Life Insurance for Seniors with Arthritis: A Complete 2026 Guide

Posted in Life Insurance w/ Pre-existing Conditions on January 28, 2026 last updated on June 10, 2026

Posted in Life Insurance w/ Pre-existing Conditions on January 28, 2026 last updated on June 10, 2026

Is Life Insurance for Seniors with Arthritis possible?

Yes, seniors with arthritis can usually qualify for life insurance.

In fact, most people with arthritis are approved for coverage, especially when the condition is well-managed and does not significantly impact overall health.

Many seniors are surprised to learn that arthritis alone rarely causes a life insurance decline.

Insurance companies understand that arthritis is common among older adults and often focus more heavily on factors such as mobility, medications, other health conditions, and overall health history.

Whether you have osteoarthritis, rheumatoid arthritis, psoriatic arthritis, or another form of arthritis, there are often multiple life insurance options available.

Potential coverage options include:

- Traditional life insurance

- Term life insurance

- Whole life insurance

- No medical exam life insurance

- Simplified issue life insurance

- Final expense insurance

- Guaranteed issue life insurance

The best option depends on your age, overall health, arthritis severity, medications, and whether other medical conditions are present.

Quick Answer

If you’re looking for the short version:

What Is Arthritis?

Arthritis is not a single disease.

Instead, arthritis refers to a group of conditions that cause inflammation, pain, stiffness, and reduced mobility in the joints.

According to the Centers for Disease Control and Prevention (CDC), arthritis is one of the most common chronic health conditions affecting older adults.

Symptoms can include:

- Joint pain

- Stiffness

- Swelling

- Reduced range of motion

- Difficulty walking

- Fatigue

- Weakness

The severity of arthritis can vary dramatically from one person to another.

Some seniors experience only occasional discomfort, while others may have significant mobility limitations that affect daily activities.

Because of these differences, life insurance companies evaluate arthritis on a case-by-case basis.

How Life Insurance Companies View Arthritis

Before applying for life insurance for seniors with arthritis, it helps to understand how insurers evaluate the condition. Not all forms of arthritis are treated the same, and the type you have plays a major role in pricing and approval.

Osteoarthritis vs. Rheumatoid Arthritis: Why Insurers Treat Them Differently

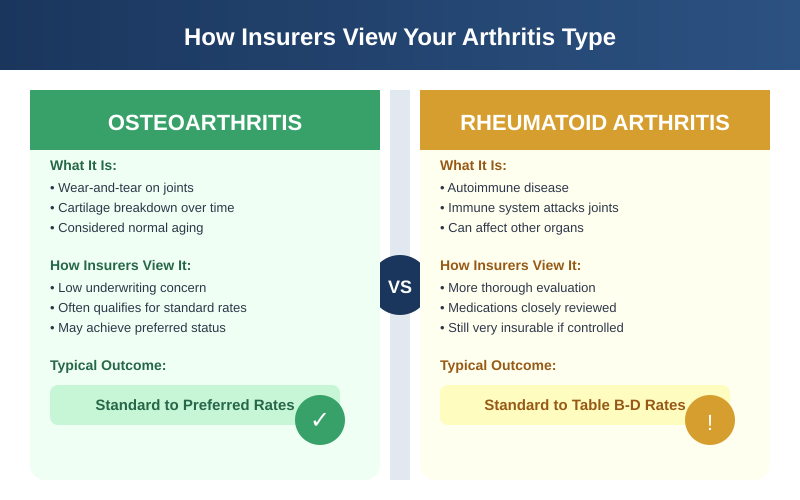

Insurance underwriters draw a clear distinction between osteoarthritis (OA) and rheumatoid arthritis (RA).

Osteoarthritis (OA)

Osteoarthritis is the most common form of arthritis.

It occurs when the protective cartilage within joints gradually wears down over time.

Commonly affected areas include:

- Knees

- Hips

- Hands

- Spine

- Shoulders

Life Insurance Outlook

Osteoarthritis is generally viewed favorably by insurance companies.

Applicants with mild to moderate osteoarthritis often qualify for standard or even preferred rates if no significant health issues are present.

Rheumatoid Arthritis

Rheumatoid arthritis (RA) is an autoimmune disease that causes the body’s immune system to attack healthy joint tissue.

Unlike osteoarthritis, rheumatoid arthritis can affect multiple organs and body systems.

Insurance companies may review:

- Disease severity

- Medication history

- Joint damage

- Organ involvement

- Hospitalizations

Reason: Many RA applicants have additional conditions.

Life Insurance Outlook

Many applicants with rheumatoid arthritis still qualify for life insurance.

However, underwriting is often more detailed than for osteoarthritis.

Psoriatic Arthritis

Psoriatic arthritis is an inflammatory condition that affects some individuals with psoriasis.

Insurance companies may evaluate:

- Severity of symptoms

- Medication usage

- Mobility limitations

- Overall health history

Life Insurance Outlook

Mild cases generally receive favorable consideration.

More severe cases may receive additional underwriting review.

Gout

Gout is a form of inflammatory arthritis caused by elevated uric acid levels.

Insurance companies often review:

- Frequency of flare-ups

- Medication usage

- Kidney function

- Other health conditions

Life Insurance Outlook

Most applicants with controlled gout qualify for coverage without significant difficulty.rease long-term health risks, insurers review it more carefully and may apply higher rates depending on severity and progression.

What Underwriters Look at When Seniors With Arthritis Apply

ery insurance company uses different underwriting guidelines.

However, most carriers review several common factors.

Severity of Arthritis

One of the biggest underwriting factors is severity.

Insurance companies often ask:

- How severe is the condition?

- Does it limit daily activities?

- Has mobility been affected?

- Is assistance required?

Mild arthritis generally creates few underwriting concerns.

Severe arthritis may receive additional review.

Medications

Insurance companies frequently review medications such as:

- Methotrexate

- Humira

- Enbrel

- Prednisone

- Celebrex

- Meloxicam

- Hydroxychloroquine

Medication history often helps insurers understand disease severity and control.

Mobility and Daily Activities

Can you walk independently?

Can you perform normal daily activities?

Do you use:

- A cane?

- A walker?

- A wheelchair?

Mobility limitations can affect underwriting decisions because they may indicate more advanced disease.

Joint Replacement History

Many seniors have undergone:

- Knee replacement surgery

- Hip replacement surgery

- Shoulder replacement surgery

Successful joint replacement surgery is often viewed positively because it may improve mobility and quality of life.

Other Health Conditions

Insurance companies frequently review conditions that occur alongside arthritis, including:

- Obesity

- Diabetes

- Heart disease

- High blood pressure

- Kidney disease

- Sleep apnea

- Multiple health conditions

In many cases, these conditions have a greater impact on underwriting than arthritis itself.e tends to be.

Life Insurance Rating Classes Explained (and How Arthritis Fits In)

Insurance companies assign applicants to rating classes that determine pricing. Seniors with arthritis may fall into standard or table-rated categories depending on severity.

Mild Arthritis

Characteristics often include:

- Occasional joint pain

- Minimal stiffness

- No significant mobility limitations

- Controlled with medication or lifestyle changes

- No major complications

Life Insurance Outlook

This group typically receives the most favorable underwriting consideration.

Many seniors with mild arthritis qualify for standard, and occasionally preferred, rates depending on age and overall health.

Moderate Arthritis

Characteristics often include:

- Frequent joint pain

- Reduced range of motion

- Regular medication use

- Periodic flare-ups

- Some mobility limitations

Life Insurance Outlook

Coverage is usually available, although some applicants may receive standard or table-rated classifications depending on other health factors.

Standard Rating Classes

| Rating Class | Description | Arthritis Qualification |

|---|---|---|

| Preferred Plus | Best possible rates | Rare for RA; possible only for very mild OA |

| Preferred | Very good health | Mild OA with no limitations |

| Standard Plus | Slightly above average | Controlled OA or mild RA |

| Standard | Average health | Common outcome for mild–moderate RA |

Severe Arthritis

Characteristics often include:

- Significant mobility limitations

- Difficulty performing daily activities

- Use of assistive devices

- Frequent specialist care

- Multiple medications

Life Insurance Outlook

Traditional underwriting becomes more challenging. Many applicants still qualify, but premiums may be higher and coverage options may become more limited.

Advanced Arthritis

Characteristics often include:

- Wheelchair dependence

- Severe joint damage

- Multiple joint replacements

- Significant disability

- Extensive medical treatment

Life Insurance Outlook

Traditional underwriting may be difficult, but final expense, simplified issue, and guaranteed issue policies are often available.

Table Ratings Explained

If arthritis increases risk beyond standard guidelines, insurers may assign a table rating, which increases premiums in 25% increments.

| Table Rating | Rate Increase | Example ($100 Standard Rate) |

|---|---|---|

| Table A / 1 | +25% | $125 |

| Table B / 2 | +50% | $150 |

| Table C / 3 | +75% | $175 |

| Table D / 4 | +100% | $200 |

| Table E / 5 | +125% | $225 |

| Table F / 6 | +150% | $250 |

| Table G / 7 | +175% | $275 |

| Table H / 8 | +200% | $300 |

Many seniors with well-managed arthritis qualify for standard or low table ratings, especially when symptoms are stable.

Osteoarthritis vs Rheumatoid Arthritis: Which Is Easier to Insure?

| Factor | Osteoarthritis | Rheumatoid Arthritis |

|---|---|---|

| Underwriting Difficulty | Lower | Higher |

| Autoimmune Disease | No | Yes |

| Organ Involvement Possible | No | Yes |

| Mobility Impact | Usually Localized | Can Be Widespread |

| Medication Review | Moderate | Extensive |

| Approval Opportunities | Excellent | Good to Moderate |

While both conditions can qualify for coverage, osteoarthritis generally receives more favorable underwriting treatment.

Arthritis-Friendly Life Insurance Companies for Seniors

Some insurers are known for being more flexible with applicants who have arthritis. These companies frequently appear in searches for life insurance for seniors with arthritis because of their underwriting approach.

| Company | AM Best Rating | Why They’re Senior-Friendly |

|---|---|---|

| Prudential | A+ | Flexible underwriting for chronic conditions |

| Mutual of Omaha | A+ | Strong final expense options, guaranteed acceptance |

| Pacific Life | A+ | Favorable senior term rates, no-exam options |

| Protective Life | A+ | Competitive pricing with health considerations |

| Transamerica | A | High age limits and conversion flexibility |

| Banner Life | A+ | Competitive term rates for seniors |

| Corebridge (AIG) | A | Conversion options and senior flexibility |

| State Farm | A++ | Strong customer satisfaction and fast approvals |

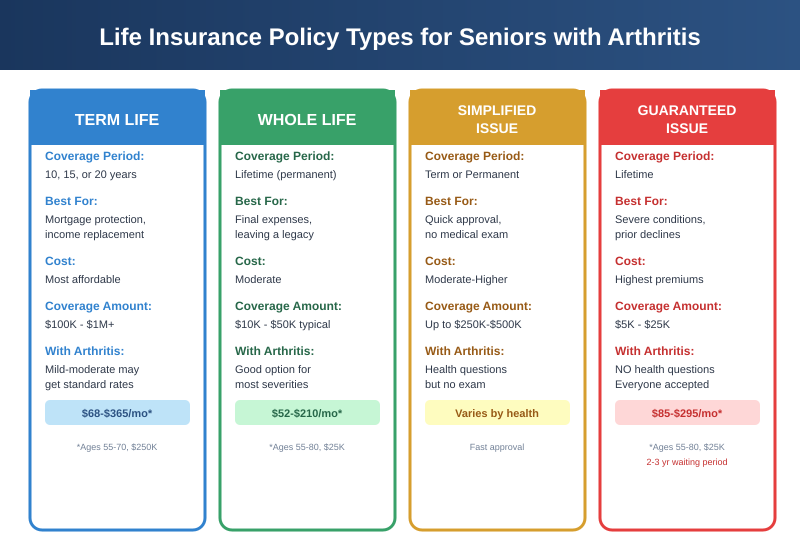

Types of Life Insurance for Seniors with Arthritis

Depending on the severity of your arthritis, most types of life insurance are available whether it is term, whole life, or final expense.

Term Life Insurance

Term life insurance offers coverage for a fixed period (10–20 years) and is usually the most affordable option. Seniors with mild to moderate arthritis often qualify for standard or near-standard rates.

Whole Life Insurance

Whole life insurance provides permanent coverage and builds cash value. It’s a strong option for seniors who want lifelong protection or coverage for final expenses.

Simplified Issue Life Insurance

Simplified issue policies also known as final expense insurance requires health questions but no medical exam. They offer faster approval and moderate pricing, making them a popular option for seniors with controlled arthritis.

Guaranteed Issue Life Insurance

Guaranteed issue policies accept applicants regardless of health. They are often used when arthritis is severe or other conditions are present. These policies cost more and usually include a waiting period. These policies are most used for seniors with health conditions.

What Underwriting Class Can You Qualify For With Arthritis?

Many seniors want to know how arthritis affects rates.

The answer depends on severity, medications, mobility, and overall health.

Preferred

Possible for:

- Mild osteoarthritis

- Minimal symptoms

- Excellent overall health

- No significant medical conditions

Standard

Common for:

- Mild to moderate arthritis

- Controlled symptoms

- Stable medical history

Table Rated

Common for:

- Rheumatoid arthritis

- Multiple health conditions

- Significant mobility limitations

Simplified Issue

Common for:

- Moderate to severe arthritis

- Older applicants

- Multiple medications

➡️ Guaranteed Issue vs Simplified Issue Life Insurance

Guaranteed Issue

Often considered when:

- Traditional underwriting is unavailable

- Significant disabilities exist

- Multiple serious health conditions are present

Sample Life Insurance Rates for Seniors With Arthritis

Term Life Insurance Rates (10-Year Term, $250,000 Coverage)

| Age | Male (Standard) | Female (Standard) | Male (Table B) | Female (Table B) |

|---|---|---|---|---|

| 55 | $68 | $52 | $102 | $78 |

| 60 | $105 | $78 | $158 | $117 |

| 65 | $185 | $138 | $278 | $207 |

| 70 | $365 | $275 | $548 | $413 |

Whole Life / Final Expense Rates ($25,000 Coverage)

| Age | Male | Female | Guaranteed Issue |

|---|---|---|---|

| 55 | $52 | $40 | $85 |

| 60 | $68 | $52 | $105 |

| 65 | $88 | $68 | $135 |

| 70 | $115 | $92 | $175 |

| 75 | $155 | $125 | $225 |

| 80 | $210 | $175 | $295 |

➡️ Average Life Insurance Rates for seniors

Arthritis and Obesity

Obesity often increases stress on weight-bearing joints and may contribute to arthritis symptoms.

Insurance companies frequently review:

- BMI

- Blood pressure

- Diabetes history

- Mobility limitations

- Overall health

Many applicants with both arthritis and obesity still qualify for coverage.

Arthritis and Diabetes

Diabetes commonly occurs alongside arthritis, particularly among older adults.

Insurance companies often evaluate:

- A1C levels

- Medication usage

- Kidney function

- Neuropathy

- Cardiovascular history

Well-controlled diabetes generally results in more favorable underwriting outcomes.

Arthritis and Heart Disease

Heart disease is one of the most common conditions reviewed alongside arthritis.

Insurance companies may evaluate:

- Previous heart attacks

- Stents

- Bypass surgery

- Blood pressure

- Cholesterol levels

The overall cardiovascular picture often has a larger impact on underwriting than arthritis itself.

Arthritis and Joint Replacement Surgery

Many seniors applying for life insurance have undergone joint replacement surgery.

Common procedures include:

- Knee replacement

- Hip replacement

- Shoulder replacement

Insurance companies generally view successful joint replacement surgery positively because it often improves mobility, reduces pain, and increases quality of life.

Underwriters may review:

- Date of surgery

- Recovery status

- Complications

- Current mobility

- Physical therapy outcomes

Applicants who recover successfully and regain mobility often receive more favorable consideration than those with ongoing limitations.

Arthritis and Sleep Apnea

Sleep apnea commonly occurs alongside arthritis, particularly among seniors who experience obesity, chronic inflammation, reduced mobility, or other health conditions. In some cases, joint pain and discomfort can also contribute to poor sleep quality, making sleep-related disorders more common.

When evaluating life insurance applications, insurance companies may review:

- Whether sleep apnea has been diagnosed

- CPAP machine usage and compliance

- Severity of the condition

- Oxygen levels during sleep studies

- Associated health conditions

- Overall cardiovascular health

Well-controlled sleep apnea generally receives favorable underwriting consideration. Many applicants who consistently use their CPAP machine and follow their physician’s recommendations are able to qualify for competitive rates.

However, untreated sleep apnea may receive additional underwriting review because it can increase the risk of heart disease, stroke, high blood pressure, and other medical complications.

For many seniors, sleep apnea has a greater impact on underwriting than arthritis itself. Insurance companies often evaluate the complete health picture rather than focusing on a single diagnosis.

Learn more in our guide to Life Insurance for Seniors with Sleep Apnea.

Arthritis and Kidney Disease

Kidney disease is another condition that may occur alongside arthritis, particularly among seniors with rheumatoid arthritis, diabetes, high blood pressure, or long-term use of certain medications.

Insurance companies often review:

- Stage of kidney disease

- Kidney function test results

- Creatinine levels

- Estimated GFR (glomerular filtration rate)

- Dialysis history

- Diabetes status

- Blood pressure control

In many cases, the severity of kidney disease has a larger impact on life insurance approval and rates than arthritis itself.

Applicants with mild or stable kidney disease often qualify for coverage, especially when the condition is well-managed and monitored by a physician. However, advanced kidney disease or dialysis treatment may significantly limit available options and lead insurers to recommend simplified issue, final expense, or guaranteed issue coverage.

Because arthritis, diabetes, high blood pressure, and kidney disease frequently occur together, underwriters typically evaluate the overall health profile rather than any one condition in isolation.

Learn more in our guide to Life Insurance for Seniors with Kidney Disease.

➡️ Affordable Life Insurance for Seniors

Real-Life Example

A 69-year-old applicant contacted us after assuming that rheumatoid arthritis would prevent her from qualifying for affordable life insurance.

She had been diagnosed more than 10 years earlier and was taking medication to manage her symptoms.

Her health profile included:

- Rheumatoid arthritis

- Controlled high blood pressure

- No history of heart disease

- No diabetes

- Active lifestyle

- No smoking history

Several years earlier, she had been told that autoimmune conditions often made life insurance difficult to obtain.

As a result, she delayed applying.

When we reviewed her situation, we discovered that her arthritis had remained stable for years and that she maintained regular medical care.

While some insurance companies viewed rheumatoid arthritis more cautiously, others focused more heavily on her overall health profile.

Factors that worked in her favor included:

- Stable symptoms

- No organ involvement

- Good mobility

- Consistent medication compliance

- Strong overall health

After comparing multiple companies, she was approved for coverage that provided meaningful protection for her family.

➡️ Best Life Insurance Companies for Seniors with Health Problems

The experience highlights an important lesson:

A diagnosis alone does not determine your life insurance outcome.

Insurance companies evaluate the entire health picture, not just the presence of arthritis.

Helpful Resources

You may also find these guides helpful:

Tips to Get Approved and Find the Best Rates

Seniors searching for life insurance with arthritis can improve approval odds by:

- Working with an independent broker

- Following prescribed treatment plans

- Providing up-to-date medical records

- Being fully honest on applications

- Comparing multiple insurers

- Applying during stable periods (not flare-ups)

- Requesting reconsideration if health improves

Frequently Asked Questions: Life Insurance for Seniors With Arthritis

Can I get life insurance if I have rheumatoid arthritis?

Yes. Many seniors with mild to moderate RA qualify for standard or table-rated policies, especially when the condition is well controlled.

Do arthritis medications affect life insurance rates?

Yes. NSAIDs usually have minimal impact, while biologics, steroids, or methotrexate may lead to higher premiums.

Can I get life insurance without a medical exam?

Yes. Simplified issue and guaranteed issue policies are available and popular among seniors with arthritis.

No. Once your policy is issued, premiums are typically locked in for life.

Is osteoarthritis treated the same as rheumatoid arthritis?

No. Osteoarthritis is generally viewed as lower risk and often has little impact on rates.

Can you get life insurance if you have arthritis?

Yes. Most seniors with arthritis can qualify for life insurance. Approval depends on factors such as severity, medications, mobility, and overall health.

Does arthritis increase life insurance rates?

Mild arthritis often has little impact on premiums. More severe arthritis or rheumatoid arthritis may receive additional underwriting review.

Is rheumatoid arthritis harder to insure than osteoarthritis?

Generally, yes. Rheumatoid arthritis is an autoimmune disease and may receive more detailed underwriting consideration

Can I get life insurance after a knee replacement?

Yes. knee replacement surgery alone rarely prevents someone from qualifying for life insurance.

What if I have arthritis and other health conditions?

Insurance companies evaluate your complete health profile. Conditions such as diabetes, heart disease, obesity, kidney disease, and sleep apnea may influence underwriting decisions.

What is the easiest life insurance policy to qualify for with arthritis?

Final expense insurance and guaranteed issue life insurance are often among the easiest options to qualify for.

Get Personalized Life Insurance Quotes — Even With Arthritis

Having arthritis does not automatically prevent you from getting life insurance.

Many seniors are surprised to learn they still qualify for affordable coverage, even if they have rheumatoid arthritis, osteoarthritis, joint replacements, mobility limitations, or multiple health conditions.

The key is finding the right insurance company.

Every insurer evaluates arthritis differently. One company may offer standard rates while another may apply stricter underwriting guidelines.

That’s why Rob and Tracy Pinner compare multiple life insurance companies on your behalf.

We Can Help You Compare:

✅ Traditional Life Insurance

✅ No Medical Exam Life Insurance

✅ Simplified Issue Life Insurance

✅ Final Expense Insurance

✅ Guaranteed Issue Life Insurance

Get Help If You Have:

- Osteoarthritis

- Rheumatoid Arthritis

- Psoriatic Arthritis

- Gout

- Joint Replacements

- Diabetes

- Heart Disease

- Obesity

- Multiple Health Conditions

Don’t assume you will be declined or forced to overpay.

Request a personalized quote today and discover which companies may offer the best rates and approval opportunities for your specific health profile.

Get Your Free Life Insurance Quote Today

Why Trust Really Smart Insurance?

Really Smart Insurance specializes in helping seniors compare life insurance options across multiple insurance companies.

We regularly assist applicants with:

- Arthritis

- Diabetes

- Heart Disease

- High Blood Pressure

- Kidney Disease

- Sleep Apnea

- Obesity

- Multiple Health Conditions

Because we are independent agents, we can compare multiple carriers to help identify companies that may offer better rates and approval opportunities based on your unique health history.

Final Thoughts

Arthritis is one of the most common health conditions affecting seniors, and fortunately, it rarely prevents someone from obtaining life insurance.

Whether you have osteoarthritis, rheumatoid arthritis, psoriatic arthritis, gout, or a history of joint replacement surgery, there are often more coverage options available than you might expect.

The key is understanding how insurance companies evaluate arthritis, choosing the right policy type, and comparing multiple carriers.

By working with an independent agency and exploring all available options, many seniors with arthritis are able to find affordable life insurance that helps protect their loved ones and preserve their financial legacy.