Life Insurance After Cancer for Seniors: 2026 Complete Guide

Posted in Life Insurance w/ Pre-existing Conditions on November 25, 2025 last updated on May 7, 2026

Posted in Life Insurance w/ Pre-existing Conditions on November 25, 2025 last updated on May 7, 2026

Can You Get Life Insurance After Cancer?

Yes, seniors can get life insurance after cancer, especially if the cancer is in remission. Approval and rates depend on the type of cancer, stage, treatment history, and how long you’ve been cancer-free.

If you’re a cancer survivor, congratulations—you’ve won one of life’s toughest battles. But now you might be facing a new challenge: getting life insurance. Many cancer survivors believe they’re permanently uninsurable, but that’s simply not true.

Life insurance after cancer for seniors is not only possible, but thousands of cancer survivors secure affordable coverage every year.

The reality is that insurance companies have become much more accommodating to cancer survivors, especially those who’ve been in remission for several years.

Finding affordable life insurance for cancer survivors starts with understanding that your cancer diagnosis doesn’t define your insurability—what matters is the type of cancer, how long you’ve been cancer-free, your prognosis, and your overall health today.

Whether you beat breast cancer five years ago, you’re a recent prostate cancer survivor, or you’re dealing with a more aggressive form of cancer, options exist for your situation. Life insurance after breast cancer and life insurance after prostate cancer are among the most commonly approved cancer survivor cases, but coverage is available for nearly all cancer types.

Finding life insurance after cancer for seniors requires understanding how insurers evaluate cancer history, knowing realistic waiting periods, and choosing the right policy type for your specific cancer and timeline.

In this comprehensive guide, I’ll walk you through everything you need to know about getting life insurance as a senior cancer survivor—from understanding waiting periods by cancer type to finding the most cancer-friendly insurers and realistic costs you can expect.

Can cancer survivors get life insurance? Absolutely yes. The question isn’t whether you can get coverage, but rather which type of policy best fits your cancer history and timeline.

Understanding How Insurance Companies View Cancer

Insurance underwriters evaluate cancer survivors carefully, but they’re not automatically declining everyone with cancer history. They’re looking at specific factors that predict long-term survival and recurrence risk. Understanding these factors is key to finding affordable life insurance after cancer.

What Matters Most to Insurers

Type of Cancer:

Some cancers are viewed much more favorably than others:

Most Favorable (Easier Approval):

- Basal cell or squamous cell skin cancer (non-melanoma)

- Stage 0 or Stage I breast cancer

- Low-grade prostate cancer

- Papillary thyroid cancer

- Stage I cervical cancer

Moderately Favorable:

- Stage II breast cancer

- Stage I-II colorectal cancer

- Low-grade bladder cancer

- Early-stage melanoma

- Stage I lung cancer (rare in early detection)

More Challenging:

- Stage III cancers (any type)

- Leukemia or lymphoma

- Pancreatic cancer

- Stage IV cancers

- Multiple myeloma

- Aggressive melanoma

Time Since Diagnosis and Treatment Completion:

This is often the most important factor:

- Less than 2 years: Guaranteed issue only for most cancers

- 2-5 years: Simplified issue possible for favorable cancers

- 5+ years: Good chances for simplified issue, some traditional policies

- 10+ years: May qualify for standard rates with favorable cancers

Stage at Diagnosis:

- Stage 0 (in situ): Best prognosis, shortest waiting period

- Stage I: Very good prognosis, reasonable waiting periods

- Stage II: Good prognosis, moderate waiting periods

- Stage III: More challenging, longer waiting periods

- Stage IV: Guaranteed issue typically only option

Treatment Type and Response:

- Surgery only: Best case scenario

- Surgery + radiation: Still favorable

- Surgery + chemotherapy: Acceptable if successful

- Ongoing treatment: Very challenging for simplified issue

- Clinical trial medications: Requires case-by-case evaluation

Recurrence History:

- No recurrence: Excellent

- One recurrence, now in remission 5+ years: Possible

- Multiple recurrences: Very challenging

- Active recurrence: Guaranteed issue only

Current Health Status:

- Cancer-free with no complications: Best approval odds

- Cancer-free with treatment side effects: Acceptable

- New health issues from treatment: Complicates approval

- Ongoing monitoring shows no signs: Positive factor

Related Health Conditions:

Cancer survivors often develop other conditions that affect insurance:

- Diabetes from certain treatments (Read about life insurance with diabetes)

- Heart disease from chemotherapy or radiation (Read about life insurance with heart disease)

- High blood pressure (Learn about life insurance with high blood pressure)

- COPD from smoking history (Check out life insurance options for COPD)

Check out our blog post on the best life insurance companies for seniors with health problems.

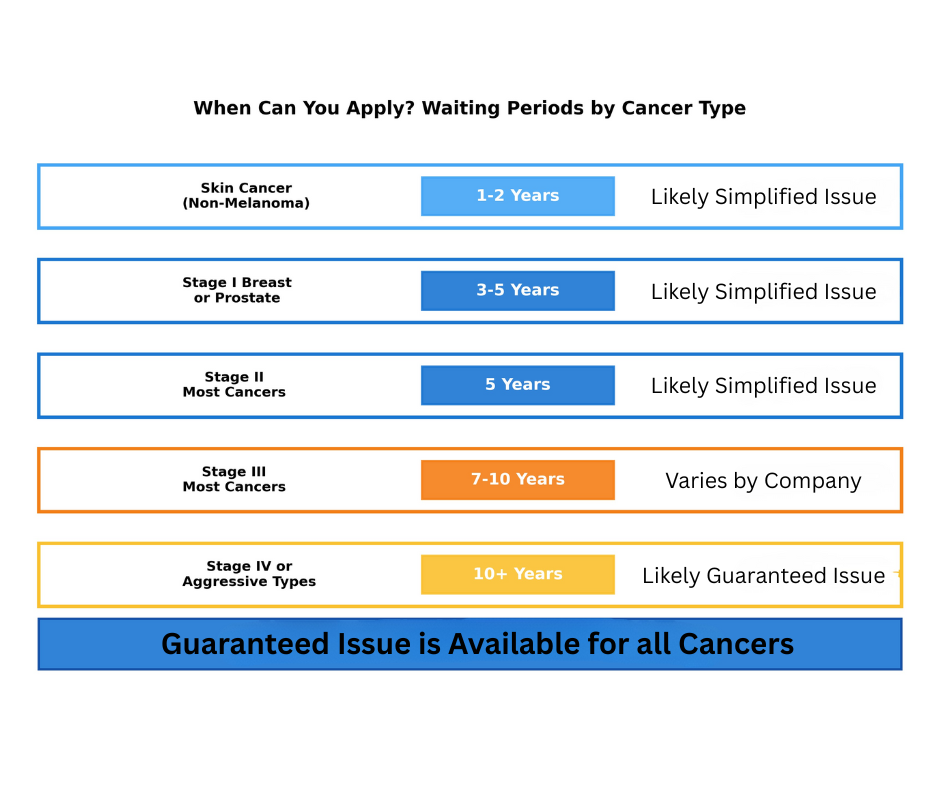

Cancer-Specific Waiting Periods

Different cancers have different typical waiting periods before insurers will consider simplified issue:

Shortest Waiting Periods (1-2 years):

- Basal/squamous cell skin cancer

- Stage 0 breast cancer (DCIS)

- Very low-grade prostate cancer (Gleason 6)

- Papillary thyroid cancer (Stage I)

Moderate Waiting Periods (3-5 years):

- Stage I-II breast cancer

- Stage I colon cancer

- Low-risk prostate cancer (Gleason 7)

- Stage I melanoma

- Stage I cervical cancer

Longer Waiting Periods (5-10 years):

- Stage III breast cancer

- Stage II-III colorectal cancer

- Lymphoma (Hodgkin’s or Non-Hodgkin’s)

- Stage II-III melanoma

- Bladder cancer

Very Long Waiting Periods (10+ years):

- Lung cancer (any stage)

- Pancreatic cancer survivors

- Leukemia

- Brain cancer

- Liver cancer

Your Life Insurance Options as a Cancer Survivor

Option 1: Simplified Issue Life Insurance

Simplified Issue Life Insurance is your target if you’ve been cancer-free for 2-5+ years (depending on cancer type). Great product for life insurance with pre-existing conditions.

Best For:

- 2+ years cancer-free (favorable cancers)

- 5+ years cancer-free (most cancers)

- Early-stage cancers (0, I, or II)

- No recurrence

- Good overall health now

How It Works:

- Answer 10-15 health questions (no medical exam required)

- Questions about cancer type, stage, treatment, and time since completion

- No blood work or medical records review typically

- Decision within 24-48 hours for many applicants

- Coverage from $25,000-$500,000

- No waiting period—full coverage starts immediately

Pros: ✓ No medical exam needed ✓ Much faster than traditional underwriting ✓ Higher coverage amounts than guaranteed issue ✓ Immediate full death benefit ✓ More affordable per dollar of coverage than guaranteed issue

Cons: ✗ Recent cancer (under 2 years) usually disqualifies ✗ Must answer questions honestly about cancer history ✗ Aggressive or late-stage cancers may not qualify ✗ Higher premiums than fully underwritten policies

What to Expect: A 68-year-old woman who completed breast cancer treatment 5 years ago (Stage I) might pay $300-$450/month for $100,000 in simplified issue coverage. A 72-year-old man who completed prostate cancer treatment 3 years ago might pay $400-$550/month for the same coverage. These rates represent typical life insurance for cancer survivors pricing.

Top Companies for Simplified Issue (Cancer Survivors):

- Mutual of Omaha (accepts favorable cancers after 2-3 years)

- AIG (considers early-stage cancers after 5 years)

- Prudential (good for breast and prostate cancer survivors)

- John Hancock (flexible for cancer survivors with good prognosis)

Option 2: Guaranteed Issue Life Insurance

Your safety net will be guaranteed issue life insurance—available regardless of cancer type, stage, or how recent. This definitively answers “can cancer survivors get life insurance?” with a resounding yes for everyone. No exam is necessary to qualify for this life insurance.

Best For:

- Recent cancer diagnosis (within past 2 years)

- Stage III or IV cancer survivors

- Cancer with recurrence history

- Ongoing cancer treatment

- Any cancer that doesn’t qualify for simplified issue

How It Works:

- Request a quote online or by phone

- Provide only basic information (no health questions)

- Cannot be denied for any reason

- Coverage typically $5,000-$25,000

- 2-3 year waiting period for natural death

- Accidental death covered from day one

The Waiting Period:

Years 1-2:

- Death from illness/natural causes: Return of premiums paid plus 10% interest

- Death from accident: Full death benefit paid immediately

Year 3+:

- Full death benefit for any cause of death

Pros: ✓ Absolutely cannot be declined ✓ No questions about cancer type, stage, or treatment ✓ Perfect for recent cancer survivors ✓ Covers final expenses ($7,000-$12,000 average funeral) ✓ Simple application process

Cons: ✗ Lower coverage amounts ✗ Higher cost per dollar of coverage ✗ Waiting period limits immediate benefit ✗ Not suitable for large coverage needs

What to Expect: That same 68-year-old woman with recent cancer (6 months post-treatment) might pay $150-$210/month for just $15,000 in guaranteed issue coverage. It’s more expensive per dollar, but it’s available immediately regardless of cancer status.

Top Companies for Guaranteed Issue:

- Gerber Life (up to $25,000, ages 50-80)

- Mutual of Omaha (up to $25,000, ages 45-85)

- Colonial Penn (well-known guaranteed acceptance)

- Globe Life (straightforward process)

Option 3: Traditional Fully Underwritten (For Long-Term Survivors)

If you’ve been cancer-free for 10+ years with favorable cancer type, you might qualify.

Requirements:

- 10+ years cancer-free (some companies 5+ for very favorable cancers)

- Early-stage cancer only (Stage 0 or I typically)

- No recurrence

- Excellent current health

- Willing to undergo medical exam

Pros: ✓ Best possible rates ✓ Highest coverage amounts ($500K-$5M+) ✓ More policy options and riders ✓ May get standard or even preferred rates

Cons: ✗ Requires full medical exam and records review ✗ Longest approval process (4-8 weeks) ✗ Easy to be declined or rated significantly higher ✗ Most invasive process

Option 4: Graded Benefit Policies

A middle ground for moderate situations.

How It Works:

- Fewer health questions than simplified issue

- Death benefit increases over time

- Typically reaches full benefit after 2-3 years

- Some offer 50% immediately, 100% after waiting period

Best For:

- 2-4 years post-cancer

- Moderate-stage cancers

- One recurrence but now stable

- Between simplified and guaranteed issue in severity

What Is the Best Life Insurance After Cancer?

The best life insurance after cancer depends on your recovery and current health. Traditional term or whole life policies may be available after remission, while simplified or guaranteed issue policies are better for recent or higher-risk cases.

Real Stories: Cancer Survivors Getting Life Insurance

Case Study 1: Susan, Age 66 – Breast Cancer Survivor (5 Years)

Cancer History:

- Stage I breast cancer diagnosed at age 61

- Lumpectomy and radiation (no chemotherapy)

- No recurrence in 5 years

- Annual mammograms all clear

- Takes tamoxifen (hormone therapy)

- Excellent prognosis

- No other health issues

What She Did: Susan applied for simplified issue through Prudential. She answered questions honestly about her breast cancer diagnosis, treatment completion date, and current status. The application took 20 minutes online.

Result: Approved within 48 hours for $200,000 coverage at $385/month. No medical exam required. Coverage started immediately. Five years cancer-free with Stage I breast cancer was enough for approval. This is a typical example of successful life insurance after breast cancer for seniors.

Key Takeaway: Early-stage breast cancer survivors with 5+ years of remission have excellent chances for simplified issue approval with reasonable rates.

Case Study 2: Michael, Age 70 – Prostate Cancer Survivor (3 Years)

Cancer History:

- Prostate cancer (Gleason 7) diagnosed at age 67

- Radical prostatectomy (surgery)

- PSA levels undetectable since surgery

- No additional treatment needed

- 3 years cancer-free

- Some urinary incontinence (common side effect)

- Also has high blood pressure (controlled)

What He Did: Michael initially tried for fully underwritten coverage but was told to wait until 5 years post-treatment. He then applied for simplified issue through Mutual of Omaha, which accepts prostate cancer survivors after 3 years.

Result: Approved for $150,000 simplified issue coverage at $465/month. Had to answer detailed questions about Gleason score and PSA levels but no medical exam required. This demonstrates that life insurance after prostate cancer is very achievable with the right insurer.

Key Takeaway: Prostate cancer survivors with good prognostic factors (low Gleason, undetectable PSA) can get simplified issue after 3 years with cancer-friendly insurers.

Case Study 3: Patricia, Age 69 – Recent Melanoma Survivor (18 Months)

Cancer History:

- Stage II melanoma diagnosed 18 months ago

- Wide excision surgery (removed completely)

- No chemotherapy or radiation needed

- Clear margins on pathology

- No recurrence detected in follow-ups

- Sees dermatologist every 3 months

- Considered moderate risk for recurrence

What She Did: Patricia knew 18 months wasn’t long enough for simplified issue with most companies. She applied for guaranteed issue through Gerber Life to get immediate coverage.

Result: Automatically approved for $20,000 coverage at $145/month. Two-year waiting period applies. She plans to reapply for simplified issue after hitting the 3-year mark for potentially more coverage.

Key Takeaway: Recent cancer survivors (under 2 years) can use guaranteed issue for immediate protection, then upgrade later once enough time passes.

Case Study 4: Robert, Age 74 – Colon Cancer Survivor (8 Years)

Cancer History:

- Stage II colon cancer at age 66

- Colon resection surgery

- Adjuvant chemotherapy (6 months)

- 8 years completely cancer-free

- Regular colonoscopies all clear

- No complications from treatment

- Also has controlled diabetes

What He Did: With 8 years of being cancer-free, Robert applied for fully underwritten coverage through Banner Life to get the best possible rates. He completed a medical exam and provided all cancer treatment records.

Result: Approved for $250,000 in 15-year term coverage at $425/month (rated standard). His long remission period and early-stage diagnosis allowed him to qualify for traditional underwriting despite the cancer history.

Key Takeaway: Long-term cancer survivors (5-10+ years) with early-stage disease can often qualify for traditional underwriting with standard or near-standard rates.

How Much Does Life Insurance Cost After Cancer?

Life insurance after cancer typically costs more than standard policies because insurers consider it a higher-risk condition. However, rates vary widely based on cancer type, stage, and time in remission. However, affordable life insurance after cancer is available when you know where to look and understand pricing factors. Let’s discuss real numbers based on COPD severity and coverage type.

Monthly Premium Estimates for $100,000 Coverage

Simplified Issue (Cancer Survivors):

| Age | Favorable Cancer 5+ Yrs | Moderate Cancer 5+ Yrs | Recent/Aggressive |

|---|---|---|---|

| 65 | $300-$425 | $450-$625 | Usually declined |

| 70 | $425-$575 | $625-$850 | Usually declined |

| 75 | $600-$800 | $850-$1,150 | Usually declined |

Guaranteed Issue (for $10,000-$15,000 coverage):

| Age | Monthly Premium (Any Cancer) |

|---|---|

| 65 | $80-$120 |

| 70 | $115-$165 |

| 75 | $160-$225 |

| 80 | $215-$305 |

Cost Factors for Cancer Survivors

What Reduces Your Premium:

- Longer time since treatment (5+ years much better than 2-3)

- Early-stage cancer (Stage 0 or I)

- Favorable cancer type (skin, breast, prostate)

- No recurrence history

- Clean follow-up tests

- Young age at diagnosis

- Good overall health now

- Non-smoker (critical for lung cancer survivors)

What Increases Your Premium:

- Recent treatment (under 3 years)

- Late-stage cancer (Stage III or IV)

- Aggressive cancer types

- Recurrence history

- Ongoing treatment or monitoring

- Older age

- Multiple health conditions

- Smoker status

Is Life Insurance More Expensive After Cancer?

Yes, life insurance is typically more expensive after cancer because insurers consider it a higher-risk condition. Premiums vary based on cancer type, stage, and how long you’ve been in remission.

👉 Want to see what you qualify for? Get a personalized life insurance quote in under 60 seconds.

Real Example Comparisons:

Scenario 1:

- 68-year-old woman

- Stage 0 breast cancer (DCIS)

- 6 years cancer-free

- No other health issues

- Premium: $325/month for $100K

Scenario 2:

- 68-year-old woman

- Stage II breast cancer

- 3 years cancer-free

- Also has diabetes

- Premium: $575/month for $100K

Difference: $250/month or $3,000/year based on stage, time, and other conditions.

Getting life insurance for cancer survivors becomes straightforward when you follow this proven six-step process.

Step-by-Step: Getting Life Insurance as a Cancer Survivor

Step 1: Gather Your Cancer Treatment Records

Before applying, compile:

Essential Information:

- Cancer type and specific diagnosis

- Date of diagnosis

- Stage at diagnosis (0, I, II, III, or IV)

- Tumor size and characteristics

- Treatment dates (surgery, chemo, radiation)

- Date treatment completed

- All follow-up test results

- Current cancer status (remission, NED, etc.)

- Oncologist’s contact information

Why This Matters: Having detailed information ready shows insurers you’re organized and makes the application process smoother. It also ensures you answer questions accurately.

Step 2: Determine Your Waiting Period

Based on your cancer type and stage, figure out if you’re past the typical waiting period:

If Less Than 2 Years:

- Guaranteed issue is likely your only option

- Exception: Very favorable cancers (basal cell skin cancer) may qualify sooner

If 2-5 Years:

- Simplified issue possible for favorable cancers (Stage 0-I breast, prostate, skin)

- Guaranteed issue still best for aggressive or late-stage cancers

- Worth trying simplified issue and having guaranteed issue as backup

If 5-10 Years:

- Good chances for simplified issue with most cancer types

- May qualify for traditional underwriting with very favorable cancers

- Shop around—different companies have different waiting periods

If 10+ Years:

- Strong chance for simplified issue with any cancer

- May qualify for standard rates with traditional underwriting

- Consider applying for best possible rates

Step 3: Calculate Your Coverage Needs

For Final Expenses ($10,000-$25,000):

- Funeral and burial: $7,000-$12,000

- Final medical bills: $3,000-$8,000

- Small debts: $2,000-$5,000

- Best option: Guaranteed issue

For Family Protection ($50,000-$200,000):

- Final expenses: $10,000-$15,000

- Mortgage or debts: $30,000-$150,000

- Legacy for children: $10,000-$35,000

- Best option: Simplified issue if you qualify

For Comprehensive Coverage ($200,000+):

- All of the above plus significant legacy

- Best option: Simplified issue or traditional if 10+ years cancer-free

Step 4: Choose Cancer-Friendly Insurance Companies

Not all insurers view cancer survivors the same way.

Most Accommodating to Cancer Survivors:

- Mutual of Omaha

- Accepts many cancer types after 2-3 years

- Both simplified and guaranteed issue available

- Reasonable rates for cancer survivors

- Ages 45-85

- Prudential

- Good for breast and prostate cancer survivors

- Accepts survivors at 5+ years with favorable prognosis

- Higher coverage amounts available

- Strong reputation

- AIG

- Simplified issue for cancer survivors 5+ years

- Fast approval process

- Accommodating underwriting

- Good for early-stage cancers

- John Hancock

- Flexible for cancer survivors

- Considers individual cases carefully

- May accept shorter remission periods

- Good customer service

For Guaranteed Issue:

- Gerber Life – Up to $25,000, excellent for recent cancer

- Colonial Penn – Cannot be denied, straightforward

- Mutual of Omaha – Trusted name, reliable

- Globe Life – Quick process, multiple options

Step 5: Be Completely Honest About Your Cancer History

Insurance companies will verify everything through:

- Medical Information Bureau (MIB)

- Prescription records (they see all cancer medications)

- Medical records (they request from your doctors)

- Cancer registry databases

- Social Security Death Index

You Must Disclose:

- Cancer diagnosis date and type

- Exact stage at diagnosis

- All treatments received

- Treatment completion date

- Any recurrences

- Current status and monitoring schedule

- All cancer-related medications

- Follow-up test results

Lying Will Result In:

- Application denial if caught during underwriting

- Policy cancellation if discovered later

- Claim denial when your family needs it most

- Possible fraud charges

Example: John had melanoma 3 years ago but didn’t disclose it, hoping to get better rates. When he died from an unrelated heart attack 2 years after getting coverage, the company investigated (as they do for all deaths within first 2-3 years) and discovered the undisclosed cancer. They voided the policy and returned only premiums paid—his family received nothing.

Step 6: Consider Working With a Specialized Agent

Cancer survivors benefit enormously from working with agents who specialize in high-risk or cancer cases.

They Can Help Because They:

- Know which companies are most cancer-friendly

- Understand specific waiting periods by cancer type

- Know how to position your application favorably

- Can shop 15-20 companies simultaneously

- Have direct underwriter relationships

- Stay updated on changing cancer underwriting guidelines

This Is Especially Valuable If:

- You had late-stage cancer

- You’re within 2-5 years of treatment

- You’ve had a recurrence

- You have multiple health conditions

- You’ve been declined before

Cost: Independent agents cost you nothing—they’re paid by insurance companies, not by you.

Cancer-Specific Insurance Considerations

Breast Cancer Survivors

Good News: Breast cancer has excellent life insurance prospects, especially with early detection. Life insurance after breast cancer is one of the most commonly approved cancer survivor scenarios.

Typical Waiting Periods:

- Stage 0 (DCIS): 2 years

- Stage I: 3-5 years

- Stage II: 5 years

- Stage III: 7-10 years

What Helps Approval:

- ER/PR positive (hormone-responsive)

- HER2 negative

- Clean lymph nodes

- Lumpectomy vs. mastectomy doesn’t matter much

- Completing hormone therapy successfully

Example Rates: 65-year-old woman, Stage I breast cancer, 5 years remission: $325-$425/month for $100K simplified issue

Prostate Cancer Survivors

Good News: Prostate cancer is often slow-growing, and insurers know this. Life insurance after prostate cancer has favorable approval rates compared to other cancer types.

Typical Waiting Periods:

- Gleason 6 (low-grade): 2-3 years

- Gleason 7: 3-5 years

- Gleason 8+: 7-10 years

What Helps Approval:

- Low Gleason score (6-7)

- Undetectable PSA post-treatment

- Successful surgery with clear margins

- Low PSA velocity before diagnosis

- No metastases

Example Rates: 70-year-old man, Gleason 7 prostate cancer, 4 years remission: $450-$575/month for $100K simplified issue

Skin Cancer Survivors (Non-Melanoma)

Good News: Basal cell and squamous cell skin cancers are viewed very favorably.

Typical Waiting Periods:

- Basal cell: 1-2 years

- Squamous cell: 1-2 years

- May qualify for standard rates quickly

What Helps Approval:

- Complete surgical removal

- No recurrence

- No metastasis

- Single occurrence vs. multiple

Example Rates: 68-year-old, basal cell skin cancer removed 2 years ago: $250-$350/month for $100K simplified issue

Melanoma Survivors

More Challenging: Melanoma is taken more seriously due to metastasis risk.

Typical Waiting Periods:

- Stage 0 (in situ): 2-3 years

- Stage I: 5 years

- Stage II: 7-10 years

- Stage III: 10+ years

What Helps Approval:

- Thin tumor (< 1mm)

- No ulceration

- Low mitotic rate

- Clean sentinel nodes

- Complete excision with clear margins

Colorectal Cancer Survivors

Moderately Challenging: Depends heavily on stage and lymph node involvement.

Typical Waiting Periods:

- Stage I: 5 years

- Stage II: 5-7 years

- Stage III: 10+ years

What Helps Approval:

- Early stage (I-II)

- No lymph node involvement

- MSI-high tumors (better prognosis)

- Clean colonoscopies post-treatment

Lung Cancer Survivors

Most Challenging: Lung cancer has lower survival rates, so insurers are cautious.

Typical Waiting Periods:

- Any stage: Usually 10+ years minimum

- May need guaranteed issue for first 10 years

What Helps Approval:

- Stage I only

- Complete surgical removal

- Never smoker or quit decades ago

- Long remission period (10+ years)

Frequently Asked Questions

Can cancer survivors get life insurance?

Yes, absolutely! Cancer survivors can get life insurance after cancer for seniors, though options and timing depend on cancer type, stage, and how long you’ve been cancer-free. If you’ve been in remission for 5+ years with early-stage cancer, you’ll likely qualify for simplified issue policies offering $25,000-$500,000 without a medical exam. If your cancer was recent (under 2 years) or more aggressive, guaranteed issue policies provide $5,000-$25,000 regardless of cancer status. The key is understanding waiting periods and choosing the right policy type for your situation. Most cancer survivors eventually qualify for affordable coverage.

How long after cancer treatment can I get life insurance?

The waiting period varies dramatically by cancer type. Basal cell skin cancer survivors might qualify for simplified issue after just 1-2 years, while Stage I breast or prostate cancer typically requires 3-5 years. More aggressive cancers like melanoma, lung, or pancreatic cancer may need 7-10+ years before simplified issue approval. However, you can get guaranteed issue coverage immediately after any cancer diagnosis or treatment—there’s no waiting period required. These policies provide $5,000-$25,000 with a grading period but cannot deny you regardless of cancer type or how recent. Many cancer survivors use guaranteed issue for immediate protection, then upgrade to simplified issue once enough time passes.

Does the stage of cancer matter for life insurance?

Yes, cancer stage is one of the most critical factors insurers consider. Stage 0 (in situ) or Stage I cancers have the shortest waiting periods (2-5 years typically) and best approval odds because survival rates are excellent. Stage II cancers require moderate waiting periods (5-7 years usually) and face slightly higher premiums. Stage III cancers need longer waiting periods (7-10+ years) and may be declined by some simplified issue insurers. Stage IV cancers typically require guaranteed issue coverage for many years, as recurrence risk is highest. The stage at diagnosis matters far more than the type of cancer in many cases—early detection dramatically improves your life insurance prospects.

Can I get life insurance if my cancer came back?

Yes, but recurrence significantly limits your options and extends waiting periods. If you’ve had a recurrence that’s now in remission for 5-10 years with no further issues, some simplified issue companies may consider you, though you’ll face higher premiums and stricter underwriting. If your recurrence was recent (within 5 years), guaranteed issue is typically your only option, providing $5,000-$25,000 with a waiting period. Multiple recurrences make simplified issue approval extremely difficult, and most survivors with recurrent cancer rely on guaranteed issue. The good news is you absolutely can get coverage—it just may be guaranteed issue with lower amounts rather than simplified issue with higher coverage.

Is life insurance more expensive for cancer survivors?

Yes, life insurance costs more for cancer survivors than for people who’ve never had cancer, but how much more depends on many factors. A Stage I breast cancer survivor who’s been cancer-free for 5 years might pay 50-100% more than someone without cancer history. A Stage III cancer survivor might pay 100-200% more. Recent cancer survivors (under 2 years) typically need guaranteed issue, which costs significantly more per dollar of coverage. However, long-term survivors (10+ years) with favorable cancers can sometimes qualify for rates close to standard. Your cancer type, stage, time since treatment, and current health all affect pricing. It’s more expensive, but it’s affordable and available.

What’s the best life insurance for breast cancer survivors?

For breast cancer survivors, the best option depends on how long you’ve been cancer-free. If it’s been 5+ years since completing treatment for Stage I-II breast cancer, simplified issue policies from companies like Prudential, Mutual of Omaha, or John Hancock offer excellent value—no medical exam, coverage up to $500,000, and reasonable rates ($300-$500/month for $100K at age 65-70). If it’s been 2-5 years, some insurers may still consider you but with higher premiums. If it’s been less than 2 years or you had Stage III breast cancer, guaranteed issue from Gerber Life or Mutual of Omaha ensures coverage ($5,000-$25,000) while you wait for enough time to pass for simplified issue.

Do I need to disclose cancer if it was more than 10 years ago?

Yes, you must always disclose any cancer history, even if it was decades ago. Life insurance applications explicitly ask about cancer diagnoses regardless of when they occurred. Lying or omitting cancer history is insurance fraud and will result in claim denial when your family needs the money most. The good news is that cancer 10+ years ago with no recurrence is viewed very favorably by insurers—you’ll likely qualify for simplified or even traditional coverage with reasonable rates. Your honest disclosure of old, successfully treated cancer actually helps your application because it shows a long cancer-free period. Never hide cancer history, no matter how old.

Can I get life insurance while undergoing cancer treatment?

Getting simplified issue life insurance during active cancer treatment is virtually impossible—companies want to see completed treatment and some cancer-free time. However, you can get guaranteed issue life insurance at any point, even during active treatment. Guaranteed issue policies ask no health questions and cannot deny you whether you’re mid-chemotherapy, recovering from surgery, or in any stage of treatment. Coverage is limited ($5,000-$25,000) with a 2-3 year waiting period, but it ensures your funeral expenses are covered and gives your family some protection. Many cancer patients get guaranteed issue during treatment, then upgrade to simplified issue after 2-5 years of remission.

Does the type of cancer treatment affect life insurance approval?

Yes, treatment type influences approval odds and timing. Surgery-only treatment is viewed most favorably, especially if margins were clear and cancer was completely removed. Surgery plus radiation is also acceptable. Surgery plus chemotherapy shows more aggressive cancer but isn’t necessarily disqualifying if you’ve been cancer-free for enough time. Ongoing hormone therapy (like tamoxifen for breast cancer) is generally acceptable. Immunotherapy and targeted therapies are evaluated case-by-case. The key factor isn’t so much which treatment you had, but rather: (1) was treatment successful? (2) has cancer stayed away? (3) how long has it been? Complete treatment with no recurrence for 3-5+ years is what matters most.

Can prostate cancer survivors get life insurance?

Yes, prostate cancer survivors have good life insurance prospects because prostate cancer is often slow-growing with excellent survival rates. Low-grade prostate cancer (Gleason 6-7) survivors can often qualify for simplified issue after just 2-3 years if PSA levels remain undetectable. Higher-grade prostate cancer (Gleason 8+) typically requires 5-7 years before simplified issue approval. Companies like Mutual of Omaha, Prudential, and AIG are particularly accommodating to prostate cancer survivors. A 70-year-old man with Gleason 7 prostate cancer, 3 years post-surgery with undetectable PSA, might pay $450-$575/month for $100K simplified issue coverage—higher than someone without cancer, but very affordable.

Will life insurance pay out if I die from cancer recurrence?

Yes, if you were honest on your application about your cancer history, life insurance will pay the full death benefit if you die from cancer recurrence. Your policy cannot be cancelled or claims denied simply because your cancer came back—you had cancer when you applied (and disclosed it), so recurrence is not considered non-disclosure. The only way a claim would be denied is if you lied about or failed to disclose your cancer history when applying. This is why honesty is absolutely critical. If you disclosed everything and were approved, your beneficiaries will receive the full benefit regardless of whether you die from cancer recurrence, a different cause, or any other reason (after any waiting period ends).

Should I wait longer to apply to get better rates?

This depends on your specific situation. If you’re just 6 months past treatment, waiting another 18 months to hit the 2-year mark could open up simplified issue options with much better rates and higher coverage. However, don’t wait excessively—every year you age increases premiums by 8-12%, which can offset any savings from waiting longer. A good strategy: get guaranteed issue coverage now for immediate protection ($10,000-$20,000), then reapply for simplified issue once you hit the optimal waiting period for your cancer type. This gives you coverage today while positioning you for an upgrade later. If you’re already past 5 years cancer-free, don’t wait any longer—apply now before aging makes coverage more expensive.

Taking Action: Your Next Steps

Can cancer survivors get life insurance? The answer is definitively yes. Getting life insurance after cancer for seniors is absolutely achievable with the right approach. Here’s your action plan:

This Week:

- Gather all cancer treatment records (diagnosis, stage, treatment dates, pathology reports)

- Note your exact cancer-free date (last day of treatment or surgery)

- Collect recent follow-up test results (clean scans, normal blood work)

- List all current medications (including cancer-related ones)

- Calculate how much coverage you actually need

This Month:

- Determine which policy type fits your timeline (simplified vs. guaranteed)

- Identify cancer-friendly insurance companies for your specific cancer type

- Get quotes from 3-5 companies (rates vary significantly)

- Consider working with an agent who specializes in cancer survivor cases

- Check for any group life insurance options (employer, associations)

Before Applying:

- Have your oncologist’s contact information ready

- Be prepared to disclose everything about your cancer honestly

- Understand waiting periods if choosing guaranteed issue

- Choose your beneficiaries

- Confirm premiums fit your budget

Remember:

- You’ve beaten cancer—getting life insurance is much easier

- Options exist regardless of cancer type or how recent

- Time is your friend—the longer you’re cancer-free, the better

- Guaranteed issue ensures immediate coverage while you wait

- Your family deserves protection—don’t put this off

Conclusion: You’re Not Uninsurable

Being a cancer survivor doesn’t make you uninsurable—it just means you need to be strategic about when and how you apply for life insurance after cancer for seniors. Whether you beat breast cancer last year, you’re a prostate cancer survivor celebrating 5 years of remission, or you’re dealing with a more challenging cancer history, affordable life insurance after cancer options exist.

Key Takeaways:

✓ Time matters most: The longer you’re cancer-free, the better your options ✓ Cancer type and stage are critical: Early-stage, favorable cancers have shortest waiting periods ✓ Guaranteed issue is always available: No waiting period to apply, immediate protection ✓ Simplified issue opens up: 2-5+ years cancer-free (depending on type) ✓ Traditional coverage possible: 10+ years cancer-free with favorable cancers ✓ Honesty is essential: Never hide your cancer history ✓ Rates vary dramatically: Shop multiple companies for best pricing

You’ve already won the hardest battle. Getting life insurance is just paperwork in comparison. Don’t let your cancer history prevent you from protecting your family financially. Whether you need $10,000 for final expenses or $250,000 for comprehensive coverage, the right policy exists for your situation.

Compare quotes today, choose a cancer-friendly insurer, and take that crucial first step toward peace of mind. Your family—and your legacy—deserve nothing less.

Disclaimer: This article provides general information about life insurance for senior cancer survivors and should not be considered medical, financial, or legal advice. Life insurance availability, rates, and underwriting standards vary significantly by company, state, individual health circumstances, cancer type, stage, treatment history, time since diagnosis, and many other factors. Premium estimates are approximate and for illustrative purposes only. Cancer is a serious disease requiring ongoing medical care—always consult with your oncologist and healthcare team about your treatment and prognosis. This article does not constitute medical advice about cancer treatment or survival rates. Individual insurance results will vary based on age, gender, cancer type, stage, treatment, time since completion, recurrence history, overall health, and other factors assessed during underwriting. Always work with licensed insurance professionals and review policy documents carefully before purchasing coverage.