxygen?

- Cancer diagnosis in past 5 years?

- Heart attack or stroke recently?

- Current medications and conditions

- Height and weight

Who It’s For:

- Seniors 80-82 in relatively good health

- No recent hospitalizations

- Managed conditions (controlled diabetes, stable blood pressure)

- Not on oxygen or in hospice

- Want to avoid waiting period

- Want lower premiums (30-50% savings)

Real Example: George, 81, is in decent health with only controlled high blood pressure. He answered health questions, got approved in one day, and pays $148/month for $15,000—about $50/month less than guaranteed issue. His coverage started immediately with no waiting period.

Final Expense vs Whole Life Insurance

These terms are often used interchangeably for seniors, but there’s a subtle difference:

- Marketed specifically for funeral/final costs

- Coverage typically $5,000-$25,000

- Simplified or guaranteed issue

- Ages 50-85 accepted

- What most seniors over 80 buy

- Traditional permanent life insurance

- Broader marketing (not age-specific)

- Can offer larger amounts ($50,000+)

- May have more restrictive underwriting

- Same product structure as final expense

Bottom Line: For seniors over 80, these are functionally identical. Buy the one with the better rate and stronger company, regardless of name.

| Policy Type | Medical Exam | Best For | Typical Coverage |

|---|---|---|---|

| Final Expense | Usually No | Funeral costs | $5K–$50K |

| Guaranteed Issue | No | Serious health conditions | $5K–$25K |

| Simplified Issue | No | Moderate health conditions | $10K–$100K |

| Whole Life | Sometimes | Healthier seniors | Higher |

What About Term Life Insurance?

Short answer: term life insurance over age 80 is virtually nonexistent and wouldn’t make sense anyway.

Why Term Doesn’t Work:

- Term policies expire (10, 20, or 30 years)

- At 80, you need permanent coverage

- Term premiums for age 80+ are astronomical when available

- You could outlive the policy and receive nothing

- Whole life guarantees eventual payout

Exception: If you’re 80 and only need coverage for a very specific short-term need (like a 5-year home equity loan), you might find term. But it’s rare and expensive.

Real Costs: What You’ll Actually Pay

Let’s talk real numbers. No vague ranges or “contact us for a quote” nonsense. Here’s what life insurance for seniors over 80 actually costs in 2025.

Average Premiums by Age and Coverage ($15,000 Policy)

Guaranteed Issue – Female Non-Smoker:

- Age 80: $165-$245/month

- Age 81: $178-$265/month

- Age 82: $192-$285/month

- Age 83: $208-$308/month

- Age 84: $225-$335/month

- Age 85: $245-$365/month

Guaranteed Issue – Male Non-Smoker:

- Age 80: $228-$298/month

- Age 81: $248-$325/month

- Age 82: $268-$355/month

- Age 83: $290-$385/month

- Age 84: $315-$420/month

- Age 85: $342-$458/month

Simplified Issue – Female Non-Smoker (Ages 80-82):

- Age 80: $115-$165/month

- Age 81: $125-$178/month

- Age 82: $135-$192/month

Simplified Issue – Male Non-Smoker (Ages 80-82):

- Age 80: $155-$215/month

- Age 81: $168-$235/month

- Age 82: $182-$255/month

How Coverage Amount Affects Price

The rates above are for $15,000 coverage (most popular amount). Here’s how other amounts compare:

$10,000 Coverage:

- Multiply rates above by 0.67X

- Example: Female 80 guaranteed issue = $110-$165/month

$20,000 Coverage:

- Multiply rates above by 1.33X

- Example: Male 80 guaranteed issue = $303-$397/month

$25,000 Coverage:

- Multiply rates above by 1.67X

- Example: Female 80 guaranteed issue = $275-$410/month

Why These Multiples Aren’t Exact: Insurance companies round to certain pricing tiers, so a $25,000 policy won’t be precisely 1.67X a $15,000 policy—but it’s close enough for planning.

Factors That Affect Your Rate

Age: Every year increases premiums by roughly 8-12%. An 81-year-old pays 8-12% more than an 80-year-old.

Gender: Females pay 25-35% less than males at the same age because of longer life expectancy.

Smoking: Smokers pay 60-100% more. “Smoker” = any tobacco use in past 12-24 months.

Coverage Amount: Larger policies cost proportionally more, but the per-thousand-dollars rate slightly decreases.

Policy Type: Guaranteed issue costs 30-50% more than simplified issue for the same coverage.

Company: Rates vary 25-40% between companies for identical coverage—shopping matters!

Payment Frequency: Annual payment sometimes offers 5-10% discount versus monthly.

Company-Specific Rate Comparison (Age 80, $15,000, Female Non-Smoker, Guaranteed Issue)

| Company | Monthly Premium | Annual Total |

|---|---|---|

| Globe Life | $165 | $1,980 |

| Mutual of Omaha | $178 | $2,136 |

| Gerber Life | $172 | $2,064 |

| Colonial Penn | $198 | $2,376 |

| Foresters | $188 | $2,256 |

Savings Potential: Shopping between just these five companies saves $33/month ($396 annually) between cheapest and most expensive.

How the Application Process Actually Works

I’m going to walk you through this step-by-step because knowing exactly what to expect makes the process much less intimidating.

Step 1: Decide How Much Coverage You Need

Quick Calculation:

- Average funeral: $7,000-$12,000

- Final medical bills: $3,000-$8,000

- Small debts (credit cards, etc.): $__________

- Estate settlement costs: $2,000-$5,000

- Cushion for family: $__________

- Total = Your Coverage Amount

Most seniors over 80 buy $10,000-$20,000. That’s enough for funeral expenses and some extra for final bills without paying for excessive coverage you don’t need.

Step 2: Choose Guaranteed Issue or Simplified Issue

Choose Guaranteed Issue If:

- You have serious health conditions

- You’ve been hospitalized recently

- You use oxygen or mobility aids

- You’re on multiple medications

- You’ve been declined before

- You want instant approval with zero questions

Choose Simplified Issue If:

- You’re age 80-82 (most cap at 82)

- Your health is relatively stable

- No hospitalizations in past 2 years

- You’re not on oxygen

- You can answer 5-10 health questions honestly

- You want lower premiums and no waiting period

When Uncertain: Start with simplified issue. If declined, switch to guaranteed issue.

Step 3: Get Quotes from 5+ Companies

This is where most people stop short—but don’t! Getting multiple quotes is the single most important thing you can do.

How to Get Quotes:

- Call companies directly

- Use comparison websites (but verify with company)

- Work with independent insurance agents

- Check online quote tools

What to Compare:

- Monthly premium for identical coverage

- Total annual cost

- Company A.M. Best rating (A- or higher)

- Customer service reviews

- Claims payment reputation

Time Investment: 2-3 hours gathering quotes saves $300-$600 annually for the rest of your life.

Step 4: Complete Your Application

For Guaranteed Issue (Easiest):

- Provide basic personal information

- Name your beneficiary (with their info)

- Choose coverage amount

- Confirm premium and payment method

- Submit (often online or phone)

- Get instant approval

- Pay first premium to activate

Total Time: 5-10 minutes

For Simplified Issue:

- Everything above, plus:

- Answer 5-10 health questions honestly

- Provide medication list if asked

- Submit for underwriting review

- Wait 24-48 hours for decision

- If approved, pay first premium

Total Time: 15-20 minutes plus waiting for approval

Step 5: Review Your Policy Documents

You’ll receive policy documents by mail and/or email. Read them carefully and verify:

- Your name is spelled correctly

- Coverage amount matches what you applied for

- Premium matches the quote

- Beneficiary names and information are correct

- Beneficiary percentages add to 100%

- You understand the waiting period (if guaranteed issue)

- You know when full coverage begins

Free Look Period: You have 30 days to cancel and get a full refund if anything is wrong. Use this time to review everything.

Step 6: Set Up Payment

Payment Options:

- Monthly bank draft (most common)

- Quarterly or annual payment

- Online payment portal

- Phone payments

- Mailed checks (accepted but not recommended)

Critical: Set up automatic payments. Missing a payment can cause your policy to lapse, and getting new coverage at age 81 costs more than at 80.

Real Application Example: Dorothy, Age 84

Dorothy wanted $15,000 to cover her funeral and leave something for her grandkids. Here’s her actual experience:

Day 1 (Monday morning):

- Called three companies for quotes

- Globe Life: $235/month

- Mutual of Omaha: $248/month

- Gerber Life: $242/month

- Chose Globe Life (lowest rate)

Day 1 (Monday afternoon):

- Applied online (guaranteed issue)

- Took 8 minutes total

- Named her daughter as beneficiary

- Got instant approval

- Paid first month’s premium via debit card

- Coverage active immediately (with 2-year waiting period)

Day 4 (Thursday):

- Received policy documents by email

- Reviewed everything—all correct

- Set up automatic monthly bank draft

Total effort: Less than one hour spread across four days.

Common Questions About Life Insurance Over 80

Let me answer the questions I hear most often from seniors in their 80s.

“Will My Pre-Existing Health Conditions Prevent Approval?”

No—not with guaranteed issue. That’s the entire point.

Conditions That Are Accepted:

- Diabetes (any type, any A1C level)

- Heart disease

- Heart attack history

- Stroke or TIA history

- High blood pressure (controlled or not)

- COPD (even with oxygen use)

- Cancer (current or history)

- Kidney disease

- Arthritis, mobility issues

- Multiple health conditions

- AFIB

- Pacemaker

- Medications like blood thinners

The Only Real Exceptions:

- Some companies won’t insure if you’re currently in hospice

- Terminal diagnosis with life expectancy under 12 months sometimes excluded

- These are rare restrictions and don’t apply to most applicants

With guaranteed issue, if you’re alive and under the maximum age (usually 85), you’re approved. Your health doesn’t matter.

“What If I Can’t Afford $200/Month?”

You have several options:

Buy Less Coverage:

- $10,000 instead of $15,000 saves about $60-80/month

- $7,500 covers basic funeral costs

- Something is better than nothing

Shop Multiple Companies:

- Rates vary 25-40% between companies

- Globe Life often cheapest

- 30 minutes of comparison shopping = $30-60/month savings

Look for Discounts:

- Annual payment saves 5-10%

- Some companies offer non-smoker discounts even at 80+

- AARP membership discounts (where available)

Consider Waiting a Few Months:

- Save up for first few months of premiums

- But remember: delaying until 81 increases rates 8-12%

Real Budget Example: Mary, 82, couldn’t afford $185/month for $15,000. She bought $10,000 for $128/month instead—perfectly adequate for her funeral expenses and much better than no coverage.

“What Happens During the Waiting Period?”

This confuses people more than anything else, so let me make it crystal clear.

Guaranteed Issue Waiting Period (2-3 Years):

If You Pass From Natural Causes (Years 1-2):

- Your beneficiaries receive 100% of premiums paid

- Plus 10% interest on those premiums

- Not the full death benefit yet

- Example: Paid $200/month for 18 months = $3,600 + 10% = $3,960 returned

If You Pass From Accident (Any Time):

- Full death benefit paid immediately

- From day one of policy

- No waiting period for accidents

- Example: Car accident, fall, any accidental death = full $15,000

After Waiting Period Expires (Year 3+):

- Full death benefit for ANY cause

- Natural causes, accidents, anything

- No restrictions

- Example: After 3 years, whatever happens = full $15,000

Important: Simplified issue policies typically have NO waiting period—full coverage from day one.

“Can I Change My Beneficiary Later?”

Yes, absolutely, as often as you want.

How to Change Beneficiaries:

- Call your insurance company

- Request beneficiary change form

- Complete and return (online, mail, or fax)

- Processed within 1-2 business days

- Keep confirmation for your records

When You Should Update:

- Original beneficiary passes away

- Family relationships change

- You get married or divorced

- Grandchildren born

- You simply change your mind

No Permission Needed: You don’t need your current beneficiary’s approval to change to someone else (unless you’ve designated them “irrevocable,” which is rare).

Real Example: James, 83, originally named his wife as beneficiary. When she passed away six months later, he changed his beneficiary to his daughter with one phone call. Simple and quick.

“What If I Outlive the Waiting Period?”

That’s excellent! That’s exactly what should happen.

After 2-3 years, the waiting period expires and you have full permanent coverage for life. Your premiums never increase, your coverage never expires, and whenever you eventually pass away—whether that’s at 87 or 97—your beneficiaries get the full death benefit.

The waiting period isn’t a limitation on total coverage duration—it’s just about timing in the first 2-3 years. After that, you’re fully covered forever.

“Will My Premiums Increase Every Year?”

No—this is a level premium permanent life insurance policy.

What This Means:

- Premium you pay at 80 stays the same at 81, 82, 83, etc.

- Never increases due to age

- Never increases due to worsening health

- Locked in for life

- If you pay $200/month now, you’ll pay $200/month in 10 years

The Only Exception: If you deliberately change your coverage amount (buy more or reduce coverage), your premium adjusts accordingly. But if you leave your policy alone, the premium stays identical forever.

“Is Life Insurance Money Taxable?”

No—life insurance death benefits are tax-free to beneficiaries.

What Your Beneficiaries Receive:

- 100% of death benefit

- No federal income tax

- No state income tax (in most states)

- Full amount available immediately

Example: Your policy is $15,000. Your daughter receives the full $15,000, pays zero taxes, and can use it immediately for funeral costs, bills, or anything else.

Rare Exception: If your estate is worth over $13.61 million (2024 threshold), estate taxes might apply. This affects less than 0.1% of Americans and almost no seniors buying $10,000-$25,000 policies.

Best Life Insurance Companies for Seniors Over 80

Some life insurance companies are significantly more flexible with older applicants and seniors managing health conditions.

Companies commonly used for seniors over 80 include:

- Mutual of Omaha

- Globe Life

- Gerber Life

- Colonial Penn

- AIG-American General

Mutual of Omaha (Best Overall)

Why They’re Best:

- Accept applicants to age 85

- A+ financial strength rating

- 115+ years in business

- Excellent customer service

- Both guaranteed and simplified issue

- Competitive rates

Coverage: $2,000-$50,000

Sample Rate (Female 80, $15,000): $178/month

Application: Online or phone, instant approval for guaranteed issue

Strengths: Most balanced option—good rates, strong company, easy process

Globe Life (Best for Low Rates)

Why They’re Best for Budget:

- Often lowest premiums available

- Accept to age 85

- A financial rating

- Simple application

- Fast approval

Coverage: $5,000-$50,000

Sample Rate (Female 80, $15,000): $165/month

Application: Online, phone, or mail

Strengths: Best choice if lowest premium is top priority

Consideration: Customer service reviews are mixed

Gerber Life (Best for Small Policies)

Why They’re Best for Small Coverage:

- Specialize in $5,000-$25,000 policies

- Very simple application

- Accept to age 80

- A financial rating

- Budget-friendly

Coverage: $5,000-$25,000

Sample Rate (Female 80, $10,000): $115/month

Application: 3-minute phone application

Strengths: Perfect if you only need $10,000-$15,000 for funeral

Colonial Penn (Best Brand Recognition)

Why Seniors Trust Them:

- Heavy advertising creates familiarity

- Accept to age 85

- A financial rating

- Guaranteed acceptance

- Units pricing (buy in $5,000 increments)

Coverage: Varies by units purchased

Sample Rate (Female 80, $15,000): $198/month

Application: Online or phone

Strengths: Brand comfort for seniors who recognize the name

Consideration: Rates higher than competitors, but some prefer familiar brands

AIG/American General (Best for Health Conditions)

Why They’re Best for Complicated Health:

- Excellent underwriters who understand senior health

- Accept to age 85

- A+ financial rating

- Both policy types available

- Good at approving borderline cases

Coverage: $5,000-$100,000

Sample Rate (Female 80, $15,000 simplified issue): $125/month

Application: Phone interview recommended for health questions

Strengths: If you’re borderline for simplified issue, try AIG

👉 Compare the best life insurance companies for seniors with health problems to explore your options.

Tips for Getting the Best Rate Over 80

Even though rates are higher at 80+, you can still save significant money with smart strategies.

Tip #1: Apply Before Your Next Birthday

Every year dramatically increases premiums:

- 80 to 81: 8-12% increase

- 81 to 82: 8-12% increase

- 82 to 83: 8-12% increase

Action: If you’re 80 and 6 months, apply now before turning 81. You’ll lock in 8-12% lower rates for life.

Tip #2: Compare 5+ Companies

Rate differences are substantial:

- Cheapest: Globe Life $165/month

- Most Expensive: Colonial Penn $198/month

- Savings: $33/month = $396/year

Action: Spend 2 hours getting quotes. Save $400+ annually forever.

Tip #3: Buy Only What You Need

Don’t overbuy coverage:

- $15,000 at $178/month

- $10,000 at $120/month

- Savings: $58/month = $696/year

Action: Calculate actual needs (funeral + small debts). Don’t buy extra “just in case.”

Tip #4: Consider Annual Payment

Some companies offer discounts:

- Monthly: $178 × 12 = $2,136/year

- Annual: $2,030/year

- Savings: $106/year

Action: If you can afford the lump sum, pay annually.

Tip #5: Try Simplified Issue First

If you’re in decent health:

- Guaranteed: $178/month

- Simplified: $125/month

- Savings: $53/month = $636/year

Action: Apply for simplified issue at 80-82 if your health is stable. Switch to guaranteed if declined.

Tip #6: Quit Smoking (If Possible)

Even at 80, smoking status matters:

- Non-smoker: $178/month

- Smoker: $305/month

- Savings: $127/month = $1,524/year

Action: If you can quit for 12-24 months, reapply as non-smoker.

Tip #7: Don’t Wait

Every month you delay:

- Rates increase incrementally

- Your health might worsen

- You might age into next birthday bracket

- Life insurance protection missing

Action: If you’ve decided you need coverage, apply this week.

Real Stories from Seniors Over 80

Nothing explains life insurance for seniors over 80 better than real experiences. Here are actual stories from people I’ve worked with (names changed for privacy).

Margaret’s Story – Age 84

Situation: Margaret was 84 with COPD, diabetes, and used oxygen occasionally. She was convinced no company would insure her. Her biggest worry was leaving funeral debt for her daughter, who was on a tight budget.

What She Did:

- Applied for guaranteed issue from Mutual of Omaha

- $12,000 coverage

- Got instant approval online (no health questions)

- Premium: $195/month

The Outcome: Margaret said, “I couldn’t believe it was that easy. I kept waiting for them to call and ask about my health, but they never did. Now I sleep better knowing Sarah won’t have to scramble for funeral money.”

Two Years Later: Margaret is still with us at 86, paying her $195/month, and her coverage is now fully active (passed the waiting period).

Robert’s Story – Age 81

Situation: Robert’s wife passed away unexpectedly, and he saw firsthand how final expenses added up. He was 81, relatively healthy, and wanted $20,000 to cover not just funeral but also any final medical bills.

What He Did:

- Got quotes from six companies

- Applied for simplified issue (answered health questions)

- Approved in 24 hours

- Chose Globe Life at $248/month

- Full coverage from day one (no waiting period)

The Outcome: Robert said, “I probably spent three hours total on this whole thing, and I’m saving about $70 a month compared to guaranteed issue. Worth every minute.”

One Year Later: Robert is 82 now, still paying the same $248/month, and his coverage is fully in force.

Dorothy and Frank’s Story – Ages 82 and 83

Situation: This married couple wanted coverage for both of them. Frank had heart disease, Dorothy was relatively healthy. They wanted $15,000 each.

What They Did:

- Dorothy applied for simplified issue (got better rate)

- Frank applied for guaranteed issue (accepted with heart condition)

- Dorothy: $138/month

- Frank: $275/month

- Combined: $413/month for $30,000 total coverage

The Outcome: Frank said, “We thought about just getting one policy for both of us, but learned that doesn’t work—you need separate policies. Now we each have coverage, and whichever of us goes first, the other won’t be stuck with funeral costs.”

Helen’s Story – Age 86

Situation: At 86, Helen was told by two companies she was “too old.” She was devastated and nearly gave up. Then she found Liberty Bankers, which accepts applicants to age 89.

What She Did:

- Applied for guaranteed issue at Liberty Bankers

- $10,000 coverage

- Instant approval

- Premium: $298/month

The Outcome: Helen said, “I was so relieved. Everyone told me I’d waited too long, but I found a company that wanted my business. The premium is high, but worth it for peace of mind.”

The Lesson: If one company says you’re too old, try others. Maximum ages vary by company.

James’s Story – Age 80 (Just Turned)

Situation: James turned 80 last month and immediately started shopping for insurance. His wife convinced him not to wait until his health declined.

What He Did:

- Applied within weeks of turning 80

- Guaranteed issue at Mutual of Omaha

- $15,000 coverage

- Premium: $210/month (male rates are higher)

The Outcome: James said, “My buddy waited until he was 83, and he’s paying almost $100 more per month than me for the same coverage. I’m glad my wife pushed me to do this early.”

The Lesson: Don’t procrastinate. Every year increases costs significantly.

[IMAGE PLACEMENT #6: Success story highlights with senior photos and quotes]

Frequently Asked Questions

Can you really get life insurance at age 80?

Yes, absolutely. Multiple major insurance companies accept applicants at age 80, including Mutual of Omaha, Globe Life, Colonial Penn, AIG, and Gerber Life.

Most companies accept applicants up to age 85, and some even accept up to age 89. Life insurance for 80 year olds is readily available through guaranteed issue policies that don’t require medical exams or health questions.

These policies are specifically designed for seniors over 80 and provide coverage amounts from $5,000 to $50,000. The application process is simple, approval is often instant, and premiums never increase once you’re approved.

At age 80, you can typically choose between guaranteed issue (no health questions, 2-year waiting period, higher premiums) or simplified issue if you’re in good health (health questions required, no waiting period, lower premiums).

The key is applying with companies that specialize in senior coverage rather than traditional insurers focused on younger buyers.

How much does life insurance cost for an 80 year old?

Life insurance over 80 costs vary based on coverage amount, gender, smoking status, and policy type.

For a typical $15,000 guaranteed issue policy, an 80-year-old female non-smoker pays approximately $165-$245 per month ($1,980-$2,940 annually), while an 80-year-old male non-smoker pays approximately $228-$298 per month ($2,736-$3,576 annually).

For simplified issue policies (if you qualify with good health), rates are 30-50% lower: females pay around $115-$165/month and males pay around $155-$215/month.

Coverage amount directly affects price—$10,000 costs about 67% of these rates, while $25,000 costs about 167% of these rates. Rates increase 8-12% with each birthday, so an 81-year-old pays more than an 80-year-old.

Shopping between companies can save $30-60/month because rates vary significantly between insurers for identical coverage. Smokers pay 60-100% more than non-smokers at any age.

What is guaranteed issue life insurance?

Guaranteed issue life insurance is a type of permanent life insurance that accepts everyone regardless of health conditions, with no medical exam and no health questions asked.

For life insurance for seniors over 80, this is the most common type purchased because it provides instant approval—if you’re within the age range (typically 50-85 or 50-89), you’re automatically approved.

The trade-off is a 2-3 year waiting period: if you pass away from natural causes in the first 2-3 years, beneficiaries receive premiums paid plus 10% interest rather than the full death benefit; however, accidental death pays full benefit from day one.

After the waiting period expires, full coverage applies for any cause of death. Premiums are 30-50% higher than simplified issue because insurers accept everyone including those with serious health conditions like oxygen use, recent cancer, heart disease, or COPD.

Coverage amounts typically range from $5,000 to $50,000, premiums never increase, and policies last your entire life. This makes guaranteed issue perfect for seniors with health conditions who want absolute certainty of approval.

Is there life insurance for seniors over 85?

Yes, several companies offer life insurance for seniors over 85, though options are more limited than at age 80-84. Companies accepting age 85 include Mutual of Omaha, Globe Life, Colonial Penn, and AIG (all accept to age 85).

Liberty Bankers Life accepts applicants up to age 89, making them an option for the oldest seniors. At age 85+, virtually all policies are guaranteed issue (no health questions) because simplified issue is rarely available.

Premiums are significantly higher than at younger ages—a female 85 might pay $245-$365/month for $15,000 coverage, while a male 85 pays $342-$458/month. Coverage amounts are typically capped at $25,000-$35,000 maximum at age 85+, compared to $50,000 maximums at younger ages.

The 2-3 year waiting period still applies, and application processes remain simple. The key is applying before age 86 or finding the few companies like Liberty Bankers that accept older applicants. If you’re 85 or approaching it, don’t delay—your options decrease with each passing year.

What happens if I’m declined for life insurance at age 80?

Being declined at age 80 is rare, but if it happens, you have several options. First, understand WHY you were declined—if you applied for simplified issue and were declined due to health questions, immediately apply for guaranteed issue instead (guaranteed issue accepts everyone and can’t decline you based on health).

If you were declined because you exceeded the maximum age (some companies cap at 80, others at 85), apply with a different company that has higher age limits like Liberty Bankers (accepts to 89).

If you were declined because you’re currently in hospice or have a terminal diagnosis with life expectancy under 12 months, your options are very limited, though some companies still offer small graded benefit policies.

If you were declined for administrative reasons (identity verification issues, payment problems), resolve those issues and reapply. In rare cases where traditional life insurance isn’t available, consider: (1) Pre-need funeral insurance purchased directly from funeral homes, (2) Final expense riders on existing policies, or (3) Burial trusts or savings accounts as alternatives.

The important thing is NOT giving up after one decline—guaranteed issue policies from major companies accept the vast majority of 80-year-old applicants.

Do I need a medical exam to get life insurance at 80?

No, you do NOT need a medical exam for life insurance for elderly over 80. All policies designed for seniors over 80 are either guaranteed issue or simplified issue, both of which specifically exclude medical exams.

You won’t have blood tests, urine samples, doctor visits, or physical examinations. Guaranteed issue policies require no health information at all—not even a single question about your health conditions, medications, or medical history.

Simplified issue policies ask 5-10 basic health questions (like “Have you been hospitalized in the past 2 years?” or “Do you currently use oxygen?”) but still don’t require any medical exam or verification from doctors.

This no-exam approach makes sense because insurance companies understand that seniors over 80 typically have health conditions and often have difficulty visiting exam locations.

The application can be completed entirely online or by phone from your home, with approval in minutes (guaranteed issue) or 24-48 hours (simplified issue).

The trade-off for no medical exam is higher premiums compared to fully underwritten policies, but for most seniors over 80, avoiding the exam is worth the extra cost.

Will my medications or health conditions disqualify me?

No, with guaranteed issue life insurance, medications and health conditions cannot disqualify you. Guaranteed issue accepts everyone regardless of what medications you take or what conditions you have—diabetes, heart disease, cancer, COPD, oxygen use, stroke history, kidney disease, Alzheimer’s, and anything else.

You don’t even report these conditions on the application because no health questions are asked. For simplified issue policies (available mainly for healthier seniors 80-82), health questions are asked and certain conditions may disqualify you: current oxygen use, recent cancer diagnosis (within 5 years typically), recent hospitalizations (within 2 years), terminal illness, or currently receiving hospice care often result in decline for simplified issue.

However, if declined for simplified issue, you simply switch to guaranteed issue and get approved immediately. The only near-universal disqualifiers across all policy types are: currently in hospice care or terminal diagnosis with life expectancy under 12 months.

Beyond those rare exceptions, guaranteed issue ensures that seniors over 80 can get coverage regardless of their health conditions or medication regimen.

How long does the waiting period last?

The waiting period for guaranteed issue policies is typically 2-3 years (varies slightly by company and state). During this waiting period:

(1) If you pass away from natural causes (illness, disease, organ failure, etc.), your beneficiaries receive 100% of premiums paid plus 10% interest, not the full death benefit;

(2) If you pass away from accidental causes (car accident, fall, any accident), your beneficiaries receive the full death benefit from day one;

(3) After the waiting period expires (at the 2 or 3 year mark), full coverage applies for ANY cause of death—natural, accidental, or any other reason.

The waiting period is insurance company protection against “adverse selection” (people applying only when they know death is imminent). It’s not a limitation on total coverage duration—after the waiting period expires, you have full permanent coverage for the rest of your life, whether that’s 5 more years or 25 more years.

Simplified issue policies typically have NO waiting period—you get full coverage from day one. Some guaranteed issue policies offer modified waiting periods where a percentage of the death benefit is paid in year 1 (maybe 25%) and year 2 (maybe 50%), with full benefit in year 3+.

Can I change my beneficiary anytime?

Yes, you can change your beneficiary anytime for any reason without restrictions (unless you’ve designated an “irrevocable beneficiary,” which is very rare).

To change beneficiaries: contact your insurance company by phone, online portal, or mail; request a beneficiary change form; complete it with new beneficiary information (full name, date of birth, Social Security number, relationship); submit it; and receive confirmation within 1-2 business days.

You don’t need permission from your current beneficiary to remove or replace them. You can name multiple beneficiaries and split proceeds any way you want (50% to child A, 50% to child B, or any other split).

You should update beneficiaries after major life events: death of original beneficiary, marriage, divorce, birth of grandchildren, family relationship changes, or simply changing your mind. It’s smart to name both primary beneficiaries (first in line) and contingent beneficiaries (backup if primary is deceased).

If you don’t keep beneficiaries current, proceeds may go to unintended recipients or to your estate (causing probate delays and extra costs). Most insurance companies make this process very simple with online forms or quick phone calls.

Is the death benefit taxable to my beneficiaries?

No, life insurance death benefits are NOT taxable as income to beneficiaries in the vast majority of cases. Your beneficiaries receive the full death benefit amount completely tax-free—no federal income tax, no state income tax (in most states), and no inheritance tax in most situations.

For example, if your policy pays $15,000, your beneficiaries receive the complete $15,000 to use for funeral expenses, bills, or anything else without any tax obligations. This tax-free treatment applies regardless of policy size, your age, or your beneficiaries’ ages. The rare exceptions are:

(1) If your estate exceeds $13.61 million (2024 threshold), estate taxes might apply, but this affects less than 0.1% of Americans and essentially no seniors buying $10,000-$25,000 final expense policies;

(2) If the death benefit earns interest before being paid out (rare with prompt claims processing), the interest portion may be taxable;

(3) If you transfer policy ownership within 3 years of death for estate planning purposes, it may be included in your estate. For the vast majority of seniors over 80 purchasing standard final expense insurance, beneficiaries receive 100% of the death benefit tax-free with no IRS reporting requirements.

If you’re struggling with premiums for life insurance for seniors over 80, you have several options before canceling your policy. First, reduce your coverage amount—switching from $15,000 to $10,000 saves approximately $50-80/month; you’ll still have funeral coverage while reducing financial strain.

Second, shop for a cheaper company—rates vary 25-40% between insurers, so you might find identical coverage $30-60/month cheaper elsewhere (you can switch policies by buying a new one, then canceling the old one once approved).

Third, look for annual payment discounts—paying yearly instead of monthly sometimes saves 5-10%.

Fourth, consider a premium waiver at certain ages or conditions (some policies offer this).

Fifth, check if your policy has accumulated any cash value that could help pay premiums temporarily. Sixth, reduce to “reduced paid-up insurance” where you stop paying premiums and accept a lower death benefit permanently (some policies offer this option).

As a last resort, if you must cancel: (1) Make sure new coverage is approved before canceling old coverage; (2) Understand that getting new coverage at age 81+ will cost more than your current 80-year-old rates; (3) Consider pre-need funeral insurance as an alternative.

Never let a policy lapse silently—contact your insurance company to discuss options.

Can married couples get one joint policy?

No, life insurance for seniors over 80 doesn’t typically offer true “joint life” policies where both spouses are covered under a single policy.

Each person needs their own individual policy because life insurance insures one person’s life, not two. However, married couples absolutely should both have coverage—each spouse gets their own policy with their own coverage amount, premiums, and beneficiary designation.

Many couples make the mistake of only insuring one spouse (usually the husband), which leaves the surviving spouse without coverage for their own funeral when the time comes.

The best approach is: (1) Each spouse gets their own policy for their own funeral/final expenses; (2) Each spouse names the other as primary beneficiary; (3) Both policies have contingent beneficiaries (usually adult children) in case both spouses pass in a short timeframe; (4) Coverage amounts can differ based on each person’s individual needs and financial situation.

Some insurers offer small premium discounts when both spouses apply with the same company, but these are modest (5-10% typically).

While couples policies are rare, the advantage of separate policies is flexibility—you can have different coverage amounts, different policy types, and coverage continues for the surviving spouse.

Budget the premiums as a combined household expense rather than separate obligations.

How quickly will my family receive the money?

Life insurance death benefit payments typically take 30-60 days from the date of claim submission, though simple cases sometimes pay faster (as quick as 7-14 days) and complicated cases can take 60-90 days.

The timeline works like this: (1) Beneficiary notifies insurance company of death (can be same day or weeks later); (2) Insurance company sends claim forms (1-3 days); (3) Beneficiary submits completed forms with death certificate (varies based on how quickly they act); (4) Insurance company verifies claim and reviews policy (7-30 days for most cases); (5) Payment issued via check or direct deposit.

For faster processing, beneficiaries should: submit claims immediately rather than waiting, provide certified death certificates (not photocopies), ensure beneficiary information is current and accurate, complete all forms fully and accurately, and respond promptly to any insurer requests.

Claims are delayed when: beneficiary information is outdated or incorrect, death occurred during the waiting period (requires calculating premiums paid plus interest), death is from suicide within 2 years of policy start (most policies exclude this), death circumstances are unusual and require investigation, or required paperwork is incomplete.

Most claims are straightforward and pay within 30-45 days, giving families money for immediate funeral costs. Some funeral homes will wait for insurance proceeds rather than requiring upfront payment if beneficiaries provide proof of policy.

Taking Action: Your Next Steps

You’ve learned everything about life insurance for seniors over 80. Now it’s time to actually get your coverage in place.

This Week:

Monday-Tuesday: Calculate and Compare

- Determine how much coverage you need ($10K, $15K, $20K, $25K?)

- Get quotes from 5+ companies

- Write down rates for easy comparison

- Check A.M. Best ratings (look for A- or higher)

Wednesday-Thursday: Make Decision

- Choose guaranteed issue or simplified issue

- Select the company with best combination of price and strength

- Decide on coverage amount that fits budget

- Prepare beneficiary information

Friday: Apply

- Complete application (5-20 minutes)

- Pay first premium

- Request confirmation email

- Save all documentation

This Month:

Week 2: Receive and Review Policy

- Policy documents arrive by mail/email

- Read everything carefully

- Verify all information is correct

- Use 30-day free look period to review

Week 3: Set Up Payments

- Establish automatic monthly payments

- Verify payment processed correctly

- Keep copy of payment confirmation

Week 4: Inform Family

- Tell your beneficiaries about the policy

- Explain where documents are kept

- Give them insurance company contact information

- Consider giving them a copy of policy documents

Ongoing:

Every Year:

- Verify payment is processing correctly

- Review beneficiary designations (update if needed)

- Confirm coverage still meets needs

- Check company financial ratings haven’t declined

Don’t Procrastinate: Every month you wait:

- Rates increase incrementally

- Your health could worsen

- You edge closer to next birthday (8-12% rate increase)

- Your family remains unprotected

The best time to buy life insurance was 10 years ago. The second-best time is today.

Final Thoughts

Getting life insurance for seniors over 80 is easier than you probably expected when you started reading this guide. You don’t need perfect health. You don’t need a medical exam. And you don’t need to navigate a complicated process.

What you need is simple: decide how much coverage, get a few quotes, choose guaranteed or simplified issue, apply, and pay your first premium. That’s it.

I’ve seen too many families struggle with unexpected funeral costs, scrambling to gather $10,000-$15,000 while grieving. I’ve watched adult children max out credit cards or drain savings to cover expenses their parent could have easily insured for $150-200 per month.

Don’t let that be your family.

Whether you’re 80, 82, or 85, coverage is available right now. The companies I’ve mentioned in this guide—Mutual of Omaha, Globe Life, Gerber Life, and others—approve thousands of seniors your age every single month. They want your business. They’ve designed products specifically for your situation.

Take action this week. Get those quotes. Choose a policy. Apply.

Your family will thank you for the peace of mind, and you’ll sleep better knowing everything is handled. That’s what life insurance is really about—not money, but love. Love for the people you’ll leave behind and the desire to make their difficult time just a little bit easier.

You can do this. And you should.

Disclaimer: This article provides general information about life insurance for seniors over 80 and should not be considered insurance, financial, or legal advice. Insurance products, rates, company policies, and availability vary by state, individual circumstances, age, health status, and are subject to change without notice. Premium rates and policy details quoted are approximate ranges for illustration purposes and may not reflect actual rates available to you. Always verify current information directly with insurance companies, review complete policy documents before purchasing, and compare multiple quotes from licensed insurers. Waiting periods, coverage amounts, maximum ages, and underwriting requirements vary by company and state. Consult with licensed insurance professionals regarding your specific situation. This guide is not affiliated with or endorsed by any insurance company mentioned. Information is current as of publication date but insurance products and company offerings change frequently. No guarantee is made regarding policy approval, premium rates, or coverage availability for any individual applicant.