Types of Senior Life Insurance Explained: Term vs Whole vs Final Expense

Posted in Final Expense Life Insurance on January 9, 2026 last updated on May 29, 2026

Posted in Final Expense Life Insurance on January 9, 2026 last updated on May 29, 2026

What are the main types of Senior Life Insurance?

The most common types of senior life insurance include term life insurance, whole life insurance, final expense insurance, no medical exam life insurance, simplified issue policies, and guaranteed issue life insurance. The best option depends on age, health conditions, coverage goals, and budget

If you’re researching coverage later in life, you’ll quickly notice there isn’t just “one” kind of policy. There are several types of senior life insurance, and the best one depends on what you’re trying to protect—income, a spouse, a mortgage, funeral costs, or simply peace of mind.

In this guide, I’ll walk you through the types of life insurance for seniors in plain English—term vs whole vs final expense—including how each policy works, who it’s best for, what to watch out for, and rate charts (typical ranges) so you can budget realistically.

Quick takeaway:

- Term life = most affordable for bigger coverage for a limited time

- Whole life = lifetime coverage + cash value (higher premiums)

- Final expense = smaller whole life policy built to cover funeral/end-of-life costs

- No Medical Exam Life = term life or whole life polices that require no exam but do ask health questions

- Simplified Issue Life = no exam required but does ask a few health questions

- Guaranteed Issue Life = everyone is approved. no health questions

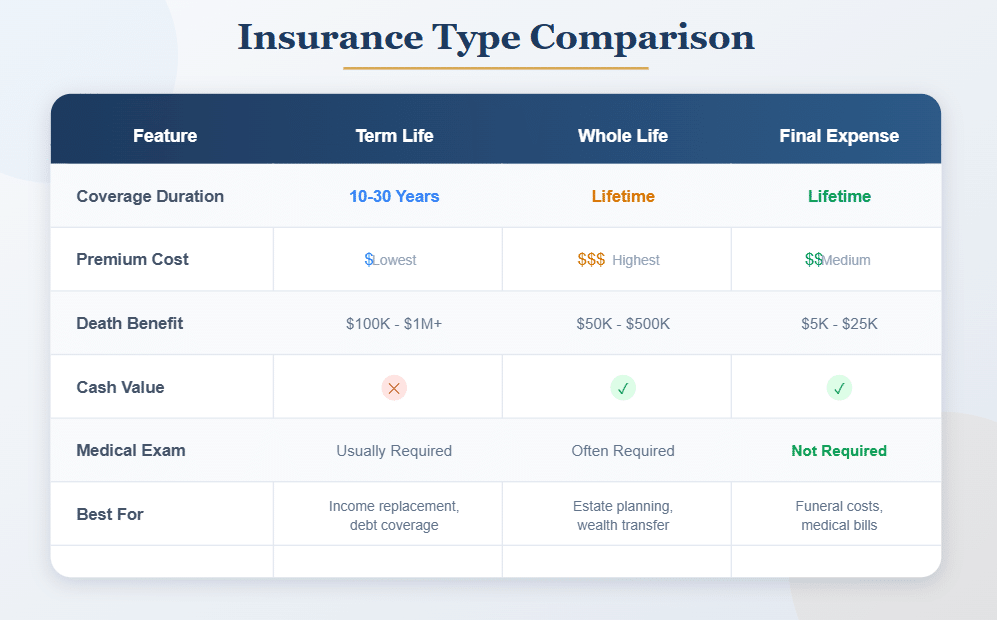

A Quick Comparison

| Policy Type | Medical Exam | Best For | Coverage Amount | Approval Difficulty |

|---|---|---|---|---|

| Term Life | Sometimes | Healthy seniors needing larger coverage | Higher | Moderate |

| Whole Life | Sometimes | Permanent protection | Moderate–High | Moderate |

| Final Expense | Usually No | Funeral costs | Smaller | Easier |

| No Medical Exam | No | Faster approvals | Moderate | Easier |

| Simplified Issue | No | Moderate health conditions | Moderate | Easier |

| Guaranteed Issue | No | Serious health conditions | Lower | Guaranteed |

1) Term Life Insurance for Seniors

What is term life insurance?

Term life insurance covers you for a specific length of time (the “term”), such as 10, 15, or 20 years. If you pass away during the term, your beneficiaries receive the death benefit. If you outlive the term, coverage ends (unless you renew, which is typically much more expensive).

This is the simplest version of the types of senior life insurance—and for the right situation, it can be extremely cost-effective.

Why seniors choose term life

Best For:

- Healthier seniors

- Income replacement

- Mortgage protection

- Larger coverage amounts

- Temporary financial needs

Term life insurance is often one of the most affordable options for seniors who are still in relatively good health and want higher coverage amounts for a specific period of time.

Many adults in their:

still qualify for term life insurance depending on their health and overall risk profile.

Pros:

- Lower premiums

- Larger death benefits

- Flexible term lengths

Cons:

- Approval may be harder with health conditions

- Coverage eventually expires

- Premiums increase with age

Term life rate chart (Typical ranges, 2026 estimates)

Below are illustrative monthly premium ranges for a 10-year term policy.

Assumptions: non-smoker, average health, U.S. market; actual rates vary by state, company, and underwriting.

10-Year Term Rate Chart (Monthly Premium Estimates)

| Age | $100,000 Coverage | $250,000 Coverage |

|---|---|---|

| 60 | $40–$75 | $85–$160 |

| 65 | $55–$100 | $120–$220 |

| 70 | $85–$160 | $190–$350 |

| 75 | $140–$260 | $320–$600+ |

Important note for seniors: Many carriers reduce maximum term lengths and coverage amounts as age increases—so availability becomes part of the decision.

2) Whole Life Insurance for Seniors

What is whole life insurance?

Whole life insurance is permanent coverage that lasts your entire life (as long as premiums are paid). It also builds cash value, which is money that grows inside the policy over time.

Whole life is a cornerstone category when discussing the types of senior life insurance explained, because it’s built for long-term certainty—fixed premiums, guaranteed death benefit, and lifetime coverage.

Best For:

- Seniors wanting permanent coverage

- Estate planning

- Lifelong financial protection

- Predictable premiums

- Building cash value

Whole life insurance provides permanent protection that remains active for life as long as premiums are paid.

These policies are commonly used by seniors who:

- want stable premiums

- dislike temporary coverage

- want to leave money to family members

- want coverage for funeral expenses or final bills

Pros:

- Permanent coverage

- Fixed premiums

- Builds cash value

Cons:

- Higher premiums than term life

- Coverage amounts may be smaller for older applicants

Whole life rate chart (Typical ranges, 2026 estimates)

Below are typical monthly ranges for senior whole life with common face amounts.

Assumptions: non-smoker, average health.

Whole Life Rate Chart (Monthly Premium Estimates)

| Age | $25,000 Coverage | $50,000 Coverage |

|---|---|---|

| 60 | $95–$150 | $180–$290 |

| 65 | $120–$190 | $230–$360 |

| 70 | $155–$240 | $300–$470 |

| 75 | $210–$330 | $400–$650 |

Why ranges are wide: whole life pricing varies a lot depending on underwriting class, whether it’s simplified issue, and how the insurer structures benefits and riders.

3) Final Expense Insurance (Burial Insurance)

What is final expense insurance?

Final expense insurance also called burial insurance is a type of permanent life insurance (usually whole life) designed specifically to cover:

Best For:

- Funeral and burial costs

- Seniors over 70

- Smaller coverage needs

- Easier approval

- Applicants wanting no medical exam options

Final expense insurance is one of the most popular types of life insurance for seniors because approval is often easier and coverage is designed specifically for end-of-life expenses.

Many seniors use final expense insurance to help cover:

- funeral costs

- cremation expenses

- medical bills

- small debts

Pros:

- Easier approval

- Usually no medical exam

- Permanent coverage

Cons:

- Smaller death benefits

- Higher cost per dollar of coverage

Final expense vs whole life: what’s the difference?

Final expense vs whole life? Final expense is essentially a “smaller, simplified issue” whole life policy. It usually has:

- lower coverage amounts (often $5,000–$25,000)

- simplified underwriting (often no medical exam)

- faster approvals

Final expense rate chart (Typical ranges, 2026 estimates)

Assumptions: non-smoker, average health (simplified issue). Guaranteed issue versions can cost more.

Final Expense Rate Chart (Monthly Premium Estimates)

| Age | $10,000 Coverage | $15,000 Coverage | $20,000 Coverage |

|---|---|---|---|

| 60 | $40–$60 | $60–$85 | $75–$110 |

| 65 | $50–$75 | $75–$105 | $95–$135 |

| 70 | $65–$95 | $95–$135 | $120–$170 |

| 75 | $85–$125 | $125–$180 | $160–$230 |

| 80 | $110–$170 | $170–$250 | $220–$320 |

4) No Medical Exam Life Insurance

Best For:

- Faster approvals

- Seniors with moderate health conditions

- Applicants avoiding medical exams

- Simplified underwriting

- Convenience

No medical exam life insurance allows many seniors to apply without:

- bloodwork

- urine testing

- physical exams

Instead, insurers often review:

- prescription history

- medical records

- health questionnaires

These policies are increasingly popular among seniors with:

Pros:

- Faster approval process

- No physical exam

- Easier application process

Cons:

- Premiums may be higher

- Coverage limits may apply

5) Simplified Issue Life Insurance

Best For:

- Moderate health conditions

- Seniors wanting easier approval

- Applicants declined for traditional coverage

- Faster underwriting

Simplified issue life insurance requires health questions but usually skips medical exams and lab testing.

These policies often work well for seniors who:

- have manageable medical conditions

- want quicker approvals

- still want reasonable coverage amounts

Pros:

- Easier approval

- Faster underwriting

- No medical exam

Cons:

- Health questions still apply

- Serious conditions may still lead to denial

6) Guaranteed Issue Life Insurance

Best For:

- Serious health conditions

- Previous life insurance denials

- Seniors over 80

- Applicants needing guaranteed approval

- Burial and funeral coverage

Guaranteed issue life insurance is designed for applicants who may struggle to qualify for traditional coverage because of age or severe medical conditions.

These policies usually:

- require no medical exam

- ask few or no health questions

- guarantee approval in most cases

Guaranteed issue coverage is commonly considered by seniors with:

- severe heart disease

- COPD

- stroke history

- cancer history

- multiple health conditions

Pros:

- Guaranteed approval

- No medical exam

- No health questions

Cons:

- Higher premiums

- Smaller coverage amounts

- Waiting periods often apply

Best Types of Life Insurance for Seniors with Health Conditions

Different policy types work better depending on health history and underwriting risk.

| Health Condition | Often Recommended Policy Types |

|---|---|

| Diabetes | Simplified Issue / No Exam |

| Past Cancer | Simplified Issue / No Exam |

| Heart Disease | Final Expense / Simplified Issue |

| Stroke History | Guaranteed Issue / Final Expense |

| COPD | Guaranteed Issue / No Exam |

| Multiple Conditions | Guaranteed Issue |

| Sleep Apnea | Simplified Issue / No Exam |

Many seniors with chronic medical conditions still qualify for coverage, especially when conditions are stable and well-managed.

Best Life Insurance Types by Age

Seniors Over 50

Often still qualify for:

- term life

- whole life

- no-exam options

Seniors Over 60

Frequently explore:

- simplified issue

- final expense

- permanent whole life

Seniors Over 70

Often shift toward:

- final expense

- guaranteed issue

- no medical exam coverage

Seniors Over 80

Most commonly consider:

- guaranteed issue

- final expense

- simplified issue whole life

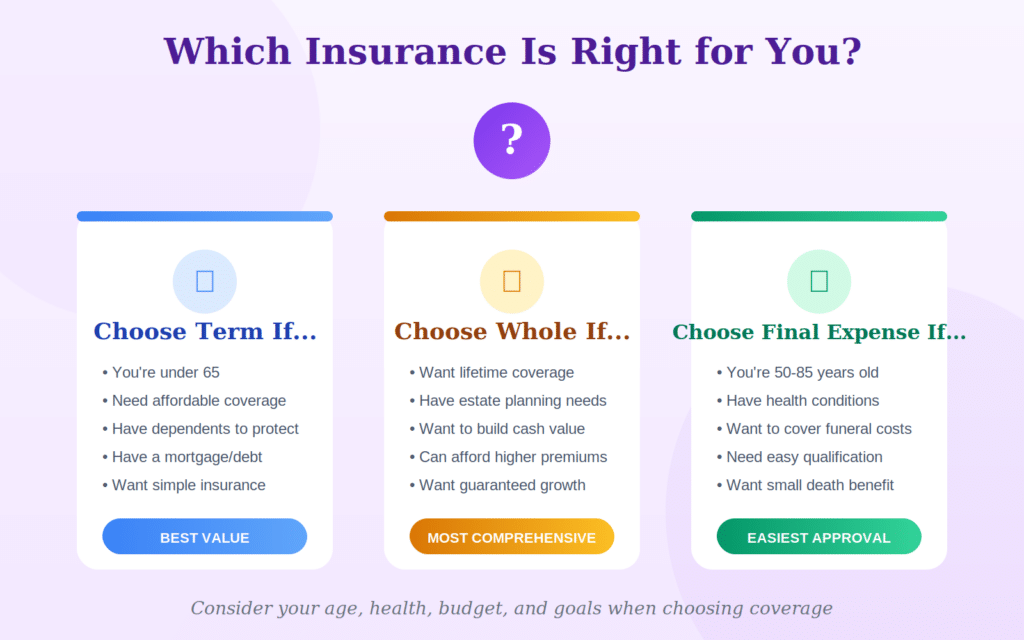

How to Choose Between Term vs Whole vs Final Expense

When people compare the types of senior life insurance, the simplest way to decide is to match the policy to the purpose.

The best type of life insurance depends on:

- age

- health conditions

- financial goals

- desired coverage amount

- budget

For example:

- healthier seniors may prefer term life for affordability

- seniors with health conditions may prefer no-exam or simplified issue coverage

- seniors primarily concerned about burial costs may prefer final expense insurance

Comparing multiple companies and policy types is often the best way to find affordable coverage.

Real-Life Experiences

Real-life example #1: Term life made sense for a short window

Gary, 66, still had 9 years left on a mortgage and wanted to make sure his spouse wouldn’t have to sell the home if something happened. He chose a 10-year term policy with enough coverage to pay off the remaining balance. His goal wasn’t lifetime coverage—just protection during the “high-risk” financial window.

Real-life example #2: Whole life supported legacy planning

Denise, 70, wanted a policy that would never expire and could leave money to her grandchildren. She chose whole life insurance with a manageable premium and felt good knowing coverage would stay in place no matter how long she lived.

Real-life example #3: Final expense prevented family financial stress

Maria, 77, didn’t want her children scrambling to pay for funeral costs. She chose final expense insurance sized at $15,000. When the family eventually needed it, the funds helped cover funeral expenses and travel costs for relatives coming in from out of state.

Common Mistakes Seniors Make When Choosing a Policy

- Buying term life without a plan for what happens when it expires

- Overbuying coverage and choosing a premium that’s hard to maintain

- Assuming final expense is “worse” (it’s often the most practical fit)

- Not comparing policy types side-by-side before applying

- Ignoring waiting periods on guaranteed issue policies

FAQ: Types of Senior Life Insurance Explained

What are the main types of senior life insurance?

The most common types of senior life insurance are term life, whole life, and final expense insurance (which is typically a smaller whole life policy designed for funeral and end-of-life costs).

Which type of senior life insurance is best?

The best policy depends on your goal:

–Term for temporary needs and higher coverage at lower cost

–Whole life for lifetime coverage and legacy planning

–Final expense for funeral costs and easier approval

Is final expense insurance the same as whole life?

Final expense is a form of whole life, but it’s designed with smaller coverage amounts and simplified approval.

Can seniors get term life insurance after age 70?

Sometimes, yes—though term lengths and coverage limits may be reduced. Premiums also rise quickly, so it’s important to compare it against permanent options.

Does whole life insurance build cash value?

Yes. Whole life includes cash value that can grow over time. It’s typically not a “get rich” feature, but it can be helpful for certain planning situations.

Does final expense insurance require a medical exam?

Most final expense policies do not require a medical exam. Many use simplified underwriting (health questions) and some guaranteed issue options have no questions.

Are life insurance payouts taxable?

In most cases, life insurance death benefits are paid to beneficiaries tax-free. (Always confirm with a qualified tax professional for your specific situation.

Can I have more than one type of policy?

Yes. Some seniors use term for a temporary big need and final expense for permanent funeral coverage.

What Type of Life Insurance Is Best for Seniors with Health Conditions?

Seniors with health conditions often benefit from simplified issue, no medical exam, final expense, or guaranteed issue life insurance depending on the severity of their condition. The best option depends on factors such as age, medical history, medications, and the amount of coverage needed. Many seniors are surprised to learn they still qualify for coverage even after a previous denial.

Final Thoughts

When you understand the types of senior life insurance, choosing a policy becomes much simpler. Term life can be perfect for a temporary need, whole life is great for lifetime certainty and legacy goals, and final expense insurance is often the most practical solution for funeral and end-of-life planning.