Life Insurance for Seniors With High Blood Pressure: 2026 Guide

Posted in Life Insurance w/ Pre-existing Conditions on November 23, 2025 last updated on June 1, 2026

Posted in Life Insurance w/ Pre-existing Conditions on November 23, 2025 last updated on June 1, 2026

Can you get life insurance with high blood pressure?

The short answer is yes, you can qualify for affordable life insurance with controlled high blood pressure.

Here’s some good news: having high blood pressure doesn’t mean you can’t get life insurance. In fact, it’s one of the most common health conditions insurance companies see, and most seniors with well-controlled hypertension can qualify for affordable coverage.

If you’ve been putting off applying for life insurance because of your blood pressure readings, or you’ve been worried that your hypertension medication will disqualify you, I’m here to tell you that you have more options than you might think. Millions of seniors with high blood pressure successfully secure life insurance every year—and you can too.

In this guide, I’ll walk you through everything you need to know about getting life insurance as a senior with high blood pressure, from understanding how insurers view hypertension to finding the best companies and rates for your situation.

Understanding Life Insurance for Seniors with High Blood Pressure

High blood pressure (hypertension) is incredibly common among seniors. According to the CDC, nearly half of all American adults have high blood pressure, and that percentage increases significantly after age 60. Insurance companies know this, which is why they’ve developed clear guidelines for evaluating applicants with hypertension.

What Insurance Companies Want to Know

When you apply for life insurance as a senior, underwriters focus on several key factors:

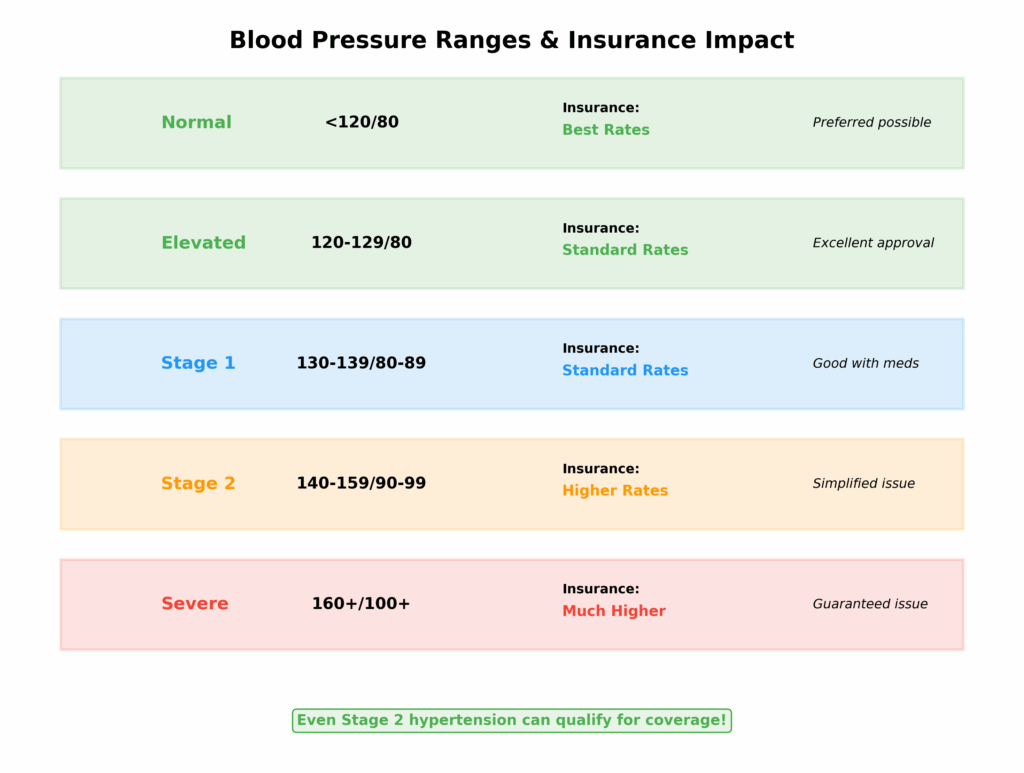

Your Blood Pressure Numbers: The most important factor is your actual blood pressure reading. Here’s how insurers typically classify it:

- Normal: Below 120/80 (best rates)

- Elevated: 120-129/80 (standard rates usually)

- Stage 1 Hypertension: 130-139/80-89 (standard to slightly higher rates)

- Stage 2 Hypertension: 140+/90+ (higher rates, may need simplified issue)

- Hypertensive Crisis: 180+/120+ (guaranteed issue likely needed)

How Well It’s Controlled:

- Are you taking medication consistently?

- Have your readings been stable over time?

- Do you monitor your blood pressure regularly?

- Have you made lifestyle changes?

How Long You’ve Had It:

- Recently diagnosed (within 6 months) makes insurers more cautious

- 1-2 years with good control is better

- 5+ years with excellent control is ideal

Related Health Conditions:

- Do you also have diabetes? (Learn about life insurance with diabetes)

- Any heart disease? (Read our guide on life insurance with heart disease)

- Kidney problems?

- High cholesterol?

- Obesity?

Complications:

- Any history of stroke?

- Heart attack or chest pain?

- Vision problems?

- Kidney disease?

The good news? If your blood pressure is under control with medication and you don’t have serious complications, you’ll likely qualify for standard or near-standard rates with most insurers.

Options for Life Insurance for Seniors with High Blood Pressure

Option 1: Traditional Fully Underwritten Life Insurance

If your blood pressure is well-controlled, you might qualify for traditional life insurance with competitive rates.

Best For:

- Blood pressure readings consistently below 140/90

- Taking 1-2 medications that work well

- No complications or related conditions

- Good overall health otherwise

The Process:

- Complete detailed application

- Medical exam including blood pressure check

- Blood work and urine sample

- Medical records review

- Underwriting decision (2-6 weeks)

Pros: ✓ Best possible rates if approved ✓ Highest coverage amounts available ($500K-$5M+) ✓ Many policy options and riders ✓ Can get preferred rates with excellent control

Cons: ✗ Requires full medical exam ✗ Longest approval time ✗ Can be declined if readings are high ✗ Most invasive process

What to Expect: A 65-year-old non-smoker with well-controlled Stage 1 hypertension might pay $180-$250/month for $250,000 in 20-year term coverage. With excellent control (below 130/80), you might even qualify for preferred rates.

Option 2: Simplified Issue Life Insurance

Also known as final expense insurance. This is the sweet spot for most seniors with high blood pressure—no medical exam required, just health questions. If you want to avoid medical exams entirely, our guide to life insurance for seniors with no medical exam covers simplified and guaranteed issue options in detail

Best For:

- Blood pressure below 150/95 with medication

- Stable readings for at least 6 months

- No recent hospitalizations

- Want to avoid medical exams

The Process:

- Answer 10-15 health questions online or by phone

- Questions about blood pressure, medications, complications

- Decision within 24-48 hours

- Coverage begins immediately upon approval

Pros: ✓ No medical exam, blood tests, or urine samples ✓ Much faster approval (1-2 days typically) ✓ Coverage amounts up to $500,000 ✓ Immediate full coverage (no waiting period) ✓ Less invasive than traditional underwriting

Cons: ✗ Slightly higher premiums than fully underwritten ✗ Must answer health questions honestly ✗ Lower coverage limits than traditional ✗ May be declined if complications exist

What to Expect: That same 65-year-old might pay $220-$300/month for $250,000 in simplified issue coverage—a bit more than traditional, but with the convenience of no exam and fast approval.

Top Companies for Simplified Issue:

- Mutual of Omaha (very accommodating to controlled hypertension)

- AIG (accepts blood pressure up to 150/95)

- SBLI (quick online approval)

- Prudential (good rates for well-controlled cases)

Option 3: Guaranteed Issue Life Insurance

If your blood pressure is poorly controlled or very high, guaranteed issue policies ensure you can still get coverage.

Best For:

- Blood pressure consistently above 160/100

- Multiple blood pressure medications

- Hypertension-related complications

- Anyone who’s been declined elsewhere

The Process:

- Request a quote (2 minutes)

- Provide basic information only

- No health questions asked at all

- Automatic approval

- Coverage begins with 2-3 year waiting period

Pros: ✓ Absolutely cannot be denied ✓ No health questions whatsoever ✓ No medical records needed ✓ Perfect for final expenses ✓ Accidental death covered immediately

Cons: ✗ Lower coverage amounts ($5,000-$25,000) ✗ Higher premiums per dollar of coverage ✗ 2-3 year waiting period for natural death ✗ Not suitable for large coverage needs

The Waiting Period Explained:

- Years 1-2: If you die from illness, beneficiaries get premiums paid back plus 10% interest

- Years 1-2: If you die from accident, full benefit paid immediately

- Year 3+: Full benefit paid for any cause of death

Top Companies for Guaranteed Issue:

- Mutual of Omaha

- Gerber Life

- Colonial Penn

- Globe Life

Real Stories: Life Insurance for Seniors with High Blood Pressure Getting Coverage

Let me share some real examples to show you what’s actually possible.

Case Study 1: Margaret, Age 68 – Well-Controlled Hypertension

Health Profile:

- Blood pressure: 132/84 (controlled with medication)

- Takes one blood pressure medication (lisinopril)

- Diagnosed 8 years ago

- Regular doctor visits every 6 months

- No complications

- Non-smoker

- Slightly overweight but active

What She Did: Margaret applied for simplified issue life insurance through AIG. She answered health questions honestly about her blood pressure and medication. The entire process took 15 minutes online.

Result: Approved within 24 hours for $150,000 coverage at $215/month. No medical exam required. Coverage started immediately.

Key Takeaway: Well-controlled Stage 1 hypertension with medication compliance easily qualifies for simplified issue with reasonable rates.

Case Study 2: Robert, Age 72 – Stage 2 Hypertension

Health Profile:

- Blood pressure: 148/92 (partially controlled)

- Takes two blood pressure medications

- Also has high cholesterol

- Diagnosed 12 years ago

- Occasional missed medications

- Former smoker (quit 5 years ago)

- Overweight

What He Did: Robert first tried simplified issue but was concerned about his readings. He worked with an independent agent who shopped multiple companies. They found one willing to offer coverage despite his higher readings.

Result: Approved by Mutual of Omaha for $100,000 simplified issue coverage at $285/month. Had to answer additional questions but no medical exam was required.

Key Takeaway: Even with Stage 2 hypertension, coverage is possible—you just need to find the right company and be prepared for higher premiums.

Case Study 3: Patricia, Age 75 – Excellent Control

Health Profile:

- Blood pressure: 118/76 (excellent control)

- Takes one low-dose blood pressure medication

- Diagnosed 15 years ago but extremely compliant

- Monitors blood pressure daily

- Healthy weight, exercises regularly

- Non-smoker

- No other health issues

What She Did: Patricia’s agent recommended she try for fully underwritten coverage given her excellent control. She completed a medical exam including blood pressure check.

Result: Approved by Banner Life for $300,000 in 15-year term at $198/month—she received standard rates, the same as someone without hypertension!

Key Takeaway: Excellent blood pressure control can earn you standard rates with traditional underwriting, making it the most affordable option.

Case Study 4: James, Age 78 – Uncontrolled Hypertension

Health Profile:

- Blood pressure: 165/98 (poorly controlled)

- Takes three blood pressure medications

- Also has diabetes and kidney disease

- Multiple hospitalizations in past year

- Non-compliant with medications

- Smoker

What He Did: James knew his health issues would disqualify him from simplified issue. He applied for guaranteed issue coverage through Gerber Life.

Result: Automatically approved for $15,000 coverage at $138/month. Two-year waiting period applies, but he has peace of mind knowing his funeral expenses will be covered.

Key Takeaway: Even with very poorly controlled hypertension and multiple complications, guaranteed issue ensures coverage is available.

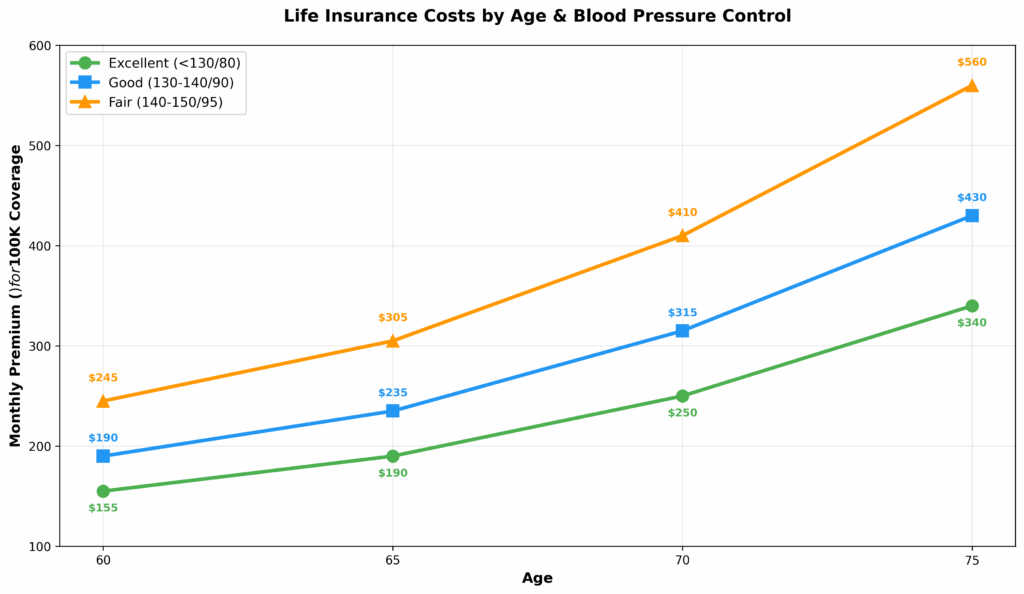

How Much Does Life Insurance Cost With High Blood Pressure?

Let’s talk real numbers. Your life insurance rate will depend on your blood pressure control, age, and overall health.

Monthly Premium Estimates for $100,000 Coverage

Simplified Issue Policies:

| Age | Excellent Control (<130/80) | Good Control (130-140/90) | Fair Control (140-150/95) |

|---|---|---|---|

| 60 | $135-$175 | $165-$215 | $215-$275 |

| 65 | $165-$215 | $205-$265 | $265-$345 |

| 70 | $215-$285 | $275-$355 | $355-$465 |

| 75 | $295-$385 | $375-$485 | $485-$635 |

Guaranteed Issue (for $10,000-$15,000 coverage):

| Age | Monthly Premium Range |

|---|---|

| 60 | $50-$75 |

| 65 | $65-$95 |

| 70 | $85-$125 |

| 75 | $110-$160 |

| 80 | $145-$210 |

What Affects Your Premium?

Premium Reducers (Save You Money):

- Blood pressure below 130/80

- Taking only 1 medication

- Consistent readings for 2+ years

- Regular doctor visits

- Non-smoker

- Healthy weight

- No complications

- Female (women typically pay 20-30% less)

- Younger age

Premium Increasers (Cost You More):

- Blood pressure above 150/95

- Multiple medications (3+)

- Inconsistent readings

- Poor medication compliance

- Smoker (adds 50-100% to premiums)

- Obesity

- Related conditions (diabetes, heart disease)

- Recent hospitalization

- Male gender

Best Life Insurance Companies for Controlled High Blood Pressure

| Company | Good For |

|---|---|

| Mutual of Omaha | Controlled hypertension |

| Prudential | Cardiac history |

| Protective | Traditional underwriting |

| Banner | Competitive term rates |

| AIG | Simplified issue |

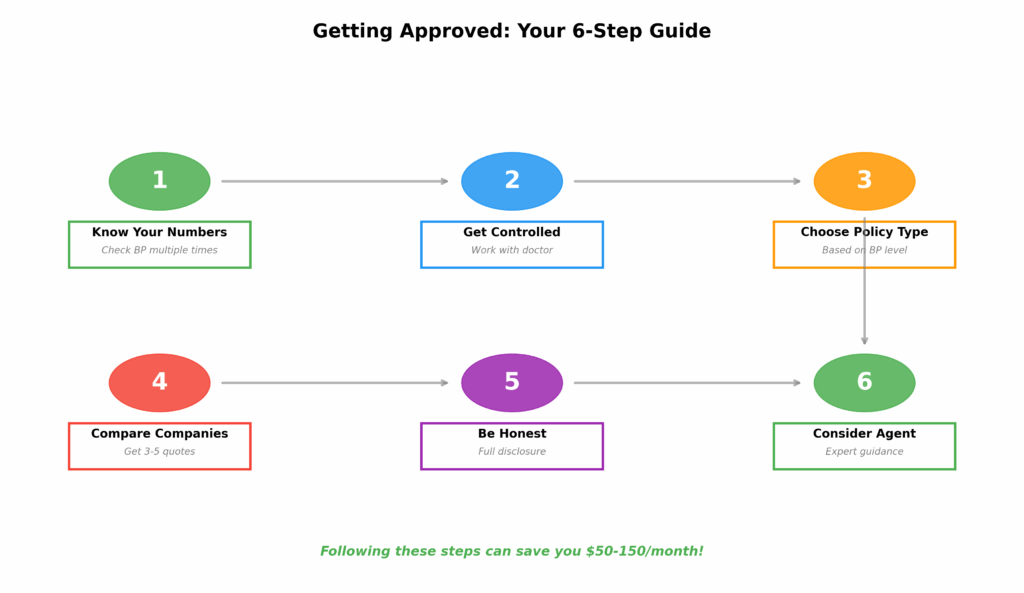

Step-by-Step: Getting Approved With High Blood Pressure

Step 1: Know Your Numbers

Before applying, you need to know:

- Your current blood pressure readings (ideally several recent readings)

- Your medications (names and dosages)

- When you were diagnosed

- Your doctor’s contact information

- Any complications you’ve had

Action Item: Check your blood pressure multiple times over the next week and record the results. If you don’t have a home monitor, get one—they’re inexpensive and show insurers you’re proactive.

Step 2: Get Your Blood Pressure Under Control

If possible, wait to apply until your blood pressure is well-controlled. Here’s why:

Example:

- Applying with BP of 158/94: Might pay $385/month for $100K

- Waiting 3 months, getting BP to 138/86: Might pay $275/month for $100K

- Savings: $110/month or $1,320/year!

Work with your doctor to:

- Adjust medications if current ones aren’t working

- Implement lifestyle changes (diet, exercise, stress reduction)

- Document consistent good readings for at least 2-3 months

However: Don’t wait years to apply. Every year you age, premiums increase 8-12%. If you’re already reasonably controlled, apply now.

Step 3: Choose Your Policy Type

Choose Traditional Fully Underwritten If:

- Blood pressure consistently below 140/90

- You want the absolute best rates

- You’re comfortable with medical exams

- You need very large coverage amounts ($500K+)

- You’re willing to wait 4-6 weeks for approval

Choose Simplified Issue If:

- Blood pressure below 150/95 with medication

- You want convenience and speed

- You prefer no medical exam

- You need coverage quickly

- Coverage needs are under $500K

Choose Guaranteed Issue If:

- Blood pressure is above 160/100

- You have complications (stroke, kidney disease, etc.)

- You’ve been declined elsewhere

- You only need final expense coverage

- You want absolute certainty of approval

Step 4: Compare Multiple Companies

Different insurers have different underwriting standards for high blood pressure. Some are much more lenient than others.

Most Accommodating to Hypertension:

- Mutual of Omaha – Accepts Stage 2 hypertension in simplified issue

- AIG – Reasonable rates for controlled blood pressure

- SBLI – Good for slightly elevated readings

- Protective Life – Flexible underwriting standards

- Transamerica – Accommodating to seniors with medication-controlled BP

For Guaranteed Issue:

- Gerber Life – Ages 50-80, up to $25,000

- Mutual of Omaha – Ages 45-85, excellent reputation

- Colonial Penn – Easy application process

- SBLI – Good customer service

Pro Tip: Get quotes from at least 3-5 companies. Premiums can vary by 30-40% between insurers for the same coverage!

Step 5: Be Completely Honest

This cannot be overstated: tell the complete truth about your blood pressure.

Insurance companies will verify through:

- Prescription drug databases (they’ll see your BP meds)

- Medical Information Bureau (MIB)

- Your medical records (with your permission)

- The medical exam (if required)

What to Disclose:

- Your highest blood pressure readings

- All medications (including dosage)

- Any hospitalizations related to hypertension

- Complications like stroke, kidney issues, or heart problems

- Other health conditions

Don’t worry: Being honest about well-controlled hypertension won’t disqualify you. Lying about it will cause claim denial later when your family needs the money most.

Step 6: Consider Working With an Independent Agent

An independent insurance agent can:

- Shop multiple companies simultaneously

- Know which insurers are most lenient for high blood pressure

- Help position your application for best results

- Answer questions about underwriting

- Save you time and potentially money

- Cost you nothing (paid by insurance companies)

This is especially valuable if:

- Your blood pressure is difficult to control

- You have multiple health conditions (high blood pressure plus diabetes, for example)

- You’ve been declined before

- You’re not sure which policy type to choose

High Blood Pressure Medications and Life Insurance

Many seniors worry that their blood pressure medications will disqualify them. Good news: they won’t! In fact, taking prescribed medication shows insurers you’re managing your condition responsibly.

Common Blood Pressure Medications (All Generally Acceptable):

ACE Inhibitors:

- Lisinopril (Prinivil, Zestril)

- Enalapril (Vasotec)

- Ramipril (Altace)

- These are very common and well-accepted by insurers

ARBs (Angiotensin II Receptor Blockers):

- Losartan (Cozaar)

- Valsartan (Diovan)

- Telmisartan (Micardis)

- Also very common and accepted

Beta Blockers:

- Metoprolol (Lopressor, Toprol)

- Atenolol (Tenormin)

- Carvedilol (Coreg)

- Accepted, though may indicate heart issues in some cases

Calcium Channel Blockers:

- Amlodipine (Norvasc)

- Diltiazem (Cardizem)

- Nifedipine (Procardia)

- Well-accepted

Diuretics (Water Pills):

- Hydrochlorothiazide (HCTZ)

- Furosemide (Lasix)

- Chlorthalidone

- Very common first-line treatment, well-accepted

Combination Medications: Many people take combinations (like lisinopril + HCTZ). This is fine and very common.

What Insurers Actually Care About:

Not Concerning:

- Taking 1-2 blood pressure medications

- Standard doses

- Medications working well

- No side effects

Slightly Concerning:

- Taking 3+ different blood pressure medications (suggests harder to control)

- Very high doses

- Frequent medication changes (suggests trial and error)

- Side effects causing non-compliance

Red Flags:

- Not taking prescribed medications

- Frequently missing doses

- Stopping medications without doctor approval

- Blood pressure still uncontrolled despite multiple medications

Bottom Line: Taking 1-2 blood pressure medications that effectively control your hypertension is completely normal and won’t negatively impact your life insurance application. It actually helps your case by showing management!

Understanding Blood Pressure Readings and Insurance Classifications

Let me break down exactly what insurers look for in blood pressure readings:

What Your Numbers Mean:

Systolic (Top Number):

- Measures pressure when your heart beats

- More important to insurers as you age

- Higher cardiovascular risk indicator

Diastolic (Bottom Number):

- Measures pressure between beats

- Still important but less critical for seniors

- Very high numbers (100+) are concerning

How Insurers Classify You:

Preferred Plus (Best Rates):

- Blood pressure below 130/80 without medication

- Rare for seniors but possible

- Requires excellent overall health

- Can save 30-40% on premiums

Preferred (Excellent Rates):

- Blood pressure below 130/80 with medication

- Or below 135/85 without medication

- No other health issues

- Can save 20-30% on premiums

Standard (Normal Rates):

- Blood pressure 130-140/80-90 with medication

- This is where most seniors land

- Fair pricing, widely available

- Still very affordable

Standard Smoker:

- Same blood pressure ranges but you smoke

- Premiums typically double

- Quitting for 12 months gets you non-smoker rates

Table Ratings (Higher Premiums):

- Blood pressure 140-160/90-100

- Or poorly controlled despite medication

- Premiums increase 25-100% above standard

- Still better than guaranteed issue

Declined/Guaranteed Issue Only:

- Blood pressure consistently above 160/100

- Or complications like stroke, kidney failure

- Guaranteed issue becomes your option

- Higher cost but ensures coverage

Life Insurance for Seniors with High Blood Pressure and Other Health Conditions

Many seniors don’t have high blood pressure alone. In fact, hypertension often occurs alongside other medical conditions that can affect life insurance approval and pricing.

Common combinations include:

- High blood pressure and diabetes

- High blood pressure and heart disease

- High blood pressure and high cholesterol

- High blood pressure and sleep apnea

- High blood pressure and a history of stroke

The good news is that many insurance companies evaluate your overall health profile rather than focusing on a single diagnosis. Seniors with stable, well-managed conditions often qualify for coverage even when multiple health issues are present.

If you have more than one chronic condition, simplified issue, no medical exam, final expense, and guaranteed issue policies may all be worth exploring depending on your age and medical history.

Frequently Asked Questions

Can you get life insurance if you have high blood pressure?

Yes, absolutely! High blood pressure is one of the most common conditions insurance companies see, and millions of seniors with hypertension have life insurance. The key is how well your blood pressure is controlled. If your readings are below 150/95 with medication, you’ll likely qualify for simplified issue policies without even needing a medical exam. If your blood pressure is higher or poorly controlled, guaranteed issue policies are available that accept everyone regardless of health conditions. The vast majority of seniors with high blood pressure can get affordable coverage.

Does high blood pressure affect life insurance rates?

es, high blood pressure affects your rates, but usually not dramatically if it’s well-controlled. Seniors with excellent blood pressure control (below 130/80 with medication) often pay standard rates or just slightly higher. Those with Stage 1 hypertension (130-140/80-90) might pay 10-30% more than someone without high blood pressure. Stage 2 hypertension (above 140/90) typically results in 30-60% higher premiums. However, these increases are still far more affordable than guaranteed issue coverage. The better your blood pressure control, the better your rates—it’s that simple.

What blood pressure is too high for life insurance?

There’s no specific blood pressure reading that automatically disqualifies you from all life insurance. However, readings consistently above 160/100 will likely limit you to guaranteed issue policies, which accept everyone regardless of blood pressure. For simplified issue coverage (no medical exam), most companies want to see readings below 150/95. For traditional fully underwritten policies with the best rates, they typically prefer blood pressure below 140/90. Remember, even if your blood pressure is very high, guaranteed issue ensures you can still get coverage—you’re never truly “too high” to get some form of life insurance.

Should I wait to apply until my blood pressure is better controlled?

This depends on your current situation. If your blood pressure is just slightly elevated (like 148/90) and your doctor is adjusting your medication, waiting 2-3 months to show better control could save you significant money on premiums. However, don’t wait years hoping for perfect readings—every year you age increases premiums by 8-12%, which can outweigh any savings from better blood pressure control. If you’re over 70, apply now rather than waiting. If you’re in your 60s with recently diagnosed hypertension, getting control for a few months first makes sense. When in doubt, get a quote now to see current costs, then decide if waiting might help.

Can you get life insurance if you don’t take blood pressure medication?

Yes, but your options depend on your actual blood pressure readings. If you have normal blood pressure (below 120/80) without medication, you’ll get the best rates available. If you have elevated blood pressure (120-140/80-90) but choose not to take medication, insurers may view this as a higher risk and charge more or require you to start medication. If you have Stage 2 hypertension (140+/90+) and refuse medication, most simplified issue companies will decline you, leaving guaranteed issue as your primary option. Insurers generally prefer applicants who take prescribed medication because it shows you’re actively managing your health.

Does smoking affect life insurance if you have high blood pressure?

Smoking dramatically affects your life insurance rates, especially when combined with high blood pressure. Smokers with hypertension typically pay 100-150% more than non-smokers with the same blood pressure readings. For example, a 65-year-old non-smoker with controlled blood pressure might pay $200/month for $100K coverage, while a smoker would pay $400-500/month for the same coverage. The good news? If you quit smoking and remain smoke-free for 12 months (24 months with some insurers), you can qualify for non-smoker rates. Quitting smoking is the single best thing you can do to lower your life insurance premiums when you have high blood pressure.

Will my life insurance company check my blood pressure during the medical exam?

Yes, if you apply for traditional fully underwritten life insurance, the medical exam always includes a blood pressure check. The examiner will typically take multiple readings and record the average. If your blood pressure is elevated during the exam due to nervousness (“white coat syndrome”), let the examiner know and they’ll often wait a few minutes and recheck. You can also provide documentation of home blood pressure readings to show your typical numbers. For simplified issue policies, there’s no medical exam at all, so your blood pressure is evaluated based only on your answers to health questions and your medical records.

Can you get life insurance after having a stroke caused by high blood pressure?

Yes, you can get life insurance after a stroke, though your options depend on when it occurred and your recovery. If your stroke was within the past 6-12 months, guaranteed issue policies are likely your only option. These policies accept all applicants and provide $5,000-$25,000 in coverage with a 2-3 year waiting period. If your stroke was 2-5 years ago with good recovery and no complications, some simplified issue companies may consider you, especially if your blood pressure is now well-controlled. If it’s been 5+ years with excellent recovery, you might even qualify for traditional underwriting with higher premiums. Having a stroke makes coverage harder to get, but not impossible.

How long after being diagnosed with high blood pressure should I wait to apply?

For the best rates, waiting 3-6 months after diagnosis allows you to establish a track record of controlled blood pressure with medication. Insurance companies like to see consistent, stable readings rather than just one or two good numbers right after starting treatment. However, if you need coverage immediately, you can apply right away—you’ll just likely pay slightly higher premiums. If you’re over 75, don’t wait at all; the premium increases from aging will outweigh any benefit from waiting. For most seniors in their 60s and early 70s, waiting 2-3 months to show medication effectiveness is a good balance between getting coverage soon and securing better rates.

Do I need life insurance if I already have high blood pressure?

This depends on your personal situation, but many seniors with high blood pressure do need life insurance. Consider getting coverage if you want to: cover final expenses so your family doesn’t face funeral costs ($7,000-$12,000 average), pay off remaining debts like mortgages or credit cards, replace income if your spouse depends on your Social Security or pension, leave an inheritance to children or grandchildren, or cover estate taxes and legal fees. High blood pressure slightly increases your mortality risk, which actually makes life insurance more important, not less. Even with hypertension, you’re likely to live many more years, but having coverage ensures your family is protected regardless of what happens.

Can life insurance companies drop you if your blood pressure gets worse?

For most seniors with high blood pressure, whole life insurance is typically the better choice. Here’s why: whole life covers you for your entire lifetime (term expires after 10-30 years when you’ll be older and harder to insure), whole life builds cash value you can borrow against in emergencies, premiums never increase with whole life while term premiums skyrocket if you need to renew after the term ends, and most simplified and guaranteed issue policies for seniors are whole life anyway. Term life can work if you only need temporary coverage (like until your mortgage is paid off) and your blood pressure is very well-controlled. However, if there’s any chance your hypertension could worsen, whole life ensures you’ll always have coverage.

What Are the Best Life Insurance Companies for High Blood Pressure?

Many life insurance companies work with applicants who have high blood pressure. The best company often depends on your age, blood pressure readings, medications, tobacco use, and other health conditions. Companies frequently considered by seniors with controlled hypertension include Mutual of Omaha, Prudential, Protective, Banner Life, and AIG.

Tips for Getting the Best Rates

Here are some insider strategies to improve your chances and reduce your costs while applying for life insurance for seniors with high blood pressure.

1. Time Your Medical Exam Strategically

If applying for fully underwritten coverage:

- Schedule your exam for morning when BP is typically lower

- Avoid caffeine for 24 hours before

- Get good sleep the night before

- Take your blood pressure medication as prescribed

- Don’t exercise vigorously the morning of the exam

- Arrive early to relax before the exam

- Practice deep breathing if nervous

2. Document Your Home Blood Pressure Readings

Keep a log showing:

- Readings taken at the same time daily for 2-4 weeks

- Results showing consistent control

- Your monitoring equipment information

Present this to the insurance company if your medical exam shows high readings due to white coat syndrome.

3. Optimize Your Application Timing

Best Times to Apply:

- 3-6 months after starting new blood pressure medication (once you can show it’s working)

- After losing weight if overweight (each 10 pounds can help)

- 12+ months after quitting smoking (to get non-smoker rates)

- After 6 months of consistent good readings

Worst Times to Apply:

- Right after diagnosis (no control track record)

- During medication changes (shows instability)

- After hospitalization (wait 3-6 months)

- During stressful life events that spike BP

4. Bundle Other Health Improvements

If you’re working on blood pressure control, also:

- Lose weight if needed (BMI affects rates significantly)

- Get cholesterol under control

- Exercise regularly (helps both BP and underwriting)

- Reduce alcohol consumption

- Manage stress

Improving multiple health factors simultaneously can move you into better rate classes.

5. Consider Applying Through Multiple Companies

If working with an independent agent:

- They can submit to several companies simultaneously

- Different insurers have different underwriting standards

- One company might offer standard rates while another offers table ratings

- There’s no penalty for multiple applications

6. Ask About Rate Reconsideration

If you’re declined or rated higher than expected:

- Provide additional documentation of good control

- Submit more home blood pressure readings

- Get a letter from your doctor explaining management

- Ask if you can reapply after improving control for 6 months

7. Take Advantage of Age-Based Pricing

Life insurance rates increase dramatically with age:

- Every year you wait costs 8-12% more

- Waiting from age 65 to 66 might cost $500-800/year more in premiums

- Even with slightly high BP now, applying sooner is often cheaper than waiting for perfect control

Do the math: If getting better control would save you $30/month but you wait a year (aging you into the next age bracket), you might actually pay $50/month more overall.

Taking Action: Your Next Steps

Getting life insurance with high blood pressure is straightforward once you know your options. Here’s your action plan:

This Week:

- Check your blood pressure multiple times and record the results

- Make a list of all your blood pressure medications and dosages

- Note when you were first diagnosed with hypertension

- Document any related health conditions

- Calculate how much coverage you actually need

This Month:

- Decide which type of policy fits your situation (traditional, simplified, or guaranteed)

- Get quotes from at least 3-5 insurance companies

- Compare rates and coverage options

- Consider whether working with an independent agent makes sense

- Check if you have any group life insurance options available

Before Applying:

- Ensure your blood pressure has been stable for at least 2-3 months

- Have your doctor’s contact information ready

- Prepare to answer questions about your health honestly and completely

- Choose your beneficiaries

- Review your budget to confirm affordable premiums

Remember:

- Don’t let high blood pressure stop you from protecting your family

- Options exist for every blood pressure level

- The sooner you apply, the better (premiums increase with age)

- Being honest about your hypertension ensures valid coverage

- Medication-controlled blood pressure is very common and insurable

High blood pressure doesn’t define you, and it certainly doesn’t disqualify you from life insurance. Take the first step today—your family’s financial security is worth it.

Conclusion

Having high blood pressure as a senior doesn’t mean you can’t get affordable life insurance protection. With nearly half of all American adults dealing with hypertension, insurance companies have developed clear, reasonable guidelines for evaluating applicants with this common condition.

The key points to remember:

✓ Well-controlled hypertension (below 140/90) qualifies for standard or near-standard rates ✓ Simplified issue policies offer convenient coverage without medical exams for Stage 1-2 hypertension ✓ Guaranteed issue ensures coverage for any blood pressure level, no matter how high ✓ Medication compliance actually helps your application by showing responsible management ✓ Multiple options exist regardless of your specific situation ✓ Acting now is better than waiting—premiums increase 8-12% each year you age

Whether your blood pressure is beautifully controlled at 125/80 or stubbornly high at 165/95, there’s a life insurance solution that fits your needs and budget. Don’t let hypertension prevent you from giving your family the financial protection they deserve.

Start comparing quotes today and take the first step toward peace of mind. You’ve managed your high blood pressure—now manage your family’s financial future with the right life insurance coverage.

Disclaimer: This article provides general information about life insurance for seniors with high blood pressure and should not be considered medical, financial, or legal advice. Life insurance availability, rates, and underwriting standards vary significantly by company, state, individual health circumstances, and specific blood pressure readings. Premium estimates are approximate and for illustrative purposes only. Always consult with licensed insurance professionals and your healthcare provider when making insurance and medical decisions. Blood pressure classifications and recommendations may differ from medical guidelines. Individual results will vary based on age, gender, blood pressure readings, medications, overall health, smoking status, and other factors assessed during underwriting.