Life Insurance for Seniors with High Cholesterol: Guide (2025)

Posted in Life Insurance w/ Pre-existing Conditions on December 3, 2025 last updated on May 16, 2026

Posted in Life Insurance w/ Pre-existing Conditions on December 3, 2025 last updated on May 16, 2026

Can Seniors with High Cholesterol Get Life Insurance?

Yes, seniors with high cholesterol can often qualify for life insurance, especially if cholesterol levels are controlled with medication or lifestyle changes. Approval and rates depend on cholesterol ratios, overall cardiovascular health, and related medical conditions.

Here’s something that might surprise you: when seniors call me worried about getting life insurance because they have high cholesterol, I often breathe a small sigh of relief. Not because high cholesterol is good for you—of course it’s not—but because in the world of life insurance, controlled high cholesterol is one of the easier conditions to work with. Some insurers are significantly more flexible with cardiovascular risk factors and chronic health conditions than others.

I’ll be honest with you. If you told me you have diabetes and high blood pressure and COPD, I’d need to carefully strategize your application. But if you tell me your only issue is high cholesterol that you’re managing with medication? We can usually get you approved without much trouble at all.

Life insurance for seniors with high cholesterol is not only available—it’s often quite affordable. I’ve helped hundreds of seniors with cholesterol levels well above 200 get approved for coverage at reasonable rates. Some even qualified for preferred rates because everything else about their health was excellent.

The key thing to understand is this: insurance companies don’t just look at your cholesterol number. They look at the whole picture. Are you taking your statin? Is your cholesterol trending down or stable? Do you see your doctor regularly? Are you following treatment? These factors often matter more than the number itself.

In this guide, I’m going to walk you through everything about life insurance for seniors with high cholesterol: how insurance companies really evaluate it, what cholesterol numbers mean to underwriters, why being on a statin can actually help your approval, what you’ll pay, which companies are most cholesterol-friendly, and exactly how to apply for the best outcome.

Whether your cholesterol is mildly elevated at 210 or significantly high at 280, whether you’re on one medication or three, whether you’ve had high cholesterol for two years or twenty, you’ll learn your real options and how to maximize your chances of approval at good rates.

Understanding High Cholesterol and Life Insurance

Before we talk about approval odds and rates, you need to understand what insurance underwriters actually think about cholesterol. This knowledge helps you present your situation in the best possible light.

Life insurance companies usually evaluate more than just your total cholesterol number.

Underwriters commonly review:

- Total cholesterol

- LDL (“bad” cholesterol)

- HDL (“good” cholesterol)

- Triglycerides

- Cholesterol-to-HDL ratio

In many cases, insurers focus heavily on the cholesterol ratio because it helps estimate cardiovascular risk.

Applicants with stable ratios and controlled cholesterol often receive significantly better underwriting outcomes than applicants with uncontrolled cholesterol and additional heart-related conditions.

What Insurance Companies Really Care About

When you apply for life insurance, underwriters evaluate your cholesterol through a specific lens. Here’s what they’re looking for:

Your Total Cholesterol Number

This is the big number everyone talks about, but it’s actually not the most important factor. Here’s how underwriters generally categorize it:

Desirable (Under 200 mg/dL):

- Minimal impact on life insurance

- May qualify for preferred rates if everything else is good

- Little to no rate increase

Borderline High (200-239 mg/dL):

- Very common in seniors (about 45% fall here)

- Usually approved with standard rates

- Slight rate increase (0-15%) depending on other factors

- Most companies very comfortable with this range if treated

High (240+ mg/dL):

- Requires more careful evaluation

- Usually approved but with table ratings (15-50% increase)

- Being on medication and showing improvement helps significantly

- Untreated high cholesterol is viewed much more negatively

Very High (300+ mg/dL):

- Significant concern for underwriters

- Requires strong management and stable history

- May face higher ratings or need guaranteed issue

- But still approvable with right approach

Your LDL Cholesterol (The “Bad” Cholesterol)

This is actually more important to underwriters than total cholesterol:

Optimal (Under 100 mg/dL):

- Best possible scenario

- Can help offset higher total cholesterol

- Preferred rates often available

Near Optimal (100-129 mg/dL):

- Still very good

- Standard rates likely

- No significant concerns

Borderline High (130-159 mg/dL):

- Manageable

- Standard to slight table rating

- Treatment compliance important

High (160-189 mg/dL):

- More significant concern

- Table rating likely (15-30%)

- Need good treatment history

Very High (190+ mg/dL):

- Major red flag

- Requires excellent management

- Higher ratings (25-50%+)

- Must be actively treated

Your HDL Cholesterol (The “Good” Cholesterol)

High HDL actually helps your application:

Poor (Under 40 mg/dL for men, under 50 mg/dL for women):

- Increases underwriting concern

- Combined with high LDL is problematic

Good (40-59 mg/dL):

- Acceptable to underwriters

- No negative impact

Excellent (60+ mg/dL):

- Protective factor

- Can offset moderately high LDL

- Underwriters view this very positively

I’ve seen seniors with total cholesterol of 230 get approved at standard rates because their HDL was 75 and their LDL was 140. The good HDL compensated for the elevated total.

Your Triglycerides

Often overlooked but important:

Normal (Under 150 mg/dL):

- No impact on underwriting

Borderline High (150-199 mg/dL):

- Minor concern

- Usually no rate impact if controlled

High (200-499 mg/dL):

- Definite concern

- Rate impact likely (10-25%)

- Need treatment and control

Very High (500+ mg/dL):

- Serious red flag

- Significant rate impact (30-50%+)

- Associated with pancreatitis risk

- May need guaranteed issue

Your Cholesterol Ratio

Total cholesterol divided by HDL cholesterol:

Ideal (Under 3.5):

- Excellent

- Helps your application

Good (3.5-5.0):

- Acceptable

- Standard rates

Moderate Risk (5.0-6.0):

- Some concern

- Slight rate impact

High Risk (Over 6.0):

- Significant concern

- Table rating likely

Example: If your total cholesterol is 240 and your HDL is 60, your ratio is 4.0—which is actually good despite the elevated total. Underwriters notice this.

What Really Matters Most

After working with hundreds of seniors with high cholesterol, here’s what I’ve learned matters most to insurance companies:

Treatment Compliance Trumps Numbers: A senior with cholesterol of 260 who takes their statin daily, sees their doctor regularly, and has stable levels looks better than someone with cholesterol of 220 who refuses treatment and is non-compliant.

Trends Matter More Than Single Numbers: Cholesterol trending down from 280 to 240 with treatment? Excellent. Cholesterol climbing from 200 to 260 despite treatment? Concerning.

Related Conditions Compound: High cholesterol alone is manageable. High cholesterol + diabetes + high blood pressure = compound risk. Each condition amplifies the others.

Medication Type Signals Severity: One low-dose statin suggests manageable cholesterol. Multiple high-dose medications plus Zetia plus PCSK9 inhibitors suggest severe, resistant cholesterol.

Cardiovascular History Is The Real Concern: Underwriters aren’t really worried about cholesterol—they’re worried about heart attacks and strokes. High cholesterol with no cardiac events is very different from high cholesterol with prior heart attack.

The Good News for Seniors

Here’s what works in your favor:

High Cholesterol Is Extremely Common: Nearly 94 million American adults have high cholesterol. Insurance companies have decades of data and know exactly how to price it. This isn’t a mysterious condition that scares underwriters.

Statins Are Safe and Effective: Insurance companies love statins. They know these drugs work, reduce cardiac risk, and have an excellent safety profile. Being on a statin often improves your approval odds.

Many Seniors Get Standard Rates: If your cholesterol is in the 200-230 range, well-controlled on a single medication, with good HDL and no cardiac history, you often qualify for standard rates—meaning no rate increase at all.

Treatment Shows You Care: Taking medication daily shows underwriters you’re actively managing your health. This compliance is viewed very positively.

Can You Get Life Insurance for Seniors with High Cholesterol? Real Scenarios

Let me answer the big question directly: Can you get life insurance with high cholesterol? Absolutely yes—but your approval odds and rates depend on your specific situation. Here are real scenarios:

Scenario 1: Mildly Elevated, Well-Controlled (Best Case)

Profile:

- Total cholesterol: 210-230 mg/dL

- LDL: 130-150 mg/dL

- HDL: 50-65 mg/dL

- On single low-dose statin (like 10mg Lipitor)

- Levels stable for 2+ years

- No other cardiac risk factors

- Regular doctor visits

Insurance Outcome:

- ✓ Easy approval for simplified issue

- ✓ Often standard rates (no increase)

- ✓ May qualify for preferred rates if everything else is excellent

- ✓ Wide company selection

- ✓ Fast approval (24-48 hours)

Real Example: Dorothy, 69, has total cholesterol of 218, LDL of 142, HDL of 58. Takes 10mg Lipitor daily. No other health issues. Applied to AARP/New York Life, got approved at standard rates with no increase. Pays $88/month for $20,000 coverage—same as if her cholesterol were perfect.

Key Insight: Mildly elevated cholesterol that’s well-managed is almost a non-issue for life insurance.

Scenario 2: Moderately High, Treated (Very Common)

Profile:

- Total cholesterol: 240-270 mg/dL

- LDL: 160-180 mg/dL

- HDL: 45-55 mg/dL

- On moderate-dose statin (like 40mg Lipitor or 20mg Crestor)

- Levels improved from higher numbers

- No cardiac history

- Good compliance

Insurance Outcome:

- ✓ Good approval odds for simplified issue

- ✓ Slight to moderate table rating (10-25% increase)

- ✓ Most companies comfortable

- ✓ Approval within 48-72 hours

- ✓ Affordable rates for most budgets

Real Example: Robert, 72, has total cholesterol of 255, LDL of 175, HDL of 52. Takes 40mg Lipitor daily. Cholesterol was 290 three years ago before treatment. Applied to Mutual of Omaha, approved with 15% table rating. Pays $168/month for $25,000 coverage (would have been $145/month with perfect cholesterol).

Key Insight: Showing improvement with treatment significantly helps your case. Robert’s approval emphasized his 35-point drop from 290.

Scenario 3: High But Stable (More Challenging)

Profile:

- Total cholesterol: 280-310 mg/dL

- LDL: 190-220 mg/dL

- HDL: 40-50 mg/dL

- On high-dose statin, possibly multiple medications

- Levels stable but not decreasing much

- No cardiac events

- Seeing cardiologist regularly

Insurance Outcome:

- ✓ Simplified issue possible at cholesterol-friendly companies

- ✓ Moderate to high table rating (25-50% increase)

- ✓ More selective company approval

- ✓ Guaranteed issue is reliable backup option

- ✓ Higher premiums but coverage available

Real Example: Margaret, 74, has total cholesterol of 295, LDL of 210, HDL of 45. Takes high-dose Crestor plus Zetia. Levels have been stable at this range for 5 years despite treatment. Applied to simplified issue at AIG, approved with 35% table rating. Pays $225/month for $20,000 coverage. She accepted this because guaranteed issue would have cost $240/month for same coverage at her age.

Key Insight: Even significantly high cholesterol gets approved if you’re treating it aggressively and have no cardiac complications.

Scenario 4: Very High or With Complications (Most Difficult)

Profile:

- Total cholesterol: 320+ mg/dL

- LDL: 240+ mg/dL

- Triglycerides: 400+ mg/dL

- Multiple medications or on PCSK9 inhibitors

- History of angina or prior cardiac event

- Recent medication changes

Insurance Outcome:

- ✗ Likely declined for simplified issue

- ✓ Guaranteed issue is best option

- ✓ 100% approval certainty

- ✓ Higher premiums but gets you covered

- ✓ 2-year waiting period applies

Real Example: James, 77, has total cholesterol of 340, LDL of 260, triglycerides of 480. Had angina 3 years ago (stent placed). On multiple medications. Applied for simplified issue, declined. Immediately applied for guaranteed issue at Foresters, approved instantly. Pays $285/month for $15,000 coverage. Waiting period means years 1-2 return premiums, year 3+ pays full benefit.

Key Insight: Very high cholesterol with cardiac complications usually requires guaranteed issue, but you absolutely can get covered.

Scenario 5: High Cholesterol With Multiple Conditions

Profile:

- Total cholesterol: 250+ mg/dL

- Also has diabetes and high blood pressure

- On multiple medications for various conditions

- All conditions reasonably controlled

Insurance Outcome:

- ✓ Possible approval for simplified issue at lenient companies

- ✓ Compound table rating (conditions stack)

- ✓ Guaranteed issue is reliable option

- ✓ Rate impact from all conditions combined

Real Example: Helen, 70, has cholesterol of 265, type 2 diabetes (A1C 7.2), and high blood pressure (controlled). Takes statin, metformin, and blood pressure medication. Applied to AIG (good with multiple conditions), approved with 40% table rating. Pays $195/month for $15,000 coverage. The cholesterol alone might have been 15% rating, diabetes another 20%, BP another 10%—they compound.

Key Insight: Multiple conditions amplify each other’s impact, but approval is still very possible.

| Cholesterol Situation | Typical Underwriting Outcome |

|---|---|

| Controlled cholesterol with medication | Standard or favorable |

| Mildly elevated cholesterol | Moderate rates |

| High cholesterol with heart disease | Higher premiums |

| High cholesterol + diabetes | Increased underwriting scrutiny |

| Uncontrolled cholesterol with smoking | Higher-risk classification |

What You’ll Actually Pay: Real Rates

Let’s talk real numbers. Here’s what life insurance for seniors with high cholesterol actually costs based on cholesterol levels and policy types.

Controlled Cholesterol (200-240) – Simplified Issue

Female, Age 65, $15,000 Coverage:

- No cholesterol issues: $63/month

- Controlled cholesterol: $65-73/month

- Increase: $2-10/month

Male, Age 70, $15,000 Coverage:

- No cholesterol issues: $105/month

- Controlled cholesterol: $110-125/month

- Increase: $5-20/month

Female, Age 75, $25,000 Coverage:

- No cholesterol issues: $185/month

- Controlled cholesterol: $195-215/month

- Increase: $10-30/month

Moderately High Cholesterol (240-280) – Simplified Issue

Female, Age 65, $15,000 Coverage:

- No cholesterol issues: $63/month

- Moderate cholesterol: $73-85/month

- Increase: $10-22/month

Male, Age 70, $15,000 Coverage:

- No cholesterol issues: $105/month

- Moderate cholesterol: $125-145/month

- Increase: $20-40/month

Female, Age 75, $25,000 Coverage:

- No cholesterol issues: $185/month

- Moderate cholesterol: $225-260/month

- Increase: $40-75/month

High Cholesterol (280+) – Simplified Issue (If Approved)

Female, Age 65, $15,000 Coverage:

- No cholesterol issues: $63/month

- High cholesterol: $85-105/month

- Increase: $22-42/month

Male, Age 70, $15,000 Coverage:

- No cholesterol issues: $105/month

- High cholesterol: $145-175/month

- Increase: $40-70/month

Guaranteed Issue Rates (Any Cholesterol Level)

If you can’t get simplified issue or rates are too high, guaranteed issue is always available. These rates are the same regardless of cholesterol:

$15,000 Coverage – Female:

- Age 65: $89/month

- Age 70: $118/month

- Age 75: $142/month

- Age 80: $178/month

$15,000 Coverage – Male:

- Age 65: $118/month

- Age 70: $135/month

- Age 75: $188/month

- Age 80: $248/month

Important Note: Sometimes guaranteed issue is actually cheaper than simplified issue with heavy table ratings. Always compare both options.

👉 Want to compare companies that work best for applicants with high cholesterol? Explore personalized options in under 60 seconds.

Real Cost Comparison

Scenario: 70-year-old female, total cholesterol 255, $15,000 coverage

Option 1 – Simplified Issue at Mutual of Omaha:

- Approved with 15% table rating

- Premium: $135/month

- No waiting period

- Annual cost: $1,620

Option 2 – Guaranteed Issue at Foresters:

- Instant approval

- Premium: $118/month

- 2-year waiting period

- Annual cost: $1,416

- Saves: $204/year vs. simplified

In this case, guaranteed issue is actually cheaper despite the waiting period! This happens more often than people realize.

Factors That Impact Your Rate

Beyond base cholesterol numbers. Having multiple health conditions can cause rates to be higher than just having high cholesterol.

Statin Use (Can Lower Rates): Being on a statin and showing compliance often results in better rates than being untreated. Underwriters see this as proactive health management.

HDL Levels (Can Improve Rates): High HDL (65+) can offset elevated total cholesterol. Some companies give you credit for protective HDL.

Recent Trends (Major Impact):

- Cholesterol dropping: Helps rates

- Cholesterol rising: Hurts rates

- Stable for 3+ years: Neutral to positive

Related Conditions (Compound Ratings):

- Cholesterol alone: 0-25% increase

- Cholesterol + diabetes: 30-50% increase

- Cholesterol + diabetes + hypertension: 50-75% increase

Smoking Status (Doubles Rates): High cholesterol + smoking = 100%+ rate increase. Don’t smoke with high cholesterol.

Cardiac History (Major Impact):

- No cardiac events: Manageable impact

- Prior heart attack: 50-100%+ increase or guaranteed issue only

- Multiple cardiac events: Guaranteed issue only

Best Life Insurance Companies for High Cholesterol

Not all insurance companies treat cholesterol the same way. Here are the most cholesterol-friendly options:

1. Mutual of Omaha – Best Overall

Why They’re Best:

- Very reasonable about controlled cholesterol

- Won’t penalize mildly elevated levels (200-230)

- Understand seniors and cholesterol correlation

- Look at whole health picture, not just one number

- Both simplified and guaranteed issue available

Cholesterol-Specific Strengths:

- Will approve cholesterol up to 280 on simplified issue

- Give credit for high HDL levels

- Reward treatment compliance and stability

- Reasonable table ratings (usually 10-20% for moderate cholesterol)

Best For:

- Total cholesterol 200-270

- Well-controlled on medication

- Seniors wanting established company

Application Tips:

- Mention years of stability if applicable

- Provide recent lipid panel showing all numbers (not just total)

- Emphasize HDL if it’s good (60+)

- Note medication compliance

2. AIG (American General) – Best for Moderate to High Cholesterol

Why They’re Best:

- Specialize in health conditions

- More lenient on cholesterol than most

- Experienced underwriters understand nuance

- Will work with borderline cases

Cholesterol-Specific Strengths:

- Approve cholesterol into the 300s if well-managed

- Understand cholesterol in context (ratios, trends, HDL)

- Won’t auto-decline high numbers if treatment is aggressive

- Reasonable ratings even for elevated levels

Best For:

- Total cholesterol 260-320

- Multiple medications but stable

- History of working to control levels

Application Tips:

- Apply by phone with agent guidance

- Provide complete medication history showing treatment escalation

- Mention any cholesterol reductions achieved

- Include cardiologist notes if seeing one

3. AARP/New York Life – Best for Mild Cholesterol

Why They’re Best:

- Group rates through AARP membership

- Very good pricing for well-controlled conditions

- Backed by AAA-rated New York Life

- Simple application process

Cholesterol-Specific Strengths:

- Excellent rates for cholesterol under 240

- Minimal impact for well-controlled levels

- Health questions are straightforward

- Fast approval for uncomplicated cases

Best For:

- Total cholesterol under 250

- On single medication

- AARP members (anyone can join for $16/year)

- Wanting larger coverage ($50,000-$100,000)

Limitations:

- Will decline cholesterol over 280-300

- More strict on multiple conditions

- Maximum age 80

4. Foresters Financial – Best Guaranteed Issue

Why They’re Best:

- True guaranteed acceptance (no health questions)

- Cholesterol level doesn’t matter at all

- Instant online approval

- Simple process

Cholesterol-Specific Advantages:

- Your cholesterol could be 400—doesn’t matter

- Same rate whether you have perfect cholesterol or very high

- No questions about medications or cardiac history

- Instant approval regardless

Best For:

- Cholesterol over 300

- Multiple cardiac risk factors

- Previous declines from simplified issue

- Anyone wanting guaranteed approval

Important Notes:

- 2-3 year waiting period for natural death

- Accidental death covered from day one

- Sometimes cheaper than simplified with heavy ratings

5. Globe Life – Best Budget Option

Why They’re Best:

- Often lowest premiums in industry

- Simple underwriting

- Reasonable about cholesterol

- Both policy types available

Cholesterol-Specific Strengths:

- Won’t over-penalize moderate cholesterol (230-260)

- Straightforward health questions

- Good approval rates for controlled cases

- Budget-friendly premiums

Best For:

- Price-conscious seniors

- Total cholesterol 200-270

- Good compliance history

- Wanting absolute lowest premium

Consideration:

- Customer service reviews are mixed

- Less personalized attention than others

Company Comparison Chart

| Company | Cholesterol Range | Rate Impact | Best For | Max Age |

|---|---|---|---|---|

| Mutual of Omaha | 200-280 | Low-Moderate | Overall best | 85 |

| AIG | 200-320 | Moderate | High cholesterol | 85 |

| AARP/NY Life | Under 250 | Low | Mild cholesterol | 80 |

| Foresters | Any level | N/A | Guaranteed | 80 |

| Globe Life | 200-270 | Low-Moderate | Budget | 85 |

👉 Compare the best life insurance companies for seniors with health problems to explore your options.

Do Statins Affect Life Insurance Approval?

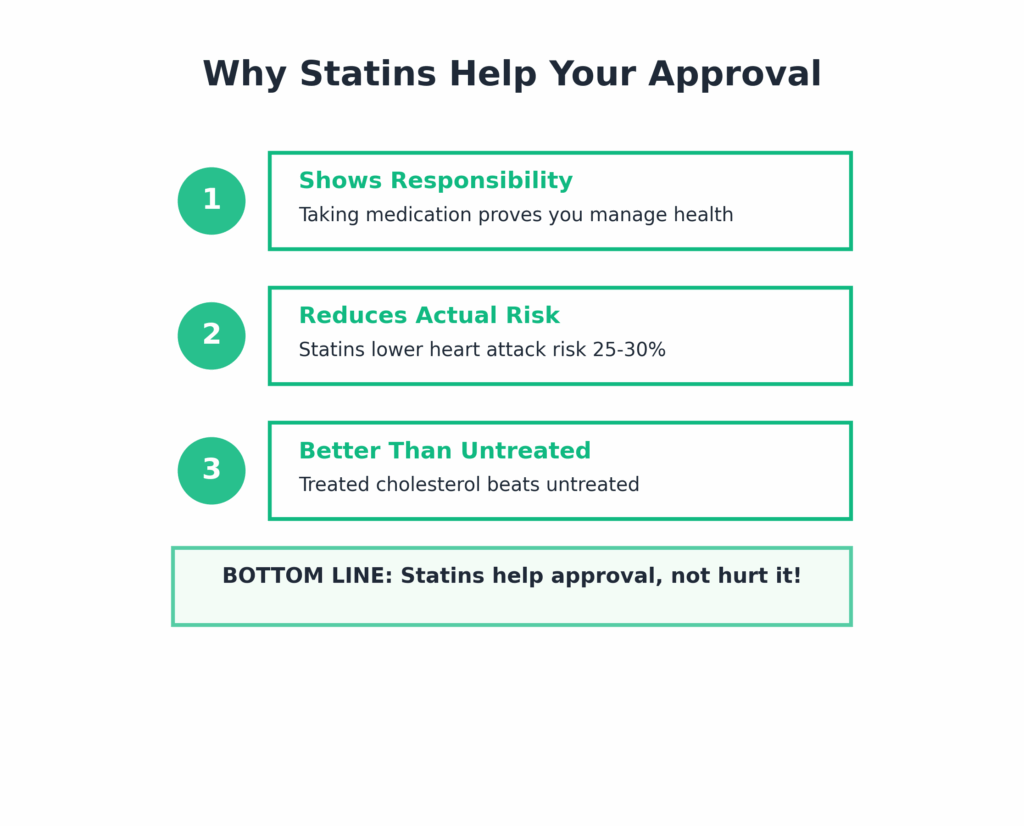

Taking statins usually does not hurt life insurance approval and may actually improve underwriting outcomes because it shows your cholesterol is being actively managed. Insurance companies often care more about cholesterol stability and overall cardiovascular health than the medication itself.

Applicants with stable cholesterol levels while taking medication often receive better rates than applicants with untreated or uncontrolled cholesterol.

Statins Show You’re Managing Your Health

Underwriters View This Positively:

- Demonstrates you see doctors regularly

- Shows medication compliance

- Proves you’re taking health seriously

- Indicates stable, managed condition vs. ignored problem

Real Impact: A senior with cholesterol of 240 on 20mg Lipitor will usually get better rates than a senior with cholesterol of 230 who refuses treatment. The treated person is viewed as lower risk.

Statins Reduce Your Actual Risk

Insurance Companies Know the Data:

- Statins reduce heart attack risk by 25-30%

- Statins reduce stroke risk by 20-25%

- Statins lower LDL cholesterol by 30-50%

- Long-term statin use shows excellent safety

Underwriter Perspective: You’re actively reducing your cardiac risk with proven medication. This makes you a better risk than someone with untreated high cholesterol.

Common Statins and How Insurance Companies View them

Low-Dose Statins (Best for Approval):

- Lipitor (atorvastatin) 10-20mg

- Crestor (rosuvastatin) 5-10mg

- Zocor (simvastatin) 20-40mg

- Pravachol (pravastatin) 40mg

Signal to Underwriters: “Mild to moderate cholesterol, well-controlled with standard treatment”

Moderate-Dose Statins:

- Lipitor 40-80mg

- Crestor 20-40mg

- Zocor 80mg

Signal to Underwriters: “Moderate to high cholesterol requiring higher doses but responding to treatment”

High-Dose or Multiple Medications:

- Maximum-dose statins

- Statin + Zetia (ezetimibe)

- Statin + PCSK9 inhibitors (Repatha, Praluent)

Signal to Underwriters: “Significant cholesterol requiring aggressive treatment—but patient is compliant”

What If You’re Not On Medication?

Two Scenarios:

Scenario 1: Cholesterol Under 200, No Medication Needed

- Excellent for approval

- May qualify for preferred rates

- Underwriters love “naturally healthy” lipid profiles

Scenario 2: Cholesterol Over 220, Refusing Treatment

- Red flag for underwriters

- Suggests non-compliance or denial

- May result in decline or high ratings

- Much worse than being on medication

The Takeaway: If your doctor recommends a statin, take it. It will help your life insurance approval, not hurt it.

Addressing Statin Concerns

“I Don’t Want To Take Medication” I understand this hesitation. But for life insurance purposes, being on a statin is viewed positively. It shows you’re managing your health proactively.

“Statins Have Side Effects” Some people do experience side effects (muscle pain, digestive issues). But underwriters know that millions take statins safely. Having minor side effects doesn’t hurt your approval.

“I Want To Try Diet and Exercise First” That’s great! But if your cholesterol remains elevated (220+) for 6-12 months despite lifestyle changes, underwriters will view untreated high cholesterol negatively. Consider medication if diet alone isn’t working.

How to Apply: Step-by-Step Strategy

Let me walk you through the smartest way to apply for life insurance with high cholesterol to maximize approval and minimize rates.

Step 1: Get Your Recent Cholesterol Numbers

What You Need:

- Total cholesterol

- LDL cholesterol

- HDL cholesterol

- Triglycerides

- Date of last test (within 12 months is best)

Where To Find It:

- Request “lipid panel” results from your doctor

- Check your patient portal online

- Call your doctor’s office for a copy

Why This Matters: Knowing your exact numbers before applying helps you choose the right strategy and company. Don’t guess.

Step 2: Gather Your Medication Information

Document These Details:

- Exact medication names (Lipitor, Crestor, etc.)

- Dosages (10mg, 20mg, 40mg, etc.)

- How long you’ve been taking each

- Any recent changes in medications

- Your compliance (do you take it daily as prescribed?)

Pro Tip: Create a simple medication list with start dates. This shows organization and compliance to underwriters.

Step 3: Calculate Your Cholesterol Ratio

Simple Formula: Total Cholesterol ÷ HDL Cholesterol = Your Ratio

Examples:

- Total 220, HDL 55 → Ratio 4.0 (good)

- Total 260, HDL 65 → Ratio 4.0 (good despite higher total)

- Total 200, HDL 35 → Ratio 5.7 (concerning despite lower total)

Why This Helps: A good ratio (under 5.0) can offset higher total cholesterol. Mention this in your application if it’s favorable.

Step 4: Assess Your Situation

Answer These Questions Honestly:

- What’s your total cholesterol? (Under 240 / 240-280 / Over 280)

- What’s your LDL? (Under 160 / 160-190 / Over 190)

- What’s your HDL? (Under 40 / 40-60 / Over 60)

- Are you on medication? (Yes / No)

- How long have levels been stable? (Under 1 year / 1-3 years / 3+ years)

- Have you had any cardiac events? (Heart attack, stroke, stents, etc.)

- Do you have other conditions? (Diabetes, high BP, etc.)

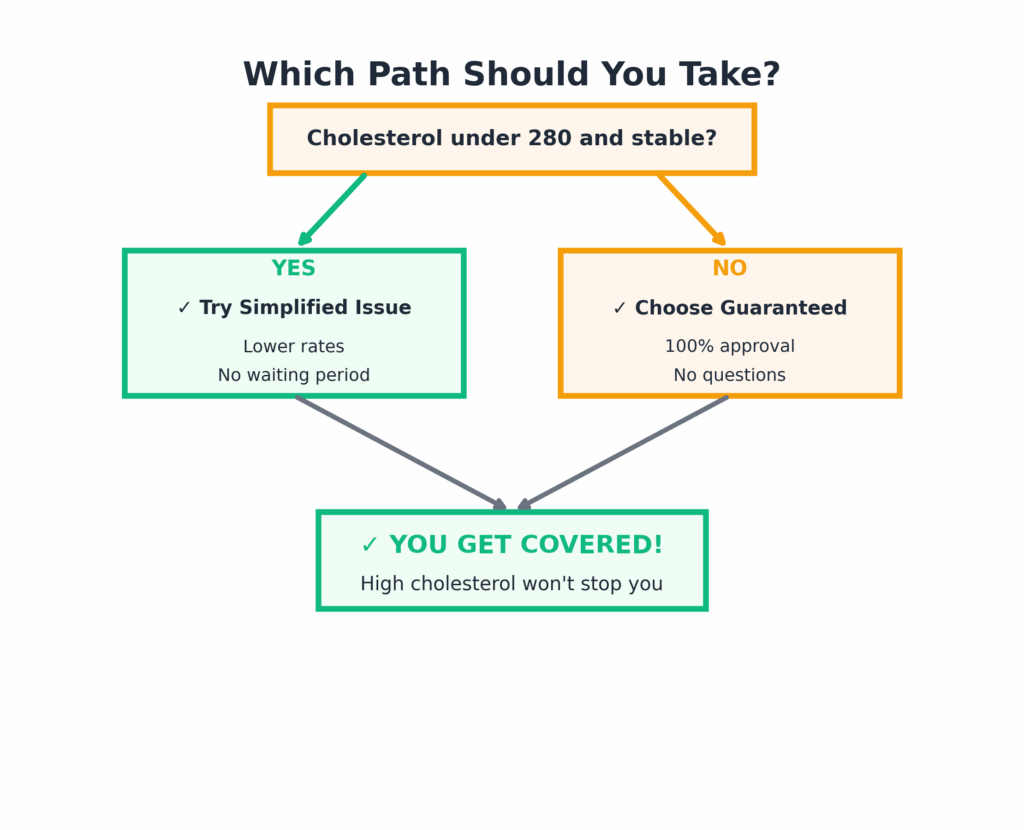

Your Strategy Based on Answers:

Mostly favorable (cholesterol under 260, on medication, stable, no cardiac events): → Try simplified issue first for best rates

Mixed (cholesterol 260-300, multiple medications, stable but high, no cardiac events): → Get quotes from both simplified and guaranteed issue

Mostly challenging (cholesterol 300+, cardiac events, multiple conditions): → Go straight to guaranteed issue for certainty

Step 5: Get Multiple Quotes

For Simplified Issue, Contact:

- Mutual of Omaha

- AIG

- AARP/New York Life (if member)

- Globe Life

- One independent agent representing multiple companies

For Guaranteed Issue, Contact:

- Mutual of Omaha

- Foresters Financial

- Globe Life

- Gerber Life

Why Multiple Quotes: Rates for the same person with same cholesterol can vary 25-40% between companies. Shopping saves $30-60/month = $360-$720/year.

Step 6: Complete Application Strategically

Answer Health Questions Carefully:

Question: “Do you have high cholesterol?” ✓ Correct: “Yes, I have high cholesterol managed with Lipitor. My latest levels are total 245, LDL 165, HDL 58, stable for 3 years.” ✗ Wrong: Just “Yes” (too vague) ✗ Wrong: “Yes, but it’s controlled” (be specific with numbers)

Question: “What medications do you take?” ✓ Correct: “Lipitor (atorvastatin) 20mg once daily, started in 2020, excellent compliance” ✗ Wrong: “A statin” (too vague) ✗ Wrong: “Cholesterol medication” (be specific)

Question: “Have you had any cardiac events?” ✓ Correct: “No cardiac events. No heart attack, stroke, or procedures.” ✓ Also Correct: “Yes, I had a stent placed in 2021 for one blocked artery, fully recovered, on medications, no symptoms since.” ✗ Wrong: “I don’t think so” (be certain)

Question: “When was your last cholesterol test?” ✓ Correct: “March 2024, results were total 238, LDL 158, HDL 62” ✗ Wrong: “A few months ago” (be specific)

Step 7: Emphasize Positive Factors

Proactively Mention:

- “My cholesterol has been stable at this level for X years”

- “My HDL is 65, which my doctor says is excellent”

- “I’ve been on the same medication for 5 years with no issues”

- “My last stress test was normal” (if applicable)

- “I take my medication every day without fail”

Provide Context Where Helpful: “My cholesterol was 290 five years ago. With medication and diet changes, it’s now 245 and stable. My doctor is very pleased with the improvement.”

This shows you’re actively managing your health and succeeding.

Step 8: Follow Up Promptly

If Company Requests:

- Additional medical records → Provide within 24 hours

- Attending physician statement → Contact doctor same day

- Clarification on medications → Respond immediately

- Recent lipid panel → Send latest test results

Fast Response Benefits:

- Shows you’re organized and serious

- Speeds up approval process

- Demonstrates transparency

Step 9: Review Your Approval

When You Receive Approval:

- Verify premium matches quote

- Check coverage amount is correct

- Understand any table rating applied

- Confirm beneficiaries listed properly

- Ask about rating if higher than expected

If Declined:

- Ask specific reason for decline

- Immediately apply for guaranteed issue

- Don’t take decline personally—companies vary

If Rates Are Higher Than Expected:

- Compare to guaranteed issue rates

- Ask what drove the rating

- Consider shopping another company

- Sometimes guaranteed is cheaper!

Common Application Mistakes

Mistake #1: Not Mentioning HDL If your HDL is good (60+), say so! Don’t assume the underwriter will notice or give you credit for it.

Mistake #2: Being Vague About Stability “Cholesterol has been the same for years” is better stated as “Total cholesterol stable between 240-250 for past 4 years per annual lipid panels.”

Mistake #3: Not Explaining Medication Changes If you recently switched from Lipitor to Crestor, explain why (better control, side effects, cost). Unexplained changes worry underwriters.

Mistake #4: Downplaying Compliance If you take your medication daily without fail, say that explicitly. Compliance is huge for underwriters.

Mistake #5: Applying Too Soon After Diagnosis If you were just diagnosed with high cholesterol last month and just started medication, wait 3-6 months to show initial response and stability.

Real Stories: Seniors With High Cholesterol Who Got Approved

Nothing explains the process better than real stories. Here are actual seniors with high cholesterol who successfully got coverage (names changed for privacy).

Linda’s Story – Mild Cholesterol, Perfect Outcome

Background: Linda, 68, was diagnosed with high cholesterol 15 years ago. Her current levels are total cholesterol 222, LDL 145, HDL 58. She takes 10mg Lipitor once daily and has been stable at these levels for over a decade. No other health conditions. Never had any cardiac events.

What She Did:

- Decided her cholesterol was well-controlled enough for simplified issue

- Got quotes from AARP, Mutual of Omaha, and Globe Life

- Chose AARP for group rates ($15,000 coverage)

- Mentioned her 15 years of stability and good HDL

- Provided recent lipid panel showing all numbers

The Outcome: Approved in 36 hours at standard rates with zero increase. Pays $88/month for $15,000 coverage—same rate as if she had no cholesterol issues. Linda said, “I was worried they’d penalize me, but the underwriter told me my numbers are excellent for my age and my stability is exactly what they like to see. I was shocked there was no rate increase at all.”

Lesson: Well-controlled cholesterol for many years is almost invisible to underwriters. Stability matters enormously.

Robert’s Story – Moderate Cholesterol, Fair Rating

Background: Robert, 73, has total cholesterol of 258, LDL 178, HDL 52. Takes 40mg Lipitor daily. His cholesterol was in the 280s when diagnosed 8 years ago, so he’s improved with treatment. Also has well-controlled high blood pressure. No cardiac events.

What He Did:

- Applied to Mutual of Omaha (good with multiple conditions)

- Got quote for both simplified and guaranteed issue

- Mentioned his cholesterol reduction from 280s to 250s

- Provided documentation of medication compliance

- Noted his blood pressure is well-controlled on single med

The Outcome: Approved for simplified issue with 25% table rating (covering both cholesterol and blood pressure). Pays $175/month for $20,000 coverage. Without any conditions, he would have paid about $135/month, so the increase was $40/month total. Robert said, “I expected worse honestly. The agent explained that my improvement over the years helped a lot, and having both conditions well-controlled kept the rating reasonable.”

Lesson: Multiple conditions do stack, but good control and positive trends help minimize the impact. $40/month increase for two conditions is quite reasonable.

Margaret’s Story – High Cholesterol, Determined Approval

Background: Margaret, 76, has struggled with high cholesterol her entire adult life. Current levels: total cholesterol 295, LDL 215, HDL 48, triglycerides 380. Takes high-dose Crestor and Zetia. No cardiac events (which surprised her doctors given her numbers). Cholesterol has been in this range for 20 years despite various medication attempts.

What She Did:

- Initially applied to AARP—declined due to high numbers

- Applied to AIG on recommendation from independent agent

- Provided extensive medical history showing no cardiac events

- Emphasized 20 years of stability despite high numbers

- Included cardiologist letter noting her cardiovascular system is surprisingly healthy

The Outcome: AIG approved her for simplified issue with 45% table rating. Pays $258/month for $20,000 coverage. She also got a guaranteed issue quote of $240/month with 2-year waiting period. She chose simplified issue for immediate full coverage despite slightly higher cost. Margaret said, “I fully expected to need guaranteed issue. When AIG approved me, I couldn’t believe it. The underwriter told me my 20-year stability without cardiac events was remarkable and showed I’m not progressing toward heart disease like they’d normally expect.”

Lesson: Very high cholesterol can still get simplified issue approval if you can show you’re stable and haven’t developed cardiac complications. Companies evaluate the whole picture.

Thomas’s Story – High Cholesterol Plus Diabetes

Background: Thomas, 71, has total cholesterol of 275, LDL 195, HDL 45, plus type 2 diabetes (A1C 7.5). Takes statin, diabetes medication, and low-dose aspirin. Both conditions reasonably controlled. No cardiac events.

What He Did:

- Applied to AIG (specializes in multiple conditions)

- Was upfront about both diagnoses

- Emphasized that both are stable and controlled

- Provided recent lab work for both conditions

- Mentioned he sees his doctors regularly

The Outcome: Approved with 50% table rating (compound rating for both conditions). Pays $218/month for $15,000 coverage. Thomas said, “The agent explained that cholesterol alone might be 25% and diabetes another 25%, and together they’re about 50%. I understand the math. I also got a guaranteed issue quote for $188/month, but I wanted immediate coverage without a waiting period, so I accepted the simplified issue rate.”

Lesson: Multiple conditions compound each other’s impact, but approval is still very possible. Sometimes guaranteed issue is actually cheaper—always compare both.

Dorothy’s Story – Cholesterol Improving, Great Result

Background: Dorothy, 69, was recently diagnosed with high cholesterol during a routine physical. Initial reading: total 295, LDL 225. Immediately started Lipitor 40mg and made diet changes. Six months later: total 235, LDL 155. Still working on getting it lower.

What She Did:

- Waited 6 months after starting treatment to show response

- Applied to Mutual of Omaha

- Emphasized 60-point drop in total cholesterol

- Provided both initial and recent lipid panels showing improvement

- Mentioned lifestyle changes along with medication

The Outcome: Approved at standard rates with zero increase. The underwriter was impressed by her proactive response and significant improvement. Pays $85/month for $15,000 coverage. Dorothy said, “My agent suggested I wait six months to show the medication was working before applying. Best advice ever. The underwriter literally wrote in my approval letter that my rapid improvement demonstrated excellent health management.”

Lesson: If you’ve recently been diagnosed, waiting a few months to show treatment response can dramatically improve your approval and rates. Improving trends are golden.

Frank’s Story – When Guaranteed Issue Is The Answer

Background: Frank, 78, has total cholesterol over 320, prior heart attack 4 years ago, stent placement, multiple medications. Complicated medical history.

What He Did:

- Didn’t waste time with simplified issue

- Went straight to guaranteed issue at Foresters

- Applied online in 10 minutes

- Got instant approval

The Outcome: Approved instantly for $12,000 coverage at $248/month. Has 2-year waiting period but full coverage after that. Frank said, “I knew my situation was too complicated for regular approval. Guaranteed issue means I don’t get questioned about anything, and my wife will have funeral money. The waiting period is fine—I’m not planning on going anywhere in the next two years anyway.”

Lesson: Sometimes the simplest path is the best path. If your situation is complicated, guaranteed issue eliminates all the stress and questioning.

Frequently Asked Questions

Can you get life insurance if you have high cholesterol?

Yes, absolutely. Life insurance for seniors with high cholesterol is very common and usually quite straightforward to obtain. Nearly 94 million American adults have high cholesterol, and insurance companies have extensive experience underwriting this condition.

Seniors with mild to moderate high cholesterol (total cholesterol 200-270) who are on medication and have no cardiac history typically get approved for simplified issue life insurance with little to no rate increase.

Even seniors with cholesterol levels in the 280-300 range can often get approved, though with higher table ratings (20-50% premium increases).

The key factors insurance companies evaluate are: how well your cholesterol is controlled with medication, your HDL (“good”) cholesterol level, your cholesterol trend over time (improving, stable, or worsening), your LDL and triglyceride levels, whether you’ve had any cardiac events (heart attack, stroke, stents), and your compliance with prescribed treatment.

Being on a statin medication actually helps your approval because it shows you’re actively managing your health. Even seniors with very high cholesterol (300+) or those who’ve had cardiac events can get guaranteed issue life insurance, which accepts everyone regardless of health with no questions asked.

The bottom line: high cholesterol alone almost never disqualifies you from getting life insurance—it just affects your rates and which policy type works best for your situation.

Does high cholesterol affect life insurance rates?

Yes, high cholesterol does affect life insurance rates, but the impact varies significantly based on your specific cholesterol levels and overall health profile. Mild cholesterol elevation (200-240 total cholesterol) typically adds only 0-15% to your premiums, often resulting in just $5-20 extra per month.

For example, a 70-year-old male who would pay $105/month might pay $110-120/month with mild controlled cholesterol. Moderate cholesterol (240-280) usually adds 15-30% to premiums, potentially $20-45/month extra depending on age and coverage. High cholesterol (280-320) can add 30-50% or more to rates.

Very high cholesterol (320+) or cholesterol combined with cardiac events may result in 50-100%+ rate increases or require guaranteed issue insurance, which has set rates regardless of health.

However, several factors can minimize rate impact: high HDL cholesterol (60+ mg/dL) can offset elevated total cholesterol and improve ratings, showing improvement from previous higher levels demonstrates good management, long-term stability (3+ years at current levels) is viewed favorably, being on appropriate statin medication shows proactive health management, and having good cholesterol ratios (total/HDL under 5.0) helps ratings.

Importantly, controlled cholesterol on medication often gets better rates than untreated cholesterol at the same level because treatment reduces actual cardiac risk.

The rate impact also depends on other health conditions—cholesterol plus diabetes plus high blood pressure results in compound ratings where each condition amplifies the others.

What cholesterol level is too high for life insurance?

There is no absolute cholesterol level that automatically disqualifies you from getting life insurance, but approval type and rates change significantly at different levels.

For simplified issue life insurance (no medical exam, just health questions): total cholesterol under 240 is generally approved with minimal rate impact (0-15% increase), 240-280 is commonly approved with moderate table ratings (15-30% increase), 280-320 may be approved at cholesterol-friendly companies like AIG or Mutual of Omaha with higher ratings (30-50% increase), and over 320 is often declined for simplified issue, though not always—especially if HDL is high, there’s been significant improvement from previous levels, no cardiac events have occurred, or you’re on appropriate treatment with good compliance.

For guaranteed issue life insurance: there is no “too high” level—you can have cholesterol of 400+ and still get approved instantly with no health questions asked, rates are the same regardless of cholesterol level, and acceptance is guaranteed for everyone.

The key insight is that insurance companies don’t just look at total cholesterol—they evaluate your complete lipid profile including LDL (“bad”) cholesterol (over 190 is major concern), HDL (“good”) cholesterol (over 60 helps offset high total), triglycerides (over 500 is serious red flag), and cholesterol ratio (total/HDL over 6.0 is concerning).

Additionally, cholesterol with complications changes everything—high cholesterol with prior heart attack or stroke usually requires guaranteed issue, while high cholesterol with no cardiac events may still qualify for simplified issue.

The practical reality is that most seniors with cholesterol under 300 and no cardiac complications can get simplified issue approved, while those with cholesterol over 300 or with cardiac history should plan for guaranteed issue.

Should I wait to apply until my cholesterol improves?

The decision to wait depends on your specific situation. Wait 3-6 months if: you were just diagnosed and just started medication (shows treatment response improves approval), your cholesterol recently spiked and you’re addressing it (wait for it to stabilize), you recently had medication dosage increased (wait to show new dose is working), or you’re making significant lifestyle changes that might lower levels (diet, exercise).

Apply now if: your cholesterol has been stable for 6+ months or more (stability is what underwriters want), you’re already on appropriate medication and compliant (treatment compliance is viewed positively), you’re in your 70s or 80s (every year of aging increases rates 8-12%), you need coverage soon for estate planning or family needs, or your cholesterol is unlikely to improve significantly (some genetic high cholesterol doesn’t respond much to treatment).

The strategy that often works best is to apply for simplified issue now while also getting a guaranteed issue quote—if simplified issue approves you with reasonable rates, great. If they decline or rates are too high, switch to guaranteed issue immediately. You can always reapply later if your cholesterol improves significantly (dropped 50+ points and stable for a year).

Important consideration: delaying from age 70 to 71 increases your base premium by 8-12% even if cholesterol improves—sometimes it’s better to lock in coverage now even with a table rating than to wait and face higher age-based rates later.

Exception: if you were just hospitalized for a cardiac event, definitely wait 3-6 months before applying for simplified issue or go with guaranteed issue for immediate coverage.

Is life insurance more expensive if you take statins?

No, this is a common misconception. Taking statins typically does not increase your life insurance rates and often actually helps your approval compared to having untreated high cholesterol.

Here’s why: insurance underwriters view statin use positively because statins reduce your actual cardiac risk by 25-30% for heart attacks and 20-25% for strokes, being on appropriate medication shows compliance and proactive health management, and treated cholesterol is considered lower risk than untreated cholesterol at the same level.

In practical terms: a senior with cholesterol of 240 taking Lipitor will typically get better rates than a senior with cholesterol of 230 who refuses treatment because the treated person is actively reducing cardiac risk while the untreated person is ignoring a known problem.

The type of statin provides underwriting signals—low-dose single statin (Lipitor 10-20mg, Crestor 5-10mg) suggests well-controlled cholesterol with standard treatment (minimal rate impact), moderate-dose statin (Lipitor 40mg, Crestor 20mg) suggests moderate cholesterol requiring higher doses but responding well, and high-dose or multiple medications (maximum statin + Zetia + PCSK9 inhibitors) suggests severe cholesterol requiring aggressive treatment (higher rate impact, but still shows compliance).

What affects rates is your cholesterol level and overall cardiac risk, not whether you take medication for it. In fact, refusing recommended statin therapy when cholesterol is elevated (220+) is viewed as a red flag suggesting non-compliance or health denial.

The bottom line: don’t avoid statins because you’re worried about life insurance—taking prescribed statins improves both your health outcomes and your life insurance approval odds.

Can I get life insurance with cholesterol over 300?

Yes, you can definitely get life insurance with cholesterol over 300, though your options and rates depend on your overall health picture.

For simplified issue (no medical exam, health questions only): approval is possible at cholesterol-friendly companies like AIG or Mutual of Omaha if you’re on appropriate treatment showing compliance, have no recent cardiac events (heart attack, stroke, stents), have relatively good HDL cholesterol (50+), show stability at this level (not recently spiking), and can demonstrate your cardiovascular system is otherwise healthy. If approved, expect significant table ratings of 40-75% premium increase.

Many seniors with cholesterol in the 300-320 range get approved this way. For guaranteed issue (no health questions): you are automatically approved regardless of cholesterol level—could be 350, 400, even higher, same rates as everyone else your age and gender, instant approval with no underwriting, and 2-3 year waiting period for natural death (accidental death covered immediately).

Success factors that help with very high cholesterol: long-term stability (cholesterol been around 300 for years without cardiac events), good HDL (65+ shows some protective factor), aggressive treatment (shows you’re taking it seriously), no smoking (smoking + high cholesterol = major compounding risk), and good glucose/blood pressure (other risk factors controlled). Real example:

I’ve worked with seniors who have cholesterol of 310-320 who got approved for simplified issue because they’d been stable at that level for 15+ years without any heart problems—their body just runs high cholesterol but hasn’t translated to cardiac disease. The practical approach is to try simplified issue first at AIG or Mutual of Omaha—if approved, great.

If declined or rates are prohibitive (70%+ increase), switch to guaranteed issue where you’ll definitely get covered and sometimes pay less than simplified with heavy ratings.

Do I need to tell the insurance company about my cholesterol?

Yes, you absolutely must disclose your high cholesterol honestly on any life insurance application that asks health questions—this is legally and ethically required.

For simplified issue applications: you’ll be directly asked about cholesterol diagnosis, levels, medications, and related conditions.

You must answer truthfully with specific numbers, dates, and medication details. Insurance companies verify your information through the Medical Information Bureau (MIB), prescription databases (they know what medications you’ve filled), and medical records requests from your doctors. For guaranteed issue applications: no health questions are asked at all, so there’s nothing to disclose—you’re approved regardless of cholesterol.

The consequences of non-disclosure or lying are severe: during the first two years (contestability period), the company can deny claims entirely if they discover undisclosed cholesterol—your family receives only premiums paid back, not the death benefit. After two years, it’s harder to deny but possible if fraud is proven.

Even if the claim is eventually paid, the benefit might be reduced to what your premiums should have purchased with honest disclosure.

The legal and ethical imperative is clear: insurers are entitled to accurate health information to properly assess risk and price coverage, and non-disclosure is considered insurance fraud regardless of intent.

The practical reality is that rate differences for cholesterol are manageable—typically 10-30% premium increase for moderate cholesterol, which is $10-40/month for most seniors. Risking your family receiving nothing (or facing legal issues) to save $20-30/month makes no financial or ethical sense.

The smart approach is to disclose everything honestly on simplified issue applications and choose guaranteed issue if you’re uncomfortable with health questions—guaranteed issue asks nothing about cholesterol so there’s no disclosure issue.

What if I have high cholesterol and diabetes?

Having both high cholesterol and diabetes together is quite common in seniors, and life insurance is definitely still available, though rates will reflect both conditions.

How underwriters evaluate this combination: each condition receives its own rating impact—cholesterol might add 15-25% and diabetes might add 20-35%, the ratings compound somewhat but not fully additively—you might face 40-60% combined increase rather than adding directly to 35-60%, well-controlled versions of both conditions get much better treatment than poorly controlled, and stability in both conditions over time helps minimize rate impact.

Your approval path depends on control levels—if both are well-controlled (cholesterol 200-260 with medication, A1C under 7.5, no complications from either): try simplified issue at AIG, Mutual of Omaha, or companies specializing in multiple conditions, expect moderate to high table ratings (30-60% increase), and approval odds are good with right company.

If one or both are poorly controlled (cholesterol 280+, A1C over 8.5, complications): simplified issue may decline, guaranteed issue is reliable option that accepts both conditions without questions, and rates are set regardless of how controlled conditions are.

Strategy for best outcomes: optimize both conditions before applying if possible (wait for A1C to come down, show cholesterol improvement), apply to companies experienced with multiple conditions (AIG specializes in this), provide complete medical documentation showing compliance and stability, emphasize any positive factors (good HDL, weight loss, exercise), and get quotes from both simplified and guaranteed issue to compare.

Real-world examples: I’ve seen seniors with both conditions get approved for simplified issue with 35-50% ratings when both are reasonably controlled—paying $185-220/month vs. $135 without conditions for $15K coverage.

Guaranteed issue alternative at same age might be $180-200/month with waiting period—sometimes actually cheaper than simplified with heavy ratings.

Should I try simplified issue or go straight to guaranteed?

The decision between simplified issue and guaranteed issue depends on your cholesterol level, overall health, and priorities.

Try simplified issue first if: total cholesterol is under 280, you’re on medication and showing compliance, you haven’t had cardiac events (heart attack, stroke), other health conditions are well-controlled or absent, you want to avoid waiting periods (simplified covers from day one), and you’re comfortable answering health questions honestly.

Simplified issue offers 30-50% lower premiums than guaranteed when approved, no waiting period for full coverage, and larger coverage amounts available (up to $100,000+).

Go straight to guaranteed issue if: cholesterol is over 320, you’ve had recent cardiac events (past 2-3 years), you have multiple complicated health conditions, you’ve been declined by simplified issue companies before, you want absolute certainty of approval with zero health questions, or you value simplicity and instant approval over potential rate savings.

Guaranteed issue provides 100% approval certainty regardless of cholesterol level or health, no questions about medications or medical history, instant online approval in minutes, and sometimes actually cheaper than simplified with heavy table ratings.

The hybrid strategy that works best for many: get quotes from both types simultaneously, apply for simplified issue first (takes 24-48 hours for decision), if simplified approves with reasonable rates (under 40% increase), take it for better pricing and no waiting period.

If simplified declines or rates are 50%+ higher, switch immediately to guaranteed issue. You lose nothing by trying simplified first except maybe 2-3 days of time.

Important: never cancel existing coverage until new coverage is approved and active—always overlap policies briefly to ensure continuous coverage.

How often can I reapply if my cholesterol improves?

You can reapply for life insurance as often as you want when circumstances change, though strategic timing matters for best results.

Consider reapplying when: your cholesterol has dropped 50+ points and been stable at the lower level for 6-12 months (significant improvement), you’ve reduced medications (from multiple to single, or from high-dose to low-dose shows improvement), you had guaranteed issue but now might qualify for simplified issue (could save 30-50% on premiums), it’s been 3-5 years since original application and cholesterol remains stable (age-based rates have increased but improved cholesterol rating might offset), or you originally had table rating but recent tests show excellent control.

The reapplication strategy is to apply for new policy while keeping existing coverage active—only cancel old policy after new one is approved and in force.

Never cancel existing coverage before getting approved for new coverage—you might be declined or get worse rates than expected. Set realistic expectations for improvement: cholesterol dropping from 290 to 240 could reduce rating from 40% to 15% (significant savings), but dropping from 240 to 220 may not change rating much (both in same risk category).

Calculate whether savings justify effort: if reapplying could save $30-50/month ($360-600/year), it’s worth the effort. If savings would only be $10/month, probably not worth it unless you’re also pursuing this for increased coverage.

Typical scenarios where reapplication makes sense: you originally got guaranteed issue at age 70 ($180/month), cholesterol dropped significantly, now age 73 but could get simplified issue at $150/month despite being older—saves $30/month despite aging.

Or you got simplified with 40% table rating ($200/month), cholesterol improved dramatically, reapply gets 15% rating ($165/month)—saves $35/month.

Most impactful reapplication is when moving from guaranteed issue to simplified issue—often saves 30-50% even accounting for aging a few years.

Taking Action: Your Next Steps

You’ve learned everything about life insurance for seniors with high cholesterol. Now let’s create your action plan to actually get covered.

This Week:

Day 1-2: Get Your Numbers

- Request your most recent lipid panel from your doctor

- Write down total cholesterol, LDL, HDL, triglycerides

- Calculate your cholesterol ratio (total ÷ HDL)

- Note the date of the test

Day 3-4: Gather Medical Information

- List all cholesterol medications with dosages

- Note how long you’ve been on each medication

- Document any medication changes in past 2 years

- List any cardiac events or procedures (if any)

- Note other health conditions you have

Day 5-6: Get Multiple Quotes

- Contact 3-5 companies (or one independent agent)

- Request quotes for simplified issue

- Also get guaranteed issue quote for comparison

- Ask specifically about cholesterol underwriting at each company

- Get written quotes you can compare

Day 7: Apply

- Choose the company with best combination of rate and rating

- Complete application honestly and thoroughly

- Emphasize positive factors (stability, improvement, compliance)

- Provide recent lipid panel results

- Be specific with all answers

This Month:

Week 2: Underwriting Period

- Respond immediately to any company requests

- Provide additional documentation promptly

- Stay in contact with agent or company representative

- Follow up if you haven’t heard back within 5 business days

Week 3: Review Approval

- If approved: Review rate, coverage, table rating

- If declined: Apply immediately for guaranteed issue

- If rates are high: Compare to guaranteed issue quote

- Calculate total annual cost for decision-making

Week 4: Activate Coverage

- Pay first premium to activate policy

- Set up automatic payments (never miss one!)

- File policy documents safely

- Inform beneficiaries about coverage

- Note your free look period (30 days to review)

Long-Term:

Every Year:

- Verify premium payments processing correctly

- Get annual lipid panel to track cholesterol

- Review beneficiary designations

- Consider reapplying if cholesterol improves 50+ points

After Major Changes:

- If cholesterol drops significantly, consider reapplying

- After 3-5 years of stability, rates might improve

- If you discontinue medications (cholesterol normalized), reapply

Don’t Procrastinate

Every month you delay:

- Base rates increase with age (8-12% annually)

- Your health could change

- You remain without protection for your family

The best time to apply was last year. The second-best time is this week.

Final Thoughts

Getting life insurance for seniors with high cholesterol is not only possible—it’s often quite straightforward and affordable. Your high cholesterol doesn’t define you or disqualify you.

What I want you to take away from this guide:

Your cholesterol is manageable. Unless your numbers are extremely high (320+) with cardiac complications, most companies will approve you at reasonable rates.

Being on a statin helps, not hurts. Taking prescribed medication shows you’re managing your health proactively. Don’t avoid treatment because you’re worried about insurance.

Stability and trends matter most. Cholesterol that’s been at 250 for 10 years looks better than cholesterol bouncing between 200 and 280. Improving numbers look great.

You have real options. Simplified issue for many, guaranteed issue for everyone. Nobody is truly uninsurable.

Shopping saves significant money. The difference between companies can be $40-70/month for the same coverage—that’s $480-840 per year.

Honesty is essential. Disclose your cholesterol completely. The rate difference is manageable, but claim denial is devastating to your family.

I’ve helped hundreds of seniors with high cholesterol get approved over the years. Some had cholesterol barely above 200 and got standard rates. Others had cholesterol over 300 and needed guaranteed issue but still got covered. What they all had in common was taking action.

Your cholesterol is a number. It’s manageable, it’s treatable, and it doesn’t prevent you from protecting your family.

Take the first step this week. Get those quotes. Complete that application. Give yourself and your family the peace of mind that comes with knowing everything is handled.

They’ll thank you for it.

Disclaimer: This article provides general educational information about life insurance for seniors with high cholesterol and should not be considered medical, insurance, or financial advice. Insurance products, underwriting guidelines, rates, and availability vary significantly by company, state, individual health status, and specific circumstances. Premium rates quoted are approximate ranges for illustration purposes and may not reflect actual rates available to you. Cholesterol level classifications and underwriting criteria vary between insurance companies. Always provide complete, honest information on all insurance applications. Consult with your physician regarding cholesterol management and medication decisions, and work with licensed insurance professionals for personalized guidance about your specific situation. This guide is not affiliated with or endorsed by any insurance company or medical provider mentioned. Information is current as of publication date but insurance and medical guidelines change frequently. Individual results will vary based on personal health history, cholesterol levels, medications, and other factors.