Life Insurance for Seniors over 60: Your Complete Guide

Posted in Senior Life Insurance on December 4, 2025 last updated on May 21, 2026

Posted in Senior Life Insurance on December 4, 2025 last updated on May 21, 2026

Can Seniors Over 60 Still Get Life Insurance?

Yes, many seniors over 60 can still qualify for life insurance, including term life, whole life, no medical exam, and final expense policies. Approval and rates depend on age, health conditions, medications, and the insurance company selected. Many insurers still offer affordable coverage options well into retirement years.

When my neighbor Susan turned 60 last year, she called me with a question I hear almost weekly: “I know I need life insurance, but I have no idea where to start. What’s the best option for someone my age?”

Susan isn’t alone. Turning 60 is a milestone that makes you think about the future differently. Your kids are grown, retirement is approaching (or already here), and you want to make sure your family isn’t stuck with funeral bills and final expenses when you’re gone. But the life insurance landscape feels overwhelming—dozens of companies, confusing policy types, and rates that seem to vary wildly.

Here’s what I told Susan, and what I’m going to tell you: finding the best life insurance for seniors over 60 isn’t as complicated as it seems. You don’t need perfect health. You don’t need to pass a medical exam. And you don’t need a degree in insurance to figure this out.

In fact, being in your 60s puts you in an excellent position. You’re young enough that rates are still very reasonable—much better than waiting until 70 or 75. You likely qualify for multiple policy types, giving you real choices. And insurance companies actively compete for your business with products designed specifically for your age group.

Over the past 15 years, I’ve helped thousands of seniors in their 60s find the right life insurance. I’ve seen what works, what doesn’t, and which companies consistently offer the best combination of rates, service, and approval odds. I’ve watched people save hundreds of dollars annually just by shopping properly, and I’ve seen others overpay because they went with the first company that sent them mail.

This comprehensive guide will walk you through everything you need to know about life insurance for seniors over 60: the best companies and why they’re recommended, exactly what you’ll pay at different ages (60, 62, 65, 69), which policy type fits your situation, how to apply and actually get approved, real stories from seniors just like you, and honest answers to every question you have.

Whether you’re 60 or 69, healthy or managing chronic conditions, this guide will help you make a confident, informed decision.

Let’s find your best life insurance over 60 option together.

If you are approaching 70 years old, check out our blog post about life insurance for seniors over 70

Why Life Insurance Over 60 Matters

Before we dive into companies and rates, let’s talk about why life insurance matters specifically in your 60s. You might be thinking, “I’m still young” or “I’ll get it later.” Here’s why now is actually the ideal time:

Your Rates Will Never Be Lower (Than They Are Today)

This is the hard truth about life insurance: every year you wait costs you money—permanent money.

The Age Factor:

- Age 60 to 61: 8-10% rate increase

- Age 60 to 65: 30-40% rate increase

- Age 60 to 70: 60-80% rate increase

Real Example: Mary, age 60, could get $15,000 coverage for $75/month. If she waits until 65, that same coverage costs $100/month. That’s $25/month × 12 months × 15 years = $4,500 extra over her lifetime—just for waiting 5 years.

The Health Factor: At 60, many people are still in good health. By 65 or 70, health issues emerge—diabetes, heart problems, high blood pressure. These conditions dramatically increase rates or limit you to more expensive guaranteed issue policies.

The Bottom Line: You will never be younger or healthier than you are today. Lock in your rates now.

Your 60s: The Sweet Spot for Life Insurance

Being in your 60s offers unique advantages:

Still Young Enough for Great Rates: Insurers consider your 60s “younger senior” territory. Rates are 40-60% lower than ages 70+ for identical coverage.

More Policy Options: At 60-69, you qualify for:

- Simplified issue (no medical exam, just health questions)

- Guaranteed issue (no health questions at all)

- Larger coverage amounts ($50,000-$100,000+)

- Both term and permanent options

By 75+, many of these options disappear or become prohibitively expensive.

Better Health = Better Approval: Most 60-year-olds can qualify for simplified issue policies with excellent rates. By 70+, more people need guaranteed issue (higher premiums, waiting periods).

What You’re Really Protecting

Life insurance at 60+ isn’t about replacing income for young children. It’s about dignity and consideration:

Final Expenses ($12,000-$25,000 typically):

- Funeral and burial: $8,000-$15,000

- Final medical bills: $2,000-$8,000

- Outstanding debts: credit cards, loans

- Estate settlement costs

- Probate expenses if applicable

Leaving Something Behind:

- Help grandchildren with college

- Leave a meaningful inheritance

- Pay off remaining mortgage

- Cover property taxes during transition

- Give to church or charity

Peace of Mind: Your spouse or children won’t scramble for money during grief. They won’t go into debt for your funeral. They won’t argue about who pays what.

Real Impact: After Susan (my neighbor) got covered, she said, “I sleep better knowing this is handled. My kids won’t have to stress about money while they’re mourning.”

That’s what the best life insurance for seniors over 60 provides: practical protection and emotional peace. Check out our post about how much life insurance seniors need.

Best Types of Life Insurance Available Over 60

Understanding policy types helps you choose the best fit. Here are your real options at 60+:

Term Life Insurance

Term life may still work well for healthier applicants in their early 60s who:

- need income replacement

- want mortgage protection

- need larger coverage amounts

However, premiums increase significantly with age.

Whole Life Insurance

Whole life insurance provides:

- permanent coverage

- fixed premiums

- cash value accumulation

This is often popular for estate planning and long-term protection.

No Medical Exam Life Insurance

No-exam policies may work well for:

- moderate health conditions

- faster approvals

- simplified underwriting

These policies are increasingly popular among seniors over 60.

Final Expense Insurance

Final expense policies are commonly used to:

- cover funeral costs

- pay final medical bills

- reduce financial stress on family members

These policies often require no medical exam and offer simplified approval.

| Policy Type | Best For | Medical Exam | Typical Coverage |

|---|---|---|---|

| Term Life | Healthier seniors | Sometimes | Higher |

| Whole Life | Lifetime protection | Sometimes | Moderate |

| No Medical Exam | Faster approval | No | Moderate |

| Final Expense | Funeral costs | Usually No | Smaller |

Which Should You Choose?

For seniors over 60, the answer is almost always whole life (marketed as final expense). Here’s why:

Permanent Need: You need coverage for whenever you pass—could be 70, 80, 90, or 100. Term insurance that expires doesn’t help.

Locked-In Rates: Pay $100/month at 60, still pay $100/month at 80. Premiums never increase.

Guaranteed Payout: As long as you pay premiums, your beneficiaries get paid. No “sorry, your policy expired” scenario.

Term Insurance: Term life will work for healthier seniors who need to cover bigger expenses such as mortgage, kids college tuition, etc. but remember if you’re 60 and buy 20-year term, it expires at 80—right when you’re most likely to need it.

The Bottom Line: When shopping for life insurance for seniors over 60, the majority you will want to go with permanent whole life coverage, whether it’s called “final expense,” “burial insurance,” or just “life insurance.”

Term life vs whole life comparison blog post.

Common Health Conditions for Seniors Over 60

Many seniors over 60 still qualify for life insurance even with pre-existing medical conditions.

Insurance companies frequently approve applicants with:

- diabetes

- high blood pressure

- high cholesterol

- sleep apnea

- heart disease

- arthritis

- stroke

- past cancer

- multiple health conditions

Insurance companies typically evaluate:

- condition stability

- medications

- smoking history

- overall cardiovascular health

Some insurers are significantly more flexible with chronic health conditions than others.

Best Life Insurance Companies for Seniors Over 60

Not all insurance companies are created equal for 60 year olds. Here are the best life insurance companies for seniors with honest assessments:

1. Mutual of Omaha – Best Overall Choice

Why They’re #1:

- Accept ages 45-85 (widest range)

- A+ financial rating (Superior) from A.M. Best

- 115+ years in business—rock solid

- Both simplified and guaranteed issue available

- Excellent customer service and claims reputation

- Competitive rates across all age groups

Coverage Options:

- Simplified Issue: Up to $50,000

- Guaranteed Issue: $2,000-$50,000

- Ages 45-85 accepted

Sample Rates (Age 60, Female, $15,000, Guaranteed Issue): $85/month

Approval Process:

- Online, phone, or mail application

- Guaranteed issue: instant approval

- Simplified issue: 24-48 hour decision

- Straightforward, senior-friendly process

What Makes Them Special: Mutual of Omaha understands seniors. Their underwriters aren’t looking for reasons to decline you—they’re looking for reasons to approve you. They evaluate your whole health picture, not just isolated conditions.

Customer Experience: Consistently high ratings for claims processing. When beneficiaries file claims, they get paid quickly without hassles—exactly what you want.

Best For: Seniors in their 60s who want a reliable, established company with fair pricing and excellent service. Great all-around choice.

2. AARP/New York Life – Best for Healthy Seniors (Simplified Issue)

Why They’re Excellent:

- Backed by AAA-rated New York Life (highest possible rating)

- Group rates through AARP membership

- Best rates available for simplified issue

- Coverage up to $100,000

- Trusted brand with exceptional financial strength

Coverage Options:

- Simplified Issue only (must answer health questions)

- $5,000-$100,000 available

- Ages 50-80 accepted

Sample Rates (Age 60, Female, $15,000, Simplified Issue): $65/month

Requirements:

- AARP membership ($16/year—anyone can join immediately)

- Must qualify on health questions (no recent hospitalizations, etc.)

- Generally good health required

What Makes Them Special: If you qualify, AARP rates are often 20-30% lower than competitors. The AAA backing means absolute certainty they’ll pay claims. Group buying power translates to lower premiums.

The Catch: They will decline applications if you have significant health issues. This is a simplified issue specialist, not for everyone—but if you qualify, it’s the best rate you’ll find.

Best For: Healthy seniors in their 60s with no major health issues and no recent hospitalizations. If you can answer health questions favorably, start here.

Application Tip: Join AARP first ($16), then apply. The membership pays for itself immediately with lower rates.

3. Globe Life – Best Budget Option

Why They’re Popular:

- Often lowest guaranteed issue rates

- Simple application process

- Accept ages 50-85

- A financial rating

- Both policy types available

Coverage Options:

- Guaranteed Issue: $5,000-$50,000

- Simplified Issue: Available

- Very straightforward pricing

Sample Rates (Age 60, Female, $15,000, Guaranteed Issue): $80/month

What Makes Them Special: Globe Life consistently offers the lowest premiums in guaranteed issue. If budget is your primary concern and you need guaranteed issue, start here.

The Trade-Off: Customer service reviews are mixed. You’ll get good rates, but don’t expect hand-holding through the process. It’s a bit more “transactional” than Mutual of Omaha.

Best For: Budget-conscious seniors who prioritize lowest premium over service experience. Great if you’re comfortable with a more self-service approach.

4. Gerber Life – Best for Small Policies

Why They’re Good:

- Specialize in $5,000-$25,000 policies

- Very simple application (3-5 minutes)

- Guaranteed acceptance

- Good rates for smaller amounts

- Ages 50-80

Coverage Options:

- Guaranteed Issue: $5,000-$25,000

- Focus on final expense coverage

Sample Rates (Age 60, Female, $10,000, Guaranteed Issue): $55/month

What Makes Them Special: If you only need $10,000-$15,000 for funeral costs, Gerber’s rates are excellent for these smaller amounts. Application is extremely simple—perfect if you find paperwork overwhelming.

Best For: Seniors who just want enough to cover funeral ($10,000-$15,000) and want the simplest possible process.

5. Foresters Financial – Best Online Experience

Why They’re Modern:

- Complete application 100% online

- Instant approval (guaranteed issue)

- No phone calls or paperwork required

- Member benefits included

- A financial rating

Coverage Options:

- Guaranteed Issue: $5,000-$30,000

- Ages 40-80

- Entirely digital process

Sample Rates (Age 60, Female, $15,000, Guaranteed Issue): $90/month

What Makes Them Special: If you’re comfortable with technology and want to complete everything online without talking to anyone, Foresters is perfect. Their online portal is intuitive and senior-friendly.

Member Benefits: Includes scholarship programs, financial counseling, and emergency assistance benefits for members.

Best For: Tech-comfortable seniors who prefer online applications over phone calls. Great for those who want to handle everything digitally at their own pace.

6. AIG (American General) – Best for Health Issues

Why They’re Lenient:

- Most understanding underwriters

- Approve cases other companies decline

- Excellent with multiple health conditions

- Simplified issue specialists

- Strong financial rating

Coverage Options:

- Simplified Issue: Their specialty

- Larger amounts available

- Very experienced with health conditions

Sample Rates (Age 60, Female, $15,000, Simplified Issue): $75/month

What Makes Them Special: AIG’s underwriters actually understand that seniors have health issues. They look at the whole picture—how well you manage conditions, stability, treatment compliance—not just diagnoses.

Best For: Seniors with multiple managed health conditions (diabetes + high blood pressure + high cholesterol, for example) who want to try simplified issue before resorting to guaranteed issue.

Application Strategy: If you have health issues but think you might qualify for simplified issue, try AIG. They approve cases others decline.

👉 Compare the best life insurance companies for seniors with health problems to explore your options.

Company Quick Comparison Table

| Company | Best For | Policy Types | Max Age | Rating | Approx Rate* |

|---|---|---|---|---|---|

| Mutual of Omaha | Overall best | Both | 85 | A+ | $85 |

| AARP/NY Life | Healthy seniors | Simplified | 80 | AAA | $65** |

| Globe Life | Lowest price | Both | 85 | A | $80 |

| Gerber Life | Small policies | Guaranteed | 80 | A | $55*** |

| Foresters | Online app | Guaranteed | 80 | A | $90 |

| AIG | Health issues | Simplified | 85 | A | $75** |

*Age 60, Female, $15,000, Guaranteed Issue

**Simplified Issue (must qualify)

***$10,000 coverage

Is Life Insurance Worth It After 60?

Many seniors over 60 assume life insurance is too expensive or difficult to qualify for, but that’s often not true.

Life insurance can still help:

- protect spouses

- cover final expenses

- leave money for children or grandchildren

- provide peace of mind during retirement

For many families, even modest coverage can reduce financial stress significantly.

Real Rates: What You’ll Actually Pay

Let’s look at real numbers. Here are actual rates you can expect for life insurance for seniors over 60:

Understanding the Rate Factors

Several factors affect your premium:

1. Age (Biggest Factor): Every year of age increases premiums 8-12%. This is why applying at 60 vs 65 makes a huge financial difference.

2. Gender: Women pay 15-25% less than men for identical coverage due to longer life expectancy.

3. Smoking Status: Smokers pay roughly double what non-smokers pay. If you quit smoking 12+ months ago, you may qualify for non-smoker rates at some companies. Cigar smokers may qualify for non tobacco rates.

4. Coverage Amount: Rates scale proportionally. Want $20,000 instead of $10,000? Premium roughly doubles.

5. Policy Type: Simplified issue (if you qualify) costs 30-50% less than guaranteed issue for same coverage.

6. Health Conditions: For simplified issue, managed multiple conditions have minimal impact. For guaranteed issue, health doesn’t affect rates at all.

7. Company: Rates vary 25-40% between companies for identical coverage. Shopping matters.

Cost Examples at Different Ages

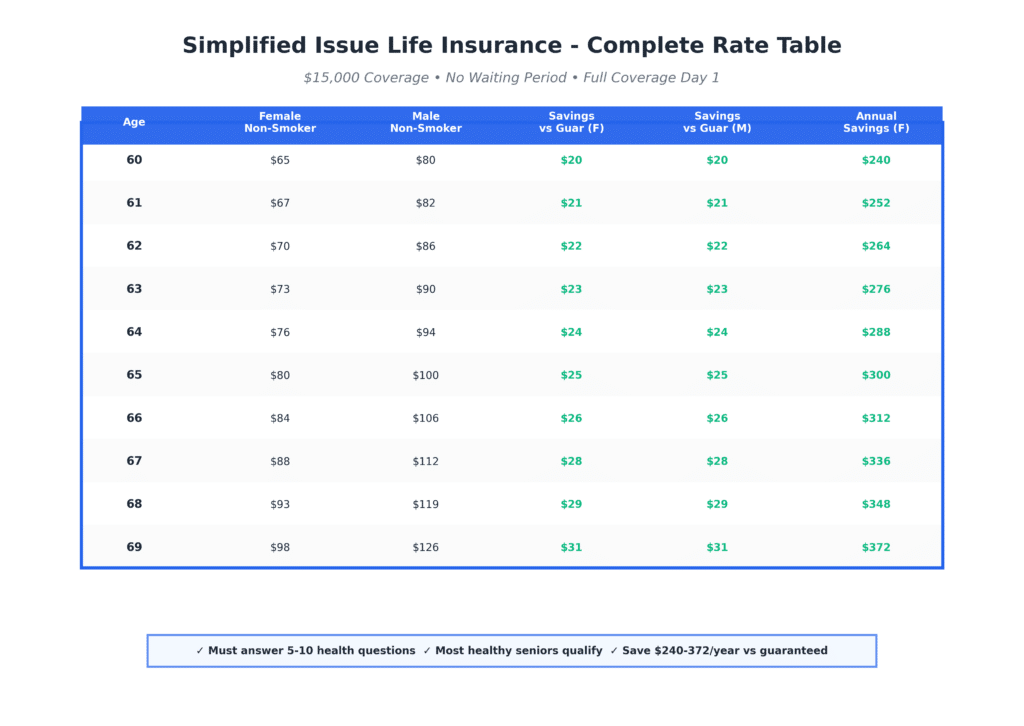

Female, Non-Smoker, $15,000 Guaranteed Issue:

- Age 60: $85/month ($1,020/year)

- Age 62: $92/month ($1,104/year)

- Age 65: $105/month ($1,260/year)

- Age 69: $125/month ($1,500/year)

Male, Non-Smoker, $15,000 Guaranteed Issue:

- Age 60: $100/month ($1,200/year)

- Age 62: $108/month ($1,296/year)

- Age 65: $125/month ($1,500/year)

- Age 69: $150/month ($1,800/year)

The Waiting Cost: If a 60-year-old woman waits until 65 to apply:

- Age 60 rate: $85/month

- Age 65 rate: $105/month

- Difference: $20/month × 12 months × 20 years = $4,800 lifetime cost of waiting

Check out our blog post about simplified issue life insurance vs. guaranteed issue life.

How to Choose the Best Option for YOU

With so many companies and options, how do you know to try simplified issue or guaranteed acceptance first? Here’s my proven framework:

Step 1: Assess Your Health Honestly

Answer These Questions:

- Have you been hospitalized in the past 2 years?

- No → Try simplified issue first

- Yes → Go straight to guaranteed issue

- Do you currently use oxygen?

- No → Try simplified issue

- Yes → Guaranteed issue only

- Do you have well-controlled chronic conditions (diabetes, high BP, etc.)?

- Yes, well-controlled → Try simplified issue

- Multiple or poorly controlled → Guaranteed issue

- Has it been 3+ years since any heart attack, stroke, or cancer?

- Yes → Try simplified issue

- No → Guaranteed issue

- Are you comfortable answering health questions honestly?

- Yes → Try simplified issue

- No/prefer not to → Guaranteed issue

Your Decision:

- Mostly “try simplified” answers? Start with AARP, Mutual of Omaha, or AIG

- Mostly “guaranteed” answers? Start with Globe Life, Mutual of Omaha, or Foresters

- Mixed answers? Try simplified first, switch to guaranteed if declined

Step 2: Determine How Much Coverage You Need

Quick Calculation:

- Average funeral costs: $12,000-$15,000

- Final medical bills: $2,000-$5,000

- Outstanding debts (credit cards, loans): $______

- Cushion for family/inheritance: $______

- Total = Your Coverage Amount

Most Popular Choices:

- $10,000: Basic funeral coverage only

- $15,000: Funeral plus small cushion (most common)

- $20,000: Comfortable coverage with breathing room

- $25,000: Generous coverage plus inheritance

My Recommendation: Most seniors in their 60s buy $15,000-$20,000. This handles funeral costs plus provides extra for unexpected final expenses or as a small inheritance.

Step 3: Get Multiple Quotes

Never buy from just one company. Here’s how to shop effectively:

Option 1 – Direct Contact:

- Call or visit websites of 4-5 companies

- Request written quotes for same coverage amount

- Compare rates side-by-side

Option 2 – Independent Agent:

- Find an independent agent (represents multiple companies)

- They do the shopping for you

- Get quotes from multiple companies at once

- Usually no cost to you (companies pay commission)

Option 3 – Online Comparison:

- Use quote comparison tools

- See multiple rates instantly

- Good for preliminary research

What to Compare:

- Monthly premium

- Annual total cost

- Company financial rating (A- or better)

- Policy type (simplified vs guaranteed)

- Coverage details (waiting period, etc.)

- Customer reviews

Time Investment: Spend 2-3 hours shopping properly. This saves $200-500 annually for the rest of your life.

Step 4: Consider Your Priorities

Different seniors have different priorities. Which matters most to you?

Lowest Price:

- Primary: Globe Life (guaranteed)

- Secondary: AARP (simplified, if qualify)

Best Service:

- Primary: Mutual of Omaha

- Secondary: AARP/New York Life

Easiest Process:

- Primary: Foresters (online)

- Secondary: Gerber (simple app)

Health Issues:

- Primary: AIG (simplified)

- Secondary: Mutual of Omaha (guaranteed)

Highest Coverage:

- Primary: AARP (up to $100K simplified)

- Secondary: Mutual of Omaha (up to $50K guaranteed)

Most Trusted:

- Primary: AARP/New York Life (AAA rated)

- Secondary: Mutual of Omaha (A+ rated)

Step 5: Apply Strategically

The Smart Strategy:

If You’re Healthy:

- Try simplified issue at AARP first (best rates)

- If declined, try AIG or Mutual of Omaha simplified

- If still declined, apply guaranteed issue

If You Have Health Issues:

- Try AIG simplified issue first (lenient underwriters)

- If declined, try Mutual of Omaha simplified

- If declined, apply guaranteed issue immediately

If You Want Certainty:

- Go straight to guaranteed issue

- Get quotes from Globe Life, Mutual of Omaha, Foresters

- Choose lowest rate

The Hybrid Approach: Apply for both types simultaneously:

- Simplified issue at one company

- Guaranteed issue at another

- If simplified approves, take it (better rates)

- If declined, you already have guaranteed approved

Real Stories: Seniors in Their 60s Who Got Covered

Let me share actual examples (names changed for privacy):

Linda’s Story – Age 60, Simplified Issue Success

Background: Linda just turned 60, in good health, takes only a statin for cholesterol. No hospitalizations in 15 years. Active lifestyle, volunteers regularly.

What She Did:

- Joined AARP for $16/year

- Applied for $20,000 simplified issue through AARP

- Answered health questions honestly (cholesterol medication only)

- Provided doctor information

The Outcome: Approved in 24 hours at $75/month. No waiting period—full coverage from day one. Linda said, “I put this off for years thinking it would be complicated. Took me 15 minutes to apply online, and I was approved the next day. I feel so relieved.”

Lesson: Healthy seniors in their early 60s should start with simplified issue. The rates are excellent and approval is fast.

Robert’s Story – Age 64, Multiple Conditions

Background: Robert, 64, has diabetes (A1C 7.8), high blood pressure, high cholesterol, and is overweight. Takes multiple medications. No recent hospitalizations but was hospitalized 3 years ago for pneumonia.

What He Did:

- Applied for simplified issue at AIG (known for lenient underwriting)

- Listed all medications honestly

- Provided detail about his stable diabetes management

- Mentioned 3 years since hospitalization

The Outcome: AIG approved him for simplified issue at $110/month for $15,000. Robert was shocked—he thought he’d need guaranteed issue. He said, “I assumed with all my conditions, I’d be rejected. AIG actually read my application and saw that everything is well-managed and stable.”

Lesson: Multiple managed conditions don’t automatically disqualify you from simplified issue. Companies like AIG evaluate the whole picture. Always try simplified first.

Margaret’s Story – Age 67, Guaranteed Issue After Decline

Background: Margaret, 67, has COPD, used oxygen at night, and had been hospitalized twice in the past year for breathing issues. Knew she likely wouldn’t qualify for simplified issue.

What She Did:

- Applied for simplified issue at AARP anyway (always worth trying)

- Was declined due to oxygen use and recent hospitalizations

- Immediately applied for guaranteed issue at Globe Life

- Got instant approval

The Outcome: Globe Life approved her instantly at $145/month for $15,000. Has a 2-year waiting period, but full coverage after that. Margaret said, “After AARP said no, I was discouraged. But Globe Life approved me in literally 5 minutes with no questions asked. I have peace of mind knowing my kids won’t have funeral expenses.”

Lesson: One decline doesn’t mean you can’t get coverage. Guaranteed issue accepts literally everyone. Don’t give up.

James and Susan’s Story – Age 62 and 60, Couple’s Approach

Background: James (62) and Susan (60) wanted coverage for both. Susan is very healthy. James has heart disease—had a stent 4 years ago but has been stable since.

What They Did:

- Susan applied for simplified issue at AARP (healthy, best rates)

- James applied for guaranteed issue at Mutual of Omaha (recent heart issue)

- Got separate $15,000 policies for each

The Outcome:

- Susan: Approved simplified at $68/month (no waiting period)

- James: Approved guaranteed at $115/month (2-year waiting)

- Combined: $183/month for $30,000 total family coverage

Susan said, “We’re spending about $6 per day combined to protect each other. James’s heart issues meant he couldn’t get simplified issue, but guaranteed issue still gave us options.”

Lesson: Couples should each get their own policy tailored to their individual health. One spouse might get simplified while the other needs guaranteed.

Patricia’s Story – Age 69, Shopping Saved Her Money

Background: Patricia, 69, wanted guaranteed issue for simplicity (didn’t want to answer health questions even though she’s relatively healthy).

What She Did:

- Requested quotes from 6 different companies

- Rates varied significantly:

- Colonial Penn: $158/month

- Mutual of Omaha: $125/month

- Globe Life: $118/month

- Chose Globe Life (lowest rate)

The Outcome: Saves $40/month ($480/year) compared to Colonial Penn for identical coverage. Patricia said, “I almost just went with Colonial Penn because I see their commercials. My daughter convinced me to get other quotes. I’m saving almost $500 a year for 30 minutes of research.”

Lesson: Shopping multiple companies saves real money. Don’t buy based on TV ads—compare actual rates.

Thomas’s Story – Age 65, Applied Just in Time

Background: Thomas turned 65 and had been “meaning to apply” since age 60. Finally decided to do it when he realized Medicare doesn’t cover life insurance.

What He Did:

- Applied at age 65 for $20,000 guaranteed issue

- Approved at $140/month

The Cost of Waiting: If Thomas had applied at age 60:

- Age 60 rate would have been: $105/month

- Age 65 actual rate: $140/month

- Difference: $35/month × 12 × 15 years = $6,300 he paid by waiting

Thomas said, “I thought I was saving money by waiting. I wasn’t. I was literally throwing away thousands of dollars.”

Lesson: Every year you wait costs you money permanently. Apply now, not later.

Step-by-Step Application Process

Let me walk you through exactly how to apply:

Step 1: Gather Your Information

What You’ll Need:

For Everyone (Guaranteed or Simplified):

- Full name, address, date of birth

- Social Security number

- Driver’s license or state ID

- Beneficiary information (full names, dates of birth, SSN)

- Payment method (bank account or credit card)

Additional for Simplified Issue:

- Current medications (names and dosages)

- Doctor names and contact information

- Dates of any hospitalizations (past 2 years)

- Health conditions being treated

Pro Tip: Write this information down before starting the application. Makes the process much faster.

Step 2: Decide on Coverage Amount

Before applying, know exactly how much you want:

- $10,000 (basic funeral)

- $15,000 (funeral plus cushion) ← most popular

- $20,000 (comfortable coverage)

- $25,000 (generous coverage)

You can’t change this after approval, so think it through now.

Step 3: Complete the Application

For Guaranteed Issue (5-10 minutes):

- Go to company website or call phone number

- Choose coverage amount

- Enter personal information

- Name your beneficiary

- Provide payment information

- Submit

- Get instant approval

- Done!

For Simplified Issue (15-25 minutes):

- Start application (online or phone)

- Enter personal information

- Answer health questions honestly and specifically

- Provide medication details

- List doctor information

- Name beneficiary

- Provide payment information

- Submit for underwriting review

- Wait 24-48 hours for decision

- If approved, pay first premium

Step 4: Answer Health Questions Properly (Simplified Issue)

The Golden Rules:

- Be honest (lying voids your policy)

- Be specific (dates, names, dosages)

- Be positive where truthful (“well-controlled,” “stable,” “compliant”)

Example Question: “What medications do you currently take?”

✓ Good Answer:

“Metformin 500mg twice daily for type 2 diabetes, Lisinopril 10mg once daily for blood pressure, Lipitor 20mg once daily for cholesterol. All conditions well-controlled, stable for 5+ years.”

✗ Bad Answer:

“Some diabetes and blood pressure pills.”

Example Question: “Have you been hospitalized in the past 2 years?”

✓ Good Answer:

“Yes, in June 2023 for a knee replacement surgery. Fully recovered, no complications.”

✓ Also Good:

“No.”

✗ Bad Answer:

“I don’t think so” or “Maybe?”

Be Certain and Specific: Vague answers raise red flags. Clear, detailed answers show transparency and improve approval odds.

Step 5: Set Up Payment

Payment Options:

- Monthly automatic bank draft (most popular)

- Monthly automatic credit card

- Quarterly or annual payment (sometimes saves 5-10%)

- Phone payments each month

- Mailed checks (not recommended—easy to miss)

Critical: Set up automatic payments. Missing a payment can cause your policy to lapse, and reapplying at an older age costs more.

Step 6: Review Your Policy Documents

Documents arrive within 7-10 days (mail and/or email).

Verify Everything:

- ✓ Your name spelled correctly

- ✓ Coverage amount matches what you applied for

- ✓ Premium matches your quote

- ✓ Beneficiaries listed correctly with right percentages (should add to 100%)

- ✓ Policy type (guaranteed vs simplified)

- ✓ Waiting period terms (if guaranteed issue)

30-Day Free Look Period: You have 30 days to review everything and cancel for full refund if anything is wrong. Use this time!

Call the Company If:

- Anything looks incorrect

- You have questions about terms

- Premium is higher than quoted

- Beneficiary information is wrong

Common Application Mistakes to Avoid

Mistake #1: Waiting for “The Perfect Time” There’s no perfect time. Apply now. Every month of delay costs money.

Mistake #2: Not Shopping Multiple Companies Rates vary 30-40% between companies for identical coverage. Always compare.

Mistake #3: Being Dishonest on Health Questions Insurance companies verify information. Dishonesty voids your policy—your family gets nothing.

Mistake #4: Choosing Wrong Coverage Amount Think carefully. You can’t easily increase later, and decreasing means you already paid higher premiums.

Mistake #5: Not Reading the Policy Use your 30-day free look period. Read everything. Make sure it matches what you expected.

Mistake #6: Canceling Existing Coverage Too Early If switching companies, wait until new policy is active before canceling old policy. Overlap briefly.

Frequently Asked Questions

What is the best life insurance for seniors over 60?

The best life insurance for seniors over 60 depends on your health and priorities, but for most seniors, the top recommendation is Mutual of Omaha for its combination of competitive rates, excellent service, both simplified and guaranteed issue options, A+ financial rating, and acceptance up to age 85.

For healthy seniors who can answer health questions favorably, AARP/New York Life offers the absolute best rates (backed by AAA-rated New York Life) through simplified issue policies up to $100,000. For budget-conscious seniors needing guaranteed issue, Globe Life consistently offers the lowest premiums.

The “best” choice is the one that balances your specific needs: if you’re healthy (no hospitalizations past 2 years, no oxygen use, managed conditions), start with AARP simplified issue for lowest rates; if you have health issues but conditions are managed, try AIG or Mutual of Omaha simplified issue; if you have significant health issues, recent hospitalizations, or want certainty without health questions, choose guaranteed issue from Globe Life or Mutual of Omaha.

Your 60s are the ideal decade for life insurance—rates are 40-60% lower than age 70+, you qualify for more policy types, and you can secure larger coverage amounts. The key is to shop 3-5 companies, compare rates for identical coverage, and apply sooner rather than later since rates increase 8-12% with each year of age.

Most seniors over 60 choose permanent whole life insurance (marketed as final expense) in amounts of $15,000-$25,000 to cover funeral costs ($12,000-15,000 average) plus final expenses.

Can seniors over 60 get life insurance with no medical exam?

Yes, absolutely—no medical exam life insurance is actually the standard for seniors over 60. There are two primary types: Guaranteed issue requires zero health questions and no medical exam whatsoever (everyone accepted regardless of conditions like cancer, heart disease, COPD, diabetes, or anything else), with instant approval but typically includes a 2-3 year waiting period and costs 30-50% more than simplified issue.

Simplified issue requires answering 5-12 health questions but still no medical exam, blood tests, or doctor visits, with approval in 24-48 hours, no waiting period (full coverage from day one), and premiums 30-50% lower than guaranteed issue—most healthy seniors in their 60s qualify even with managed chronic conditions. The health questions for simplified issue typically ask about hospitalizations in past 1-2 years, oxygen use, terminal illness, recent heart attack/stroke (past 2-5 years), recent cancer (past 5-10 years), and kidney dialysis—but well-controlled diabetes, high blood pressure, high cholesterol, arthritis, and similar common conditions usually don’t prevent approval.

Traditional fully underwritten policies (with medical exams, blood tests, and extensive underwriting) are rarely used for seniors over 60 because the simplified and guaranteed issue options provide better value and easier qualification at this age. The strategy is to try simplified issue first if you’re in decent health (saves 30-50% on premiums), and if declined, immediately switch to guaranteed issue where approval is certain.

Companies like Mutual of Omaha, AARP/New York Life, Globe Life, Foresters, and AIG all offer no-exam options specifically designed for seniors in their 60s.

How much does life insurance cost for a 60 year old?

Life insurance costs for 60 year olds vary based on gender, smoking status, policy type, and coverage amount, but here are real rates for $15,000 coverage: For guaranteed issue (no health questions, everyone approved), a 60-year-old female non-smoker pays approximately $80-90/month ($960-1,080/year), while a male non-smoker pays $95-110/month ($1,140-1,320/year).

Female smokers pay $140-165/month and male smokers $175-210/month. For simplified issue (must answer health questions and qualify), rates are 30-50% lower: females pay $60-75/month and males $75-95/month for the same coverage, with no waiting period and immediate full coverage. These rates are for permanent whole life insurance where premiums never increase—the rate you lock in at 60 stays the same at 70, 80, or 90.

Coverage amount directly affects price: $10,000 costs about 67% of these rates, $20,000 costs about 133%, and $25,000 costs about 167%. The cost difference between companies is significant—rates vary 25-40% for identical coverage, so shopping multiple companies saves $15-35/month ($180-420/year). Age makes a huge difference: every year of age increases premiums 8-12%, so a 61-year-old pays 10% more than a 60-year-old for life.

Waiting from age 60 to 65 increases rates by 30-40%, costing $20-30/month more ($240-360/year) permanently. For perspective, most 60-year-olds pay $60-110/month ($720-1,320/year) for $15,000 of coverage—roughly $2-4 per day, which is less than a coffee, and provides $15,000 to cover funeral costs that average $12,000-15,000.

The best rates at age 60 go to healthy non-smokers who qualify for simplified issue through AARP ($60-65/month for females, $75-80/month for males), while guaranteed issue rates at budget-friendly Globe Life start around $80/month for females and $95/month for males.

Is 60 too old to get life insurance?

No, 60 is definitely not too old for life insurance—in fact, your 60s are often the ideal time to apply. Age 60-69 is considered the “sweet spot” for senior life insurance for several important reasons: rates are 40-60% lower than age 70+ for identical coverage (a 60-year-old pays roughly half what a 75-year-old pays), you still qualify for multiple policy types including simplified issue (no exam, just health questions) and guaranteed issue (no questions at all), your health is typically better now than it will be at 70-75, making simplified issue approval more likely with better rates, most companies accept applicants up to age 85 (Mutual of Omaha, Globe Life) or age 80 (AARP, Gerber), and you can secure larger coverage amounts ($50,000-$100,000+) which become harder or impossible to get after age 75.

The real concern isn’t whether 60 is “too old”—it’s that waiting until 65 or 70 costs you thousands of dollars in permanently higher premiums due to the 8-12% annual rate increase with each year of age. Real example: a 60-year-old woman pays $85/month for $15,000 guaranteed issue; if she waits until 70, that same coverage costs $135/month—$50/month more ($600/year) for life, totaling $6,000+ extra over 10 years just for waiting. At 60, you’re young enough to get excellent simplified issue rates if healthy (30-50% lower than guaranteed), old enough to recognize the importance of planning ahead, and positioned to lock in rates before age-based increases kick in.

The “too old” concern is actually backwards—you’re not too old at 60; you might be too early at 50 (unnecessary expense for decades), but at 60 you’re in the perfect window. Companies actively want your business at this age, offering competitive rates and easy approval processes.

The only time you’re “too old” is if you exceed a company’s maximum age (usually 80-85), but even then, some companies accept up to age 89. Bottom line: if you’re 60 and wondering if it’s too late, the answer is absolutely not—in fact, applying now is one of the smartest financial decisions you can make. The real question isn’t “Am I too old?” but rather “Why haven’t I done this yet?”

Should I get term or whole life insurance at age 60?

At age 60, whole life insurance (permanent coverage) is almost always the right choice, not term insurance. Here’s why: Term insurance covers you for a specific period (10, 20, 30 years) and expires at the end—if you’re 60 and buy 20-year term, it expires at 80 when you’re most likely to need it, leaving your family with nothing.

Term premiums for seniors over 60 are actually higher than whole life in most cases because insurance companies know the odds of payout during a short term are higher. If you outlive the term (which many seniors do), you’ve paid premiums for years and receive zero benefit.

Whole life insurance (also called permanent or final expense insurance) covers you for your entire life regardless of when you pass—70, 80, 90, or 100, your beneficiaries get paid. Premiums are locked in forever—pay $100/month at 60, still pay $100/month at 85 (never increases).

You’re guaranteed a payout eventually since everyone passes away; it’s not “if” but “when,” making whole life a certainty rather than a gamble. Small cash value builds over time that you can borrow against in emergencies.

At age 60, you need coverage for whenever you pass away (covering final expenses, funeral costs, outstanding debts), not just for the next 10-20 years. Your need doesn’t expire—funeral costs don’t disappear at age 80. The rate comparison proves the point: at 60, whole life guaranteed issue costs $85-100/month for $15,000, while 20-year term (if available) costs $90-120/month for same coverage—term is actually more expensive and expires right when you need it most.

The term vs whole debate makes sense for 30-year-olds (term for temporary income replacement needs), but at 60+, whole life is almost universally the better choice. This is why companies market “final expense” and “burial insurance” to seniors—it’s just whole life insurance packaged for permanent needs. Exception: the only time term makes sense at 60 is for very specific short-term needs (covering a 10-year business loan, for example), but for personal funeral costs and family protection, whole life is the answer.

When shopping for life insurance for seniors over 60, focus on permanent whole life policies from companies like Mutual of Omaha, AARP, Globe Life, or Gerber—these are designed specifically for your age and needs.

Can I get life insurance if I have diabetes, high blood pressure, or other conditions?

Yes, you can definitely get life insurance with diabetes, high blood pressure, or other health conditions—in fact, most seniors in their 60s have one or more chronic conditions and still get approved.

For guaranteed issue life insurance, your health literally doesn’t matter at all—diabetes, heart disease, COPD, cancer history, high blood pressure, high cholesterol, kidney disease, stroke history, obesity, or any combination of conditions result in automatic approval with no health questions asked and the same rates as everyone your age and gender.

For simplified issue life insurance, approval depends on how well conditions are managed: well-controlled diabetes (A1C under 8-9, stable on medications, no recent hospitalizations, no complications like kidney failure or amputations) usually qualifies at companies like AIG, Mutual of Omaha, or Foresters, often with only a small rate increase or sometimes even standard rates if controlled for many years.

High blood pressure controlled with medication and no recent complications typically qualifies easily for simplified issue—this is one of the most common conditions and rarely prevents approval. High cholesterol on statins with stable levels is usually approved without issue, especially if your “good” HDL cholesterol is high (60+).

Multiple conditions together (the “diabetes + high blood pressure + high cholesterol” combination many seniors have) can still qualify for simplified issue at lenient companies like AIG if all conditions are managed, stable, and well-controlled. What matters most to underwriters is control and stability: Are you taking prescribed medications? Are your numbers improving or stable? When was your last hospitalization? Do you see your doctors regularly? Are you compliant with treatment?

Conditions that make simplified issue more difficult include recent hospitalizations (within past 1-2 years), oxygen use for COPD, recent heart attack or stroke (within 2-5 years), active cancer treatment, kidney dialysis, terminal illness, or poorly controlled conditions with frequent ER visits.

The strategy is to try simplified issue first even with health conditions—companies like AIG specifically look at the whole picture and approve many cases others decline. If declined, guaranteed issue accepts you with certainty regardless of conditions.

Real example: Robert, 64, has diabetes (A1C 7.8), high blood pressure, high cholesterol, and is overweight—applied to AIG simplified issue and was approved because all conditions were stable and managed. Patricia, 67, has COPD with oxygen use—knew she needed guaranteed issue and got instantly approved at Globe Life.

The key is matching your application to your health reality: healthy or managed conditions → try simplified first; significant health issues or want certainty → go guaranteed. Don’t self-reject thinking your conditions disqualify you—let the underwriter decide, or choose guaranteed issue where nothing disqualifies you.

How quickly can I get approved?

Approval speed depends on policy type: Guaranteed issue provides instant approval (literally within minutes)—complete application online or by phone, get approved immediately with no waiting for underwriting, and coverage is active as soon as you pay your first premium (usually same day or next business day).

Simplified issue typically takes 24-48 hours for a decision—submit application with health questions, underwriter reviews your answers and may verify information, decision rendered within 1-2 business days, occasionally takes up to 3-5 days if they need additional information from your doctor.

The fastest application path is guaranteed issue through companies with online applications: Foresters offers complete online application with instant approval in 5-10 minutes with no phone calls required. Globe Life provides instant approval online or by phone.

Mutual of Omaha gives same-day approval for guaranteed issue. For simplified issue, AARP/New York Life averages 24-36 hour approval, AIG typically approves within 48 hours, and Mutual of Omaha runs 24-48 hours for decisions.

Factors that speed up approval: having all information ready (medications, doctor info, dates), answering questions clearly and specifically, responding immediately if company requests additional information, and applying online rather than by mail.

Factors that slow down approval: incomplete applications missing information, vague or unclear health answers requiring follow-up, applying by mail (adds 1-2 weeks), and applying right before weekends or holidays. Once approved, coverage activation is immediate for simplified issue (pay first premium, coverage starts same day) and immediate for guaranteed issue (though waiting period applies for natural death in years 1-2; accidental death covered immediately).

Most seniors in their 60s complete the entire process—application to active coverage—within 1-3 days for guaranteed issue or 2-5 days for simplified issue. Real example: Linda, 60, applied to AARP simplified issue on Monday afternoon, got approved Tuesday morning, paid first premium Tuesday, coverage active Tuesday—total time 24 hours.

Patricia, 64, applied to Globe Life guaranteed issue online, got instant approval, paid immediately, coverage active same day—total time 15 minutes. If you need coverage quickly (for estate planning deadline, upcoming surgery, or just peace of mind), choose guaranteed issue for same-day approval and activation.

Your premium never increases after approval—this is one of the most important features of permanent life insurance for seniors. The monthly premium you lock in at age 60 is the exact same premium you pay at age 70, 80, 90, or even 100. This is called a “level premium” and is guaranteed in your policy contract.

For example: if you’re approved at age 60 for $15,000 coverage at $85/month, you pay $85/month for life, whether you’re 61, 75, or 95—the premium never changes. This is fundamentally different from many other types of insurance (like car or health insurance) that increase over time.

Life insurance premiums are based on your age at application and locked in permanently. What does change with age is what new applicants pay—a new 65-year-old applicant pays more than a new 60-year-old applicant (8-12% more per year), but your existing policy is unaffected.

This locked-in rate is why applying sooner rather than later is crucial: if you apply at 60 and pay $85/month forever, but wait until 65 and pay $110/month forever, you pay an extra $25/month for the rest of your life ($300/year × 20 years = $6,000+ in extra costs) just for waiting.

The only ways your premium changes are if you voluntarily increase coverage (buy more insurance, which requires new application at current age), if you miss payments and policy lapses then reinstate (you’d pay current age rates), or if you reduce coverage (some policies allow this, lowering your premium).

But as long as you pay your premiums on time, your rate is locked forever. This is one of the most valuable features for seniors on fixed incomes—you can budget knowing your life insurance cost will never increase, even as other expenses rise.

It provides financial predictability and protection against inflation (your $85/month in 2025 will still be $85/month in 2045, even though most other costs will have doubled).

Some policies even offer “paid-up” options where after 15-20 years of payments, your policy is fully paid and requires no more premiums while coverage continues for life, though most seniors over 60 simply keep paying the same locked-in premium since it never increases and remains affordable.

Can married couples get joint life insurance?

While joint life insurance policies exist, they’re rarely the best choice for seniors over 60—instead, you should each get individual policies. Here’s why individual policies are better: Coverage continues for both spouses rather than paying out only once—joint policies pay when the first person dies, leaving the surviving spouse without coverage.

Each spouse can choose appropriate coverage amounts based on their individual needs (maybe wife wants $15,000 and husband wants $20,000). Each spouse can select the appropriate policy type based on their health (one might qualify for simplified issue while the other needs guaranteed issue).

Premiums are tailored to each person’s age, gender, and health rather than being averaged together. If one spouse passes away, the other’s coverage remains active and unchanged. Beneficiary designations are simpler (children, grandchildren, other family). Divorce, separation, or estate planning is much cleaner with individual policies.

The cost comparison usually favors individual policies: for example, James (62) and Susan (60) could buy one joint policy for perhaps $180/month that pays $25,000 once (when first person dies), OR they could buy individual policies: Susan gets $15,000 simplified issue at $68/month, James gets $15,000 guaranteed at $115/month, total $183/month for $30,000 total coverage (pays $15,000 when Susan dies AND another $15,000 when James dies).

The individual approach provides double the total payout for nearly the same premium. The application process is straightforward: each spouse applies separately to companies best suited to their situation, you can apply to different companies (Susan to AARP, James to Globe Life, for example), you name each other as primary beneficiaries with children as contingent, and you manage two separate policies with separate premiums (or combine payments if same company).

Some couples consolidate with one company for simplicity: both apply to Mutual of Omaha, manage through single portal, coordinate beneficiary designations, and sometimes receive multi-policy discounts. The only scenario where joint life makes sense is for very specific estate planning needs (covering estate taxes, business succession) that don’t apply to most seniors.

For typical funeral and final expense coverage, individual policies give you more flexibility, better total coverage, and equal or better value. Strategy tip: apply for both policies simultaneously so you’re both covered quickly, even if one application takes longer than the other.

What if I’m declined by one company?

Being declined by one insurance company does not mean you can’t get life insurance—it simply means you should apply to a different company or switch to guaranteed issue.

Here’s exactly what to do: If declined for simplified issue, immediately apply for guaranteed issue life insurance at any company (Mutual of Omaha, Globe Life, Foresters, Gerber Life) which accepts everyone regardless of health with no questions asked, provides instant approval with certainty, and ensures you get covered even if simplified issue declined you.

Try a different company for simplified issue since underwriting guidelines vary significantly between companies—AIG might approve what AARP declines, Mutual of Omaha might approve what Globe Life declines, and one company’s “no” doesn’t predict another company’s decision.

Understand why you were declined by contacting the company that declined you, asking specifically what factors led to the decline (recent hospitalization? specific condition? medication?), and getting written explanation (they’re required to provide this).

Address the decline reason if possible: if declined due to very recent health event, wait 3-6 months for stability then reapply; if declined due to incomplete information, provide additional documentation showing controlled conditions; if declined due to misunderstanding, clarify the situation with detailed medical records. Don’t take it personally—declines are common and don’t reflect on you as a person, just on one company’s specific underwriting criteria.

Real examples: Robert applied to AARP simplified issue and was declined due to multiple conditions (diabetes + high BP + COPD), but AIG approved him because they’re more lenient with multiple managed conditions. Margaret was declined by Globe Life simplified but instantly approved by Globe Life guaranteed issue—same company, different product.

Thomas was declined by three companies for simplified issue (recent heart attack) but guaranteed issue at Foresters approved him instantly. Strategy after decline: don’t give up or assume you’re uninsurable, don’t try 5-10 simplified issue companies if first 2 decline (diminishing returns), switch to guaranteed issue quickly for certainty, consider working with an independent insurance agent who knows which companies approve which situations.

The guaranteed issue option ensures literally no senior is uninsurable—as long as you’re within the age range (typically 50-85), you’re approved regardless of health history, medications, hospitalizations, or previous declines. One client was declined by 4 companies for simplified issue (serious health issues) but got instant guaranteed approval and said “I felt defeated after the fourth ‘no,’ but guaranteed issue said ‘yes’ in 5 minutes. I wish I’d known about it sooner.”

Are life insurance payouts taxable?

No, life insurance death benefits are not taxable as income to beneficiaries in the vast majority of cases. Your beneficiaries receive the full death benefit completely tax-free—no federal income tax, no state income tax (in most states), and typically no inheritance tax.

For example, a $20,000 policy pays exactly $20,000 to beneficiaries with zero taxes owed, regardless of the beneficiary’s income level, regardless of the policy size, and regardless of the deceased’s estate size in most cases. This tax-free treatment applies whether death occurs from natural causes or accidents, whether it’s year 1 or year 30 of the policy, and whether beneficiaries are family members, friends, or organizations.

The rare exceptions affecting less than 1% of Americans: if your total estate exceeds $13.61 million (2024 federal estate tax threshold), estate taxes might apply to the estate itself, but this doesn’t affect beneficiaries’ receipt of the death benefit as income-tax-free; if the death benefit earns interest before being paid out (if beneficiaries delay claiming it), the interest portion may be taxable as income, though the death benefit itself remains tax-free; if the policy was transferred to another person within 3 years of death for estate planning purposes, it might be included in estate calculations, but beneficiaries still don’t pay income tax on the benefit.

For the typical senior over 60 purchasing $10,000-$25,000 final expense coverage, beneficiaries receive 100% of the death benefit tax-free with no IRS reporting requirements or tax forms to file. This makes life insurance one of the most tax-efficient ways to transfer wealth.

Additional benefits: death benefits don’t go through probate (the legal process of settling an estate), meaning beneficiaries receive money directly and quickly (usually within 7-14 days of filing claim) without court involvement, probate costs, or public records. Death benefits are also protected from creditors in most states—your debt collectors cannot claim your life insurance proceeds; they go directly to your named beneficiaries. Important: beneficiaries should file claims promptly after death, insurance companies don’t automatically know when policyholders pass away, and filing typically requires just a death certificate and claim form (process takes 7-14 days).

The tax-free nature of life insurance is one of its greatest advantages for seniors planning ahead—you can be certain your intended beneficiaries receive the full amount you planned, with no surprise tax bills reducing what you meant to leave them.

Taking Action: Your Next Steps

You’ve learned everything about finding the best life insurance for seniors over 60. Now let’s get you covered:

This Week – Decide and Apply:

Monday-Tuesday:

- Assess your health honestly using framework in this guide

- Decide if you should try simplified issue or go guaranteed

- Calculate how much coverage you need ($10K, $15K, $20K, $25K)

- Write down your decision

Wednesday-Thursday:

- Get quotes from 4-5 companies

- Simplified: AARP, Mutual of Omaha, AIG

- Guaranteed: Globe Life, Mutual of Omaha, Foresters

- Request written quotes for your coverage amount

- Compare rates side-by-side

- Choose 1-2 companies to apply with

Friday:

- Gather required information (see application section)

- Complete application(s)

- Pay first premium

- Get confirmation of coverage

This Month – Secure Your Coverage:

Week 2:

- Respond to any company requests immediately

- For simplified issue: wait for approval decision (24-48 hours)

- For guaranteed issue: coverage already active

Week 3:

- Receive policy documents by mail/email

- Read everything carefully during 30-day free look period

- Verify all information is correct

- Call company if anything needs correction

Week 4:

- File policy documents in safe, accessible place

- Confirm automatic payments are working

- Tell beneficiaries about policy (company name, policy number)

- Consider giving beneficiaries copies of policy

Ongoing – Maintain Your Coverage:

Every Year:

- Verify payments are processing

- Review beneficiary designations

- Update beneficiaries if life changes (deaths, births, divorces)

- Confirm policy is active (call company if unsure)

After Major Life Events:

- Update beneficiaries immediately

- Consider increasing coverage if needs change

- Adjust coverage if desired

Don’t Delay – The Cost of Waiting:

Remember: Every single year you wait costs you money permanently.

Real Cost of Waiting (Female, $15,000):

- Apply at 60: $85/month for life

- Wait until 65: $110/month for life

- Cost of waiting 5 years: $300/year × 20 years = $6,000

Your Health May Change: You’re healthier today than you’ll be in 5 years. Health issues that develop limit you to more expensive options.

The Best Time:

- Best time to apply: 5 years ago

- Second-best time: This week

Final Thoughts

Finding the best life insurance for seniors over 60 isn’t about finding a “perfect” option that checks every box. It’s about finding the right option for YOU—your health, your budget, your priorities.

You don’t need perfect health. You don’t need to be wealthy. You don’t need to understand complex insurance jargon. You just need to:

- Assess your health honestly

- Get 3-5 quotes

- Choose the best rate from a solid company

- Apply this week

- Pay your first premium

That’s it. 15-20 minutes of action provides thousands of dollars of protection for your family.

I’ve watched too many seniors procrastinate. They think, “I’ll do it next year” or “I need to research more” or “I’m still young.” Then next year becomes five years. Research becomes paralysis. And “still young” becomes “significantly older with higher rates.”

Don’t be that person.

You’re in your 60s—the perfect decade for life insurance. Rates are still reasonable. You qualify for good policy types. Companies want your business. You can lock in rates before age-based increases accelerate.

Susan, my neighbor who called me at age 60, finally applied after our conversation. She got approved for $20,000 at AARP for $75/month. She called me a week later and said, “I can’t believe I put this off for so long. This weight I didn’t even know I was carrying is finally gone. My kids are so relieved.”

Take action this week. Get those quotes. Complete that application. Give yourself and your family that same peace of mind.

You can do this. And you should.

Your family will thank you for it.

Disclaimer: This article provides general information about life insurance for seniors over 60 and should not be considered insurance, financial, or legal advice. Insurance products, rates, company policies, availability, underwriting guidelines, and terms vary by state, individual circumstances, age, health status, smoking status, coverage amount, and are subject to change without notice. Premium rates quoted are approximate ranges for illustration purposes based on 2025 market averages and may not reflect actual rates available to you. Always verify current rates, terms, and availability directly with insurance companies. Compare multiple quotes from licensed insurers and review complete policy documents including exclusions, limitations, waiting periods, and terms before purchasing. Health conditions, medications, and medical history affect simplified issue approval and rates but not guaranteed issue acceptance. Consult licensed insurance professionals for personalized guidance regarding your specific situation. This guide is not affiliated with or endorsed by any insurance company mentioned. Information is current as of publication date but insurance products, company offerings, and regulations change frequently. No guarantee is made regarding policy approval, premium rates, coverage availability, or terms for any individual applicant. Financial strength ratings are subject to change and should be verified with rating agencies.