Life Insurance for Seniors with a Stroke or TIA History: What You Need to Know (2026 Guide)

Posted in Life Insurance w/ Pre-existing Conditions on January 16, 2026 last updated on May 27, 2026

Posted in Life Insurance w/ Pre-existing Conditions on January 16, 2026 last updated on May 27, 2026

Can Seniors Get Life Insurance After a Stroke?

Yes, seniors can often qualify for life insurance after a stroke, especially if they have recovered well and remained stable afterward. Approval and rates depend on the type of stroke, recovery progress, time since the event, and overall health.

If you’re looking for life insurance for seniors with a stroke or TIA history, the good news is this:

having a stroke or mini stroke does not automatically disqualify you from coverage.

However, the type of policy you qualify for, the cost, and the approval process depend on:

- How long ago the stroke or TIA occurred

- Whether there are lingering effects

- Overall health stability since the event

This guide explains what seniors need to know, what options are realistic, and how to avoid common (and costly) mistakes. Some life insurance companies are significantly more flexible with stroke survivors and applicants managing multiple cardiovascular conditions.

Understanding Stroke and TIA (In Plain English)

Before insurers look at coverage, they want to understand risk.

What is a stroke?

A stroke occurs when blood flow to part of the brain is interrupted, often due to:

- A blood clot (ischemic stroke)

- A ruptured blood vessel (hemorrhagic stroke)

Strokes can cause long-term complications depending on severity.

What is a TIA (Transient Ischemic Attack)?

A TIA, often called a mini-stroke, causes stroke-like symptoms that usually resolve within 24 hours.

While symptoms may be temporary, insurers treat a TIA seriously because it increases the risk of a future stroke.

What Type of Stroke Did You Have?

Insurance companies evaluate different types of strokes differently because recurrence risk and long-term complications can vary significantly.

Common stroke types include:

- Ischemic stroke

- Hemorrhagic stroke

- Transient ischemic attack (TIA or mini-stroke)

Underwriters review:

- Severity

- Recovery

- Neurological deficits

- Hospitalizations

- Rehabilitation

- Recurrence risk

Applicants with a mild TIA and full recovery often receive better underwriting outcomes than applicants with major hemorrhagic strokes.

How a Stroke or TIA Affects Life Insurance Premium for Seniors

When evaluating life insurance for seniors with a stroke or TIA history, insurers focus on risk stability, not just diagnosis.

Key factors insurers look at:

- Time since the stroke or TIA

- Number of strokes or TIAs

- Severity and type of stroke

- Lingering symptoms (speech, mobility, cognition)

- Medications (blood thinners, BP meds)

- Blood pressure contol

- Cholesterol control

- Lifestyle changes since the event

- Age at time of stroke

- Smoking Status

Time matters.

A stroke that occurred 10 years ago with full recovery is viewed very differently than one within the last 12–24 months.

| Stroke Situation | Typical Underwriting Outcome |

|---|---|

| Mild TIA with full recovery | Moderate to favorable |

| Ischemic stroke over 12 months ago | Moderate rates |

| Recent stroke within 6 months | Possible postponement |

| Stroke + diabetes or heart disease | Higher premiums |

| Severe neurological deficits | Simplified or guaranteed issue |

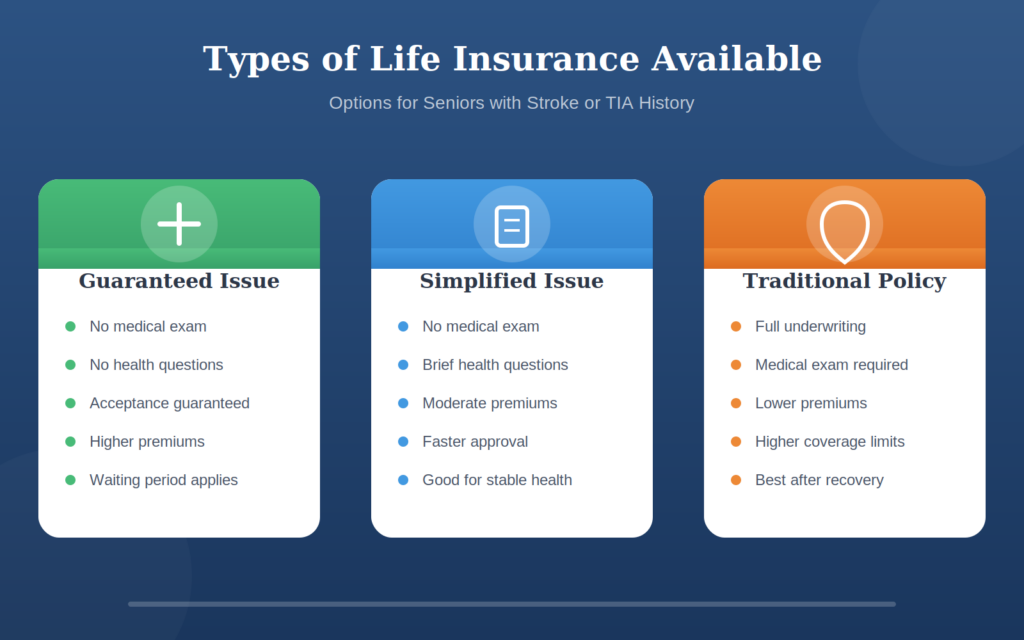

Can Seniors with a Stroke or TIA still get Life Insurance?

Yes — but policy type matters.

Seniors with a stroke or TIA history typically qualify for one (or more) of the following:

- Simplified issue life insurance

- Final expense insurance

- Guaranteed issue life insurance

- Traditional life insurance (in limited cases)

Let’s break these down.

Best Life Insurance Options for Seniors with a Stroke or TIA History

1) Simplified Issue Life Insurance (Often the Best Value)

Simplified issue life insurance does not require a medical exam but does ask health questions.

Some seniors with a stroke or TIA history do qualify, especially if:

- The event occurred several years ago

- There has been no recurrence

- Recovery was strong

- Conditions like blood pressure are controlled

Pros

- No medical exam

- Faster approval

- Better pricing than guaranteed issue

- Often permanent coverage

Cons

- Not everyone qualifies

- Coverage amounts may be capped

Best for:

Seniors with a remote or well-managed stroke/TIA history.

2) Final Expense Insurance (Most Common Choice)

For many seniors, final expense insurance is the most realistic option after a stroke or TIA.

It’s designed for:

- Funeral costs

- Medical bills

- Small debts

- End-of-life expenses

Why it works well

- Smaller coverage amounts match real needs

- Often no medical exam

- Simplified or guaranteed approval available

- Permanent coverage (does not expire)

Best for:

Seniors who want certainty, simplicity, and lifelong coverage.

3) Guaranteed Issue Life Insurance (When Health Is Severe)

If a senior:

- Has had multiple strokes

- Has significant residual impairments

- Has been declined elsewhere

Guaranteed issue life insurance may be the safest option.

What to know

- No medical exam

- No health questions

- Approval guaranteed (within age limits)

- Typically includes a waiting period (often 2–3 years)

Best for:

Seniors with serious or recent stroke history who want guaranteed approval.

4) Traditional Life Insurance (Limited Cases)

Some seniors may still qualify for traditional term or whole life insurance if:

- The stroke or TIA was mild

- It occurred many years ago

- Recovery was complete

- Overall health is excellent

However, this is less common, especially after age 65.

Rate Charts: Life Insurance for Seniors With Stroke or TIA History (2026 Estimates)

These are illustrative ranges, not quotes. Actual rates vary by age, state, severity, and insurer.

Final Expense Insurance (Stroke/TIA History)

Coverage: $10,000

| Age | Monthly Premium Range |

|---|---|

| 60 | $55–$85 |

| 65 | $65–$100 |

| 70 | $85–$130 |

| 75 | $115–$175 |

| 80 | $155–$240 |

Final Expense Insurance (Higher Coverage)

Coverage: $20,000

| Age | Monthly Premium Range |

|---|---|

| 60 | $95–$145 |

| 65 | $110–$170 |

| 70 | $145–$220 |

| 75 | $190–$290 |

| 80 | $250–$380 |

Guaranteed Issue Life Insurance (Stroke/TIA)

Coverage: $10,000

| Age | Monthly Premium Range |

|---|---|

| 60 | $70–$105 |

| 65 | $85–$125 |

| 70 | $110–$165 |

| 75 | $150–$225 |

| 80 | $200–$310 |

👉 Want to compare companies that work best for stroke survivors? Explore personalized options in under 60 seconds.

Best Life Insurance Companies for Seniors With a Stroke or TIA History

Finding the right company is just as important as choosing the right policy type when it comes to life insurance for seniors with a stroke or TIA history. Some insurers have more experience evaluating higher-risk applicants, more flexible underwriting guidelines, and dedicated simplified or guaranteed issue products that senior applicants with stroke history often qualify for.

Below are some of the most senior-friendly life insurance companies and options to consider — especially if health history includes a stroke or TIA. These carriers are known for offering products that help seniors get coverage even after a stroke/TIA, with competitive pricing and approval odds that match your situation.

1. Mutual of Omaha

What they’re known for:

Mutual of Omaha often ranks as a strong choice for seniors with health issues because it offers a range of final expense and simplified issue life insurance programs. They’re experienced with underwriting risks for older adults and have multiple product options that do not require a medical exam, which can make approval easier for seniors with a stroke or TIA history.

Why seniors with stroke/TIA history like them:

- Simplified issue and final expense policies available

- Competitive pricing for smaller permanent coverage

- Reliable customer support for older applicants

Best for: Seniors needing simplified issue or final expense coverage with flexible approval.

2. AIG (American International Group)

What they’re known for:

AIG offers both traditional and simplified issue permanent life insurance options. While some of their larger policies require underwriting, their simplified products are accessible without a medical exam — a plus for many seniors with stroke or TIA history.

Why seniors with stroke/TIA history like them:

- Whole life policies with simplified underwriting

- Helpful tools to understand eligibility early

- Larger brand with flexible options for seniors

Best for: Seniors who want permanent coverage without the hassle of exam-based underwriting.

3. Gerber Life Insurance

What they’re known for:

Gerber Life offers final expense products that can be easier to qualify for than traditional policies. Their simplified underwriting can help seniors with a stroke or TIA history get coverage even if traditional life insurance was declined.

Why seniors with stroke/TIA history like them:

- Final expense focus with gentle underwriting

- Straightforward application process

- Known for family-oriented customer service

Best for: Seniors who want final expense coverage with a clear, friendly application experience.

4. Transamerica

What they’re known for:

Transamerica offers a variety of life insurance products, including simplified issue permanent coverage and term options. Their underwriting process for simplified policies tends to be favorable for seniors who have had prior health challenges.

Why seniors with stroke/TIA history like them:

- Good range of coverage amounts

- Simplified issue options for easier approval

- Traditional and permanent coverage availability for those who qualify

Best for: Seniors who want the option to compare simplified and traditional choices with one insurer.

5. Foresters Financial

What they’re known for:

Foresters Financial combines simplified issue life insurance with member benefits that can add value over time. They typically accept older applicants with controlled health issues and provide flexible coverage for smaller permanent needs.

Why seniors with stroke/TIA history like them:

- Simplified issue whole life options

- Membership benefits (educational resources, community perks)

- Good support for first-time insurance buyers

Best for: Seniors who want permanent coverage plus additional member value.

How to Choose From These Companies (Stroke/TIA Focused)

When comparing options for life insurance for seniors with a stroke or TIA history, consider these important factors:

Underwriting Flexibility

Look for companies with:

- Simplified issue policies

- A track record of approving higher-risk applicants

- No medical exam or limited health questions

These carriers often evaluate stroke or TIA history with a more flexible approach, especially when other health metrics are stable.

Coverage Amount Options

Final expense insurers may cap coverage amounts (e.g., $5,000–$25,000). Traditional insurers may offer higher amounts if your health supports it.

Waiting Periods

Some companies include brief waiting periods on guaranteed issue policies. If peace of mind right now is the goal, that’s okay — just know how it affects benefit timing.

Cost vs Benefit

Seniors with stroke or TIA history often balance cost, approval odds, and coverage. The companies above offer good blends of these factors, but a side-by-side quote comparison is always the best way to see what works for your exact situation.

How Long Should You Wait to Apply After a Stroke?

Many life insurance companies prefer applicants to wait after a stroke before applying for traditional coverage. The waiting period allows insurers to evaluate recovery, recurrence risk, and long-term stability.

Typical guidelines:

- TIA: 3–6 months

- Ischemic stroke: 6–12 months

- Hemorrhagic stroke: 12+ months

How Multiple Health Conditions Affect Life Insurance After a Stroke

Many seniors who have experienced a stroke also manage other medical conditions that can affect life insurance approval and pricing.

Insurance companies usually evaluate your overall health profile, not just the stroke itself. The combination of conditions often plays a major role in underwriting decisions and premium costs.

Common health conditions that frequently occur alongside stroke include:

- High blood pressure

- Diabetes

- Atrial fibrillation (AFib)

- Heart disease

- Sleep apnea

- COPD

- High cholesterol

- Previous heart attack

For example, a senior who had a mild stroke but has otherwise stable health may receive significantly better rates than someone with multiple uncontrolled cardiovascular conditions.

Insurance underwriters often review:

- Recovery progress after the stroke

- Medication compliance

- Blood thinner use

- Smoking history

- Ongoing neurological symptoms

- Overall cardiovascular stability

Applicants with well-managed conditions and consistent medical follow-up generally have better approval outcomes than applicants with recent complications or unstable health.

Common Stroke-Related Health Scenarios

| Health Combination | Typical Underwriting Outcome |

|---|---|

| Stroke + controlled high blood pressure | Moderate rates |

| Stroke + diabetes | Higher premiums |

| Stroke + AFib and blood thinners | Moderate to higher risk |

| Stroke + heart disease | Increased underwriting scrutiny |

| Stroke + multiple uncontrolled conditions | Simplified or guaranteed issue may be best |

Many seniors are surprised to learn that having multiple medical conditions does not automatically prevent them from qualifying for life insurance.

In many cases, choosing the right insurance company matters more than the diagnosis itself.

Real-Life Experiences (Composite Examples)

Example 1: Stroke History, Managed Health

George, 72, had a mild stroke 6 years ago. He completed rehab and managed his blood pressure carefully. He qualified for a simplified issue final expense policy that gave him immediate coverage without a medical exam.

Example 2: Recent TIA, Fast Coverage Needed

Linda, 68, had a TIA last year. Traditional life insurance declined her. She chose a final expense policy with simplified underwriting, ensuring her family wouldn’t face funeral costs.

Example 3: Multiple Strokes, Guaranteed Approval

Robert, 79, had multiple strokes and mobility issues. Guaranteed issue life insurance gave him approval when other options weren’t available. He understood the waiting period but valued certainty.

Common Mistakes Seniors With Stroke History Make

- Assuming no coverage is available

- Applying for traditional policies too soon

- Skipping simplified issue options

- Overbuying coverage

- Not understanding waiting periods

How Seniors Can Improve Approval Odds After a Stroke or TIA

While you can’t change history, you can strengthen your application by:

- Showing stable blood pressure control

- Taking medications as prescribed

- Avoiding tobacco

- Waiting an appropriate amount of time after the event

- Applying for the right policy type first

FAQ: Life Insurance for Seniors with a Stroke or TIA History

Can seniors get life insurance after a stroke?

Yes. Many seniors qualify for simplified issue, final expense, or guaranteed issue life insurance depending on severity and time since the event.

Is a TIA treated the same as a stroke?

Not exactly. A TIA is often viewed as lower risk, but insurers still consider it a serious warning sign.

How long after a stroke can you apply for life insurance?

It depends on policy type. Some no-exam options are available even shortly after, while traditional policies usually require more time.

Is final expense insurance the best option after a stroke?

For many seniors, yes—because it offers permanent coverage and easier approval.

Usually yes, but rates vary widely based on age, recovery, and policy type.

Final Thoughts

A stroke or TIA changes many things—but it doesn’t eliminate your ability to protect your family. With the right policy type, realistic expectations, and proper guidance, life insurance for seniors with a stroke or TIA history is still achievable.

The key is choosing coverage that fits your health, budget, and goals today—not forcing a policy that isn’t designed for your situation.