Average Life Insurance Rates by Age (50, 55, 60, 65, 70) – 2026 Data

Posted in Senior Life Insurance on December 26, 2025 last updated on December 26, 2025

Posted in Senior Life Insurance on December 26, 2025 last updated on December 26, 2025

Understanding life insurance rates by age is crucial for making informed decisions about your coverage. The difference between buying at 50 versus waiting until 65 can mean thousands of dollars in savings—or costs—over your lifetime.

In this comprehensive guide, we’ve compiled the most current 2026 life insurance rates by age for seniors aged 50 to 70. You’ll see exactly what you can expect to pay for both term and whole life insurance at each age, plus the factors that affect your rates and strategies to get the best prices.

In This Guide:

- Average life insurance rates by age (50, 55, 60, 65, 70)

- Term life insurance rates by age

- Whole life insurance rates by age

- Factors that affect your rates

- Types of life insurance available

- How to get the best rates at any age

- Frequently asked questions

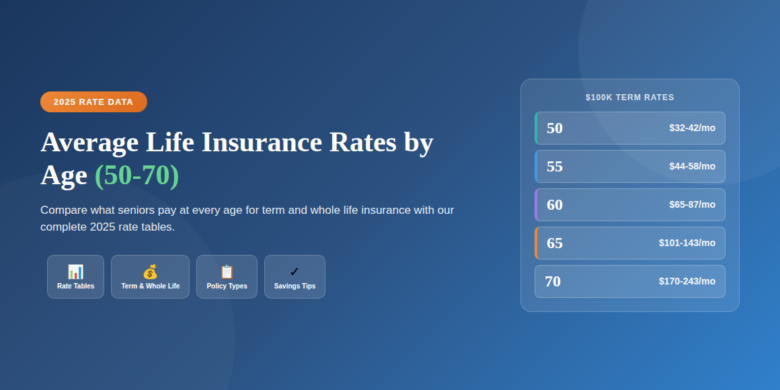

The Quick Answer: Life Insurance Rates by Age

Here’s a snapshot of what seniors pay for life insurance at each age. These are average monthly rates for healthy, non-smoking individuals. Term life vs whole life will be the most crucial part to your life insurance buying experience.

Term Life Insurance: $100,000 Coverage (10-Year Term)

| Age | Male Monthly | Female Monthly | Annual Cost |

|---|---|---|---|

| 50 | $42 | $32 | $384 – $504 |

| 55 | $58 | $44 | $528 – $696 |

| 60 | $87 | $65 | $780 – $1,044 |

| 65 | $143 | $101 | $1,212 – $1,716 |

| 70 | $243 | $170 | $2,040 – $2,916 |

Whole Life Insurance: $25,000 Coverage

| Age | Male Monthly | Female Monthly | Annual Cost |

|---|---|---|---|

| 50 | $89 | $72 | $864 – $1,068 |

| 55 | $108 | $89 | $1,068 – $1,296 |

| 60 | $138 | $115 | $1,380 – $1,656 |

| 65 | $178 | $148 | $1,776 – $2,136 |

| 70 | $238 | $198 | $2,376 – $2,856 |

Key Insight: Life insurance premiums increase approximately 8-12% for every year you delay purchasing. A 50-year-old pays roughly half what a 70-year-old pays for the same coverage.

How Age Affects Life Insurance Rates

Age is the single biggest factor determining your life insurance premiums. Here’s why—and how much it matters.

The Age Factor Explained

Insurance companies base premiums on mortality risk—the statistical likelihood you’ll die during the coverage period. As you age:

- Your mortality risk increases

- You’re more likely to develop health conditions

- The insurance company has less time to collect premiums before a potential claim

This translates directly into higher premiums at older ages.

The Cost of Waiting: Real Numbers

Let’s look at how much waiting costs you for a $100,000, 10-year term policy:

| If You’re… | And You Wait Until… | You’ll Pay Extra… | Total Extra Cost |

|---|---|---|---|

| 50 | 55 | $16/month more | $1,920 over 10 years |

| 55 | 60 | $29/month more | $3,480 over 10 years |

| 60 | 65 | $56/month more | $6,720 over 10 years |

| 50 | 65 | $101/month more | $12,120 over 10 years |

Bottom Line: A 50-year-old male who waits until 65 to buy will pay over $12,000 more for the same coverage. Every year you wait costs you money.

Age Rate Increase by Percentage

| Age Transition | Average Premium Increase |

|---|---|

| 50 to 55 | 38% higher |

| 55 to 60 | 50% higher |

| 60 to 65 | 64% higher |

| 65 to 70 | 70% higher |

| 50 to 70 | 478% higher (nearly 5x) |

Term Life Insurance Rates by Age: Complete 2025 Tables

Term life insurance provides coverage for a specific period (10, 15, 20, or 30 years). It’s the most affordable option for seniors who need maximum coverage.

10-Year Term Life Insurance Rates

$100,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $42 | $32 | $504 | $384 |

| 55 | $58 | $44 | $696 | $528 |

| 60 | $87 | $65 | $1,044 | $780 |

| 65 | $143 | $101 | $1,716 | $1,212 |

| 70 | $243 | $170 | $2,916 | $2,040 |

$250,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $78 | $58 | $936 | $696 |

| 55 | $115 | $85 | $1,380 | $1,020 |

| 60 | $185 | $138 | $2,220 | $1,656 |

| 65 | $315 | $225 | $3,780 | $2,700 |

| 70 | $565 | $398 | $6,780 | $4,776 |

$500,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $145 | $108 | $1,740 | $1,296 |

| 55 | $218 | $162 | $2,616 | $1,944 |

| 60 | $358 | $265 | $4,296 | $3,180 |

| 65 | $598 | $428 | $7,176 | $5,136 |

| 70 | $1,085 | $756 | $13,020 | $9,072 |

15-Year Term Life Insurance Rates

$100,000 Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $52 | $40 |

| 55 | $75 | $56 |

| 60 | $112 | $84 |

| 65 | $188 | $135 |

Note: 15-year terms may have limited availability after age 65.

20-Year Term Life Insurance Rates

$100,000 Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $58 | $45 |

| 55 | $89 | $67 |

| 60 | $145 | $108 |

| 65 | $248 | $178 |

Note: 20-year terms are typically not available after age 65.

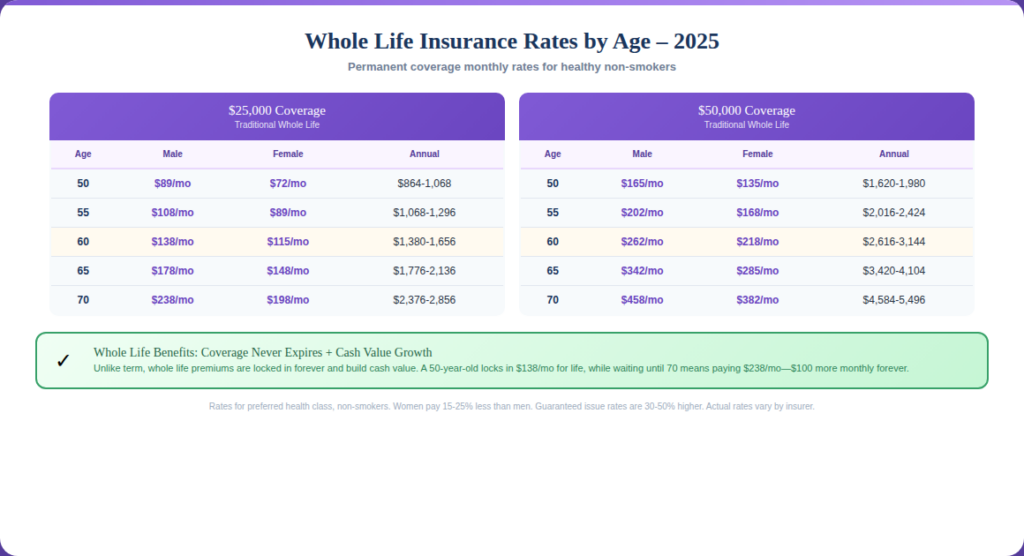

Whole Life Insurance Rates by Age: Complete 2025 Tables

Whole life insurance provides permanent coverage that never expires, with fixed premiums and cash value accumulation.

Traditional Whole Life Insurance Rates

$10,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $42 | $35 | $504 | $420 |

| 55 | $52 | $44 | $624 | $528 |

| 60 | $62 | $52 | $744 | $624 |

| 65 | $82 | $68 | $984 | $816 |

| 70 | $108 | $89 | $1,296 | $1,068 |

$25,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $89 | $72 | $1,068 | $864 |

| 55 | $108 | $89 | $1,296 | $1,068 |

| 60 | $138 | $115 | $1,656 | $1,380 |

| 65 | $178 | $148 | $2,136 | $1,776 |

| 70 | $238 | $198 | $2,856 | $2,376 |

$50,000 Coverage

| Age | Male Monthly | Female Monthly | Male Annual | Female Annual |

|---|---|---|---|---|

| 50 | $165 | $135 | $1,980 | $1,620 |

| 55 | $202 | $168 | $2,424 | $2,016 |

| 60 | $262 | $218 | $3,144 | $2,616 |

| 65 | $342 | $285 | $4,104 | $3,420 |

| 70 | $458 | $382 | $5,496 | $4,584 |

$100,000 Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $318 | $258 |

| 55 | $392 | $325 |

| 60 | $498 | $415 |

| 65 | $658 | $548 |

| 70 | $885 | $738 |

Final Expense / Burial Insurance Rates

Final expense insurance is a type of whole life specifically designed for funeral and burial costs, with coverage typically ranging from $5,000 to $25,000.

$10,000 Final Expense Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $38 | $32 |

| 55 | $48 | $40 |

| 60 | $62 | $52 |

| 65 | $82 | $68 |

| 70 | $108 | $89 |

$20,000 Final Expense Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $68 | $56 |

| 55 | $88 | $72 |

| 60 | $115 | $96 |

| 65 | $152 | $126 |

| 70 | $198 | $165 |

Guaranteed Issue Whole Life Rates (No Health Questions)

Guaranteed issue policies accept everyone regardless of health conditions. Rates are higher due to the increased risk.

$10,000 Guaranteed Issue Coverage

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $52 | $44 |

| 55 | $68 | $56 |

| 60 | $89 | $72 |

| 65 | $115 | $95 |

| 70 | $148 | $122 |

Note: Guaranteed issue policies have a 2-3 year graded benefit period for natural death.

Term vs Whole Life: Cost Comparison by Age

Understanding the cost difference between term and whole life helps you choose the right coverage.

$100,000 Coverage: Term vs Whole Life Monthly Rates

| Age | 10-Year Term (Male) | Whole Life (Male) | Difference |

|---|---|---|---|

| 50 | $42 | $318 | Whole life costs 7.6x more |

| 55 | $58 | $392 | Whole life costs 6.8x more |

| 60 | $87 | $498 | Whole life costs 5.7x more |

| 65 | $143 | $658 | Whole life costs 4.6x more |

| 70 | $243 | $885 | Whole life costs 3.6x more |

Key Insight: Term life is significantly cheaper, but it expires. Whole life costs more but provides permanent coverage. Many seniors benefit from combining both.

Total Cost Over Time: 60-Year-Old Male, $100,000 Coverage

10-Year Term:

- Monthly: $87

- Total over 10 years: $10,440

- Coverage ends at age 70

Whole Life:

- Monthly: $498

- Total over 10 years: $59,760

- Coverage continues for life

- Builds cash value

Hybrid Approach (Recommended):

- $75,000 10-year term: $68/month

- $25,000 whole life: $138/month

- Total: $206/month

- Coverage: $100,000 now, $25,000 permanent

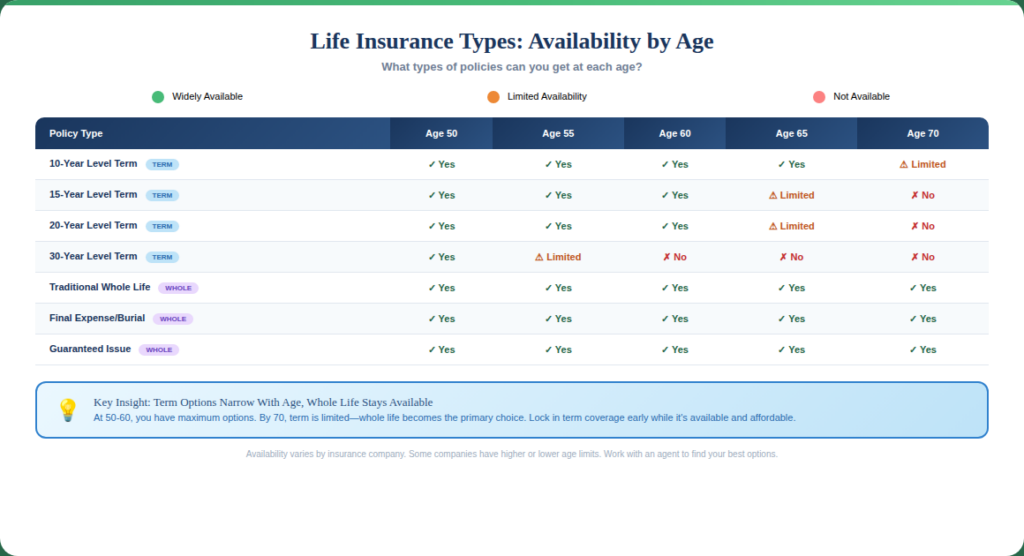

Types of Life Insurance Available by Age

Different ages have access to different types of policies. Here’s what’s available at each age.

Term Life Insurance Types

1. Level Term Life Insurance (Most Popular)

- What it is: Fixed premium and death benefit for 10-30 years

- Availability by age:

- Age 50: 10, 15, 20, 25, 30-year terms

- Age 55: 10, 15, 20, 25-year terms

- Age 60: 10, 15, 20-year terms

- Age 65: 10, 15-year terms (20-year limited)

- Age 70: 10-year term only (limited)

- Best for: Maximum coverage at lowest cost

2. Annual Renewable Term (ART)

- What it is: One-year term that renews annually; premiums increase each year

- Availability: All ages up to 80+

- Best for: Short-term needs, uncertain coverage duration

3. Decreasing Term Life Insurance

- What it is: Death benefit decreases over time; premium stays level

- Availability: Ages 50-70

- Best for: Mortgage protection (matches declining loan balance)

- Cost: 20-40% less than level term

4. Return of Premium (ROP) Term

- What it is: Get all premiums back if you outlive the term

- Availability: Ages 50-60 (limited after 60)

- Best for: Those who don’t want to “lose” money if they survive

- Cost: 2-4x higher than regular term

Whole Life Insurance Types

1. Traditional Whole Life

- What it is: Permanent coverage with fixed premiums, guaranteed death benefit, cash value growth

- Availability: All ages up to 85

- Best for: Guaranteed lifetime coverage, estate planning, inheritance

2. Guaranteed Universal Life (GUL)

- What it is: Permanent coverage with lower premiums than traditional whole life, minimal cash value

- Availability: Ages 50-80

- Best for: Affordable permanent coverage without needing cash value

- Cost: 20-30% less than traditional whole life

3. Final Expense / Burial Insurance

- What it is: Small whole life policies ($5,000-$25,000) for funeral costs

- Availability: Ages 50-85

- Best for: Covering funeral and burial expenses

- Cost: Affordable monthly payments ($30-$150 typically)

4. Guaranteed Issue Whole Life

- What it is: No health questions, everyone accepted

- Availability: Ages 50-85

- Best for: Seniors with serious health conditions

- Cost: 30-50% higher than simplified issue

- Note: 2-3 year graded benefit waiting period

Factors That Affect Your Life Insurance Rates

While age is the primary factor, several other elements impact your premiums.

1. Gender

Women consistently pay less than men for life insurance because they statistically live longer.

Average Gender Difference:

- Women pay 20-30% less than men for term life

- Women pay 15-25% less than men for whole life

Example at Age 60 ($100,000 10-year term):

- Male: $87/month

- Female: $65/month

- Savings for women: $22/month ($264/year)

2. Health Status

Your health significantly impacts your rate classification:

| Health Class | Description | Rate Impact |

|---|---|---|

| Preferred Plus | Excellent health, no conditions, ideal weight | Lowest rates |

| Preferred | Very good health, minor issues only | 10-15% higher |

| Standard Plus | Good health, controlled conditions | 20-30% higher |

| Standard | Average health, some conditions | 35-50% higher |

| Substandard | Significant health issues | 50-200% higher |

Common conditions and their impact:

- High blood pressure (controlled): 10-25% increase

- Type 2 diabetes (controlled): 25-75% increase

- Heart disease history: 50-150% increase

- Cancer history (5+ years): 25-100% increase

3. Tobacco Use

Smoking is one of the biggest rate factors after age.

Smoker vs Non-Smoker Rates (Age 60, $100,000 10-year term):

- Non-smoker male: $87/month

- Smoker male: $245/month

- Smokers pay nearly 3x more

Good news: If you quit smoking for 12-24 months (varies by insurer), you can qualify for non-smoker rates.

4. Coverage Amount

More coverage costs more, but not proportionally. Buying larger amounts often provides better value per dollar of coverage.

$100,000 vs $250,000 (Age 60 Male, 10-year term):

- $100,000: $87/month ($0.87 per $1,000)

- $250,000: $185/month ($0.74 per $1,000)

- Larger coverage = better value per dollar

5. Term Length

Longer terms cost more because there’s a higher probability of death during the coverage period.

Age 55 Male, $100,000 Coverage:

- 10-year term: $58/month

- 15-year term: $75/month

- 20-year term: $89/month

6. Policy Type

Different policy types have vastly different costs:

| Policy Type | Relative Cost | Coverage Duration |

|---|---|---|

| Term Life | Lowest | Temporary (10-30 years) |

| Guaranteed Universal Life | Medium | Permanent |

| Traditional Whole Life | Highest | Permanent + Cash Value |

Life Insurance Rates by Age: Real-World Examples

Let’s see how different seniors chose their coverage based on age and budget.

Example 1: Patricia, Age 50 – Locked in Low Rates

Situation: Patricia, 50, is healthy and wants to maximize her coverage while rates are low.

Choice: $500,000 20-year term at $108/month + $25,000 whole life at $72/month Total: $180/month for $525,000 coverage

Why this works: At 50, Patricia gets excellent rates. The 20-year term covers her mortgage and income replacement until 70, while the whole life guarantees final expense coverage forever.

What waiting would cost: If Patricia waited until 60, the same term coverage would cost $265/month—an extra $185/month ($22,200 over 10 years).

Example 2: Robert, Age 55 – Balanced Approach

Situation: Robert, 55, wants $200,000 total coverage on a $200/month budget.

Choice: $175,000 15-year term at $125/month + $25,000 whole life at $75/month Total: $200/month for $200,000 coverage

Why this works: The term covers his mortgage payoff timeline (14 years remaining), while whole life ensures his funeral costs are covered regardless of when he passes.

Example 3: Margaret, Age 60 – Income Replacement Focus

Situation: Margaret, 60, wants to provide 10 years of income replacement for her husband if she passes away.

Choice: $300,000 10-year term at $162/month

Why this works: At $162/month, Margaret secures $300,000—enough to replace her income for nearly a decade. She already has a small whole life policy for final expenses.

Example 4: James, Age 65 – Permanent Coverage Priority

Situation: James, 65, has paid off his mortgage and wants permanent coverage for final expenses and to leave money for grandchildren.

Choice: $50,000 whole life at $342/month

Why this works: At 65, term insurance is expensive and expires. James prioritizes permanent coverage that builds cash value and guarantees his $50,000 death benefit regardless of when he dies.

Example 5: Dorothy, Age 70 – Final Expense Focus

Situation: Dorothy, 70, only needs coverage for funeral costs. She has limited income.

Choice: $15,000 final expense whole life at $145/month

Why this works: At 70, term insurance is very expensive and expires at 80. Dorothy chose affordable final expense coverage that locks in her rate forever and guarantees her family won’t pay for her funeral.

How to Get the Best Life Insurance Rates at Any Age

Follow these strategies to minimize your premiums.

1. Buy Now—Don’t Wait

Every year you delay increases your premiums 8-12%. If you’re considering life insurance, the best time to buy is today.

2. Improve Your Health First (If Possible)

If you can wait 3-6 months and make health improvements, you may qualify for a better rate class:

- Lose weight (BMI significantly affects rates)

- Lower blood pressure and cholesterol

- Quit smoking (12-24 months smoke-free for non-smoker rates)

- Get conditions under control with consistent medication

3. Shop Multiple Companies

Rates vary 20-40% between insurance companies for identical coverage. Always get quotes from at least 3-5 insurers.

Companies known for competitive senior rates:

- Mutual of Omaha

- AIG

- Banner Life

- Protective

- Pacific Life

4. Work With an Independent Agent

Independent agents can:

- Shop dozens of companies for you

- Find companies lenient for your specific health conditions

- Know which companies offer the best rates at your age

- Help you avoid wasting time on applications that will be declined

5. Choose the Right Coverage Amount

Don’t over-insure or under-insure. Calculate your actual needs:

- Debts (mortgage, car loans, credit cards)

- Final expenses ($15,000-$25,000)

- Income replacement (3-10 years of income)

- Legacy goals

6. Consider a Hybrid Approach

Combine term and whole life to optimize cost and coverage:

- Term: Covers large temporary needs (mortgage, income replacement)

- Whole life: Covers permanent needs (final expenses)

7. Be Honest on Your Application

Lying about health conditions can result in:

- Application denial

- Claim denial (family gets nothing)

- Being flagged in the MIB database

Insurance companies verify your information through prescription databases and medical records.

Frequently Asked Questions

What is the average cost of life insurance by age?

Average life insurance costs vary significantly by age and policy type. For a $100,000 10-year term policy for healthy non-smokers: age 50 pays approximately $32-$42/month, age 55 pays $44-$58/month, age 60 pays $65-$87/month, age 65 pays $101-$143/month, and age 70 pays $170-$243/month. Women typically pay 20-30% less than men. Whole life insurance costs 3-7 times more than term for the same coverage amount.

How much does life insurance cost for a 50-year-old?

A healthy, non-smoking 50-year-old can expect to pay approximately $32-$42/month for a $100,000 10-year term policy (women pay the lower end, men the higher). For $250,000 coverage, expect $58-$78/month. Whole life insurance for a 50 year old with $25,000 coverage costs approximately $72-$89/month. Age 50 is an excellent time to buy—rates are 40-60% lower than at age 70.

How much does life insurance cost for a 60-year-old?

A healthy, non-smoking 60-year-old typically pays $65-$87/month for a $100,000 10-year term policy. For $250,000 coverage, expect $138-$185/month. Whole life insurance for $25,000 coverage costs approximately $115-$138/month. Life insurance at 60, you still have access to 10, 15, and 20-year term options, though 20-year terms become more expensive.

How much does life insurance cost for a 70-year-old?

A healthy, non-smoking 70-year-old pays approximately $170-$243/month for a $100,000 10-year term policy. Term options become limited at 70—most companies only offer 10-year terms. For whole life insurance, expect $198-$238/month for $25,000 coverage. Many 70-year-olds find whole life or final expense insurance more practical than term at this age.

Why do life insurance rates increase with age?

Life insurance rates increase with age because mortality risk increases. As you get older, you’re statistically more likely to die during the coverage period, which means the insurance company is more likely to pay a claim. Rates typically increase 8-12% for each year of age. A 70-year-old has approximately 5 times higher mortality risk than a 50-year-old, which is why rates are roughly 5 times higher.

Is life insurance cheaper for females?

Yes, women consistently pay 20-30% less than men for life insurance. This is because women statistically live longer than men (average life expectancy is about 5 years longer), which means insurance companies are less likely to pay claims during the coverage period. For example, a 60-year-old woman might pay $65/month for coverage that costs a 60-year-old man $87/month.

What factors affect life insurance rates besides age?

Besides age, major factors affecting life insurance rates include: gender (women pay 20-30% less), health status (conditions can increase rates 25-200%), tobacco use (smokers pay 2-3x more), coverage amount (more coverage costs more but better value per dollar), term length (longer terms cost more), and policy type (term is cheapest, whole life is most expensive). Your rate classification (preferred, standard, substandard) based on these factors significantly impacts your premium.

Can I get life insurance at 70 years old?

Yes, you can definitely get life insurance at 70. Your options include: 10-year term life insurance (limited availability, higher rates), whole life insurance (widely available up to age 85), final expense/burial insurance (available up to age 85, coverage $5,000-$25,000), and guaranteed issue whole life (accepts everyone regardless of health, available to age 85). While rates are higher at 70 than at younger ages, coverage is readily available.

Is term or whole life insurance better for seniors?

Term life vs whole life depends on your needs and age. Term life is better if you need maximum coverage for a specific period (mortgage payoff, income replacement), want the lowest premiums, and are age 50-65 when term is most available. Whole life is better if you want permanent coverage that never expires, need guaranteed final expense coverage, are over 65 when term becomes expensive/limited, or want to build cash value. Many seniors benefit from combining both: term for temporary needs and whole life for permanent final expense coverage.

How can I lower my life insurance rates?

To get lower life insurance rates: buy now (rates increase 8-12% yearly), improve your health if possible (lose weight, lower BP/cholesterol, quit smoking), shop multiple companies (rates vary 20-40%), work with an independent agent who can find the best rates for your situation, choose the right coverage amount (don’t over-insure), consider a term/whole life combination, and be completely honest on your application to avoid clai

Taking the Next Step

Understanding life insurance rates by age empowers you to make the right decision for your situation. Here are the key takeaways:

For 50-55 year-olds:

- You have access to the best rates and all policy types

- Consider locking in a 20-year term while it’s affordable

- Don’t wait—every year costs you money

For 60-65 year-olds:

- Term insurance is still affordable but becoming more expensive

- 20-year terms may be limited; 10-15 year terms are best value

- Consider combining term with whole life for permanent coverage

For 70+ year-olds:

- Term options are limited and expensive

- Whole life or final expense insurance is typically the best choice

- Guaranteed issue is available if health prevents other options

Remember: The best time to buy life insurance is always now. Every year you wait costs you money in higher premiums and potentially limits your options.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Life insurance rates shown are estimates for healthy, non-smoking individuals in preferred or standard health classes and may not reflect your actual costs. Rates vary significantly based on individual factors including age, gender, health status, tobacco use, coverage amount, term length, and the specific insurance company. Always obtain personalized quotes from licensed insurance professionals. Data reflects 2025 estimates and is subject to change.