Term Life Insurance vs Whole Life Insurance for Seniors: Which Is Right for You?

Posted in Types of Life Insurance on December 10, 2025 last updated on December 10, 2025

Posted in Types of Life Insurance on December 10, 2025 last updated on December 10, 2025

Term life insurance vs whole life insurance for seniors is one of the most important financial decisions you’ll. Both options can protect your loved ones, but they work in fundamentally different ways—and the wrong choice could cost you thousands of dollars or leave your family without the coverage they need.

If you’re over 50, 60, or 70 and trying to figure out which type of life insurance makes sense for your situation, you’re in the right place. In this comprehensive guide, we’ll break down everything you need to know about term life vs whole life insurance for seniors, including real rates, the different types of each policy, and a clear framework for making the right decision.

In This Guide:

- What is term life insurance and how does it work?

- What is whole life insurance and how does it work?

- The 5 types of term life insurance explained

- The 4 types of whole life insurance explained

- Current rates and costs comparison by age

- Key differences between term and whole life

- How to choose the right policy for your situation

- Frequently asked questions

What Is Term Life Insurance for Seniors?

Term life insurance is the simplest and most affordable type of life insurance. It provides coverage for a specific period—typically 10, 15, 20, or 30 years—and pays a death benefit to your beneficiaries if you pass away during that term.

Think of term life insurance like renting an apartment. You pay for coverage as long as you need it, but you don’t build any equity or ownership in the policy. When the term ends, your coverage ends too (unless you renew at a higher rate or convert to permanent coverage).

How Term Life Insurance Works

Here’s the basic structure:

- You choose a coverage amount (death benefit) based on your needs—typically $50,000 to $1,000,000 or more

- You select a term length that matches your financial obligations (10, 15, 20, or 30 years)

- You pay fixed monthly or annual premiums that never increase during the term

- If you die during the term, your beneficiaries receive the full death benefit tax-free

- If you outlive the term, coverage ends and you receive nothing back (unless you have a return of premium policy)

Why Seniors Choose Term Life Insurance

Term life insurance appeals to seniors for several reasons:

- Affordability: Premiums are significantly lower than whole life insurance—often 5-10 times cheaper for the same death benefit

- Simplicity: Easy to understand with no complicated investment components

- Flexibility: Choose the exact coverage period you need

- Specific needs: Perfect for covering temporary obligations like a mortgage or providing income replacement during retirement years

What Is Whole Life Insurance for Seniors?

Whole life insurance is a type of permanent life insurance that covers you for your entire lifetime—as long as you continue paying premiums. Unlike term life, whole life insurance includes a savings component called “cash value” that grows over time.

Think of whole life insurance like buying a house. Your premiums build equity (cash value) that you can access during your lifetime, and the coverage remains in place no matter how long you live.

How Whole Life Insurance Works

Here’s the basic structure:

- Coverage lasts your entire life—there’s no expiration date

- Premiums are fixed and guaranteed never to increase

- Cash value accumulates on a tax-deferred basis over time

- You can borrow against or withdraw from your cash value while alive

- Death benefit is guaranteed and paid to beneficiaries whenever you pass away

- Some policies pay dividends that can increase your cash value or reduce premiums

Why Seniors Choose Whole Life Insurance

Whole life insurance appeals to seniors for different reasons:

- Lifetime coverage: Never worry about outliving your policy

- Cash value growth: Build a financial asset you can access if needed

- Fixed premiums: Lock in rates that never increase, even as you age

- Estate planning: Guaranteed death benefit for inheritance or estate taxes

- Final expense coverage: Ensure funeral and burial costs are always covered

The 5 Types of Term Life Insurance

Not all term life insurance policies are the same. Understanding the different types helps you choose the right one for your specific needs.

1. Level Term Life Insurance (Most Popular)

What it is: The death benefit and premium stay exactly the same throughout the entire term.

Best for: Most seniors—it’s simple, predictable, and offers the best overall value.

Example: A 60-year-old buys a 15-year level term policy with a $250,000 death benefit. She pays $101/month for all 15 years. If she dies at age 72, her family receives $250,000. If she’s still alive at 75, coverage ends.

Pros:

- Predictable, fixed premiums

- Lowest cost for guaranteed coverage

- Easy to understand and compare

Cons:

- Coverage ends when term expires

- No cash value accumulation

- Renewal rates are very expensive

2. Annual Renewable Term (ART) Life Insurance

What it is: Coverage that renews automatically each year. Premiums start low but increase annually as you age.

Best for: Seniors who need coverage for an uncertain or short time period (1-5 years).

Example: Tom, age 65, needs coverage while waiting to sell his business. Year 1: $150/month, Year 2: $175/month, Year 3: $205/month. After selling his business, he cancels the policy.

Pros:

- Lower initial premiums

- No long-term commitment

- No medical exam required for renewal

Cons:

- Premiums increase significantly each year

- Becomes very expensive over time

- Difficult to budget

3. Decreasing Term Life Insurance

What it is: The death benefit decreases over time while premiums stay level. Often called “mortgage protection insurance.”

Best for: Covering a mortgage or other debt that decreases over time.

Example: James, age 62, has 15 years left on his $200,000 mortgage. He buys a 15-year decreasing term policy. The death benefit decreases roughly in line with his mortgage balance. He pays a flat $95/month.

Pros:

- 20-40% cheaper than level term

- Matches declining debt obligations

- Fixed monthly payment

Cons:

- Coverage decreases even if your needs don’t change

- Less flexibility

- Not ideal for inheritance purposes

4. Return of Premium (ROP) Term Life Insurance

What it is: If you outlive the policy term, the insurance company refunds 100% of your premiums.

Best for: Seniors who can afford higher premiums and don’t want to “lose” money if they survive the term.

Example: Susan, age 55, buys a 20-year ROP policy. Regular term would cost $175/month, but ROP costs $525/month. Over 20 years, she pays $126,000. At age 75, she’s still alive and receives a $126,000 refund.

Pros:

- Get all your money back if you survive

- Full death benefit if you die during the term

- Acts as forced savings

Cons:

- Premiums are 2-5 times higher than regular term

- Money returned has lost value due to inflation

- Investing the difference elsewhere could yield better returns

5. Increasing Term Life Insurance

What it is: The death benefit automatically increases each year (typically 3-5%) to keep pace with inflation.

Best for: Seniors concerned about inflation eroding their coverage value over a long term.

Example: Robert, age 58, buys a 20-year increasing term policy with an initial $300,000 death benefit that grows 4% annually. By year 20, his coverage has grown to $658,000.

Pros:

- Coverage keeps pace with inflation

- No medical exam needed for increases

- Good for long-term protection

Cons:

- Higher initial premiums

- Premiums may increase as coverage grows

- Not widely available

The 3 Types of Whole Life Insurance

Whole life insurance also comes in different varieties, each with unique features and benefits.

1. Traditional Whole Life Insurance (Most Common)

What it is: The classic whole life policy with fixed premiums, guaranteed death benefit, and guaranteed cash value growth.

Best for: Seniors who want maximum guarantees and predictable growth.

How it works:

- Premiums remain level for life

- Cash value grows at a guaranteed minimum rate

- Death benefit is guaranteed from day one

- May pay dividends (with participating policies)

Example: Margaret, age 60, buys a $50,000 traditional whole life policy for $245/month. Her premiums never change, her death benefit is guaranteed at $50,000, and her cash value grows at a guaranteed 2-3% annually.

Pros:

- Maximum guarantees

- Predictable premiums and growth

- Simple to understand

Cons:

- Higher premiums than other types

- Lower potential returns than universal life

- Less flexibility

2. Single Premium Whole Life Insurance

What it is: You pay one large lump sum upfront, and you’re covered for life with no further premiums.

Best for: Seniors with significant savings who want to convert cash into a tax-advantaged death benefit.

How it works:

- One payment (typically $5,000-$100,000+) purchases lifetime coverage

- Death benefit is usually 2-3 times the premium amount

- Immediate cash value equal to your premium

- No ongoing payments required

Example: Barbara, age 70, pays $25,000 in a single premium and receives $52,000 in death benefit coverage. Her $25,000 is now worth $52,000 to her heirs—a 108% increase that passes tax-free.

Pros:

- No ongoing premiums

- Immediate coverage and cash value

- Leverages money for larger death benefit

- Great for estate planning

Cons:

- Requires significant upfront cash

- May be classified as Modified Endowment Contract (MEC) with tax implications on withdrawals

- Less flexibility once purchased

3. Final Expense / Burial Insurance (Simplified Whole Life)

What it is: Final Expense Insurance are small whole life policies ($5,000-$25,000) designed specifically to cover funeral costs and end-of-life expenses. Often available with no medical exam.

Best for: Seniors who want guaranteed acceptance coverage for funeral expenses without burdening their family.

How it works:

- Coverage amounts typically $5,000-$25,000

- Simplified underwriting (health questions only, no medical exam)

- Some policies offer guaranteed acceptance regardless of health

- Permanent coverage that never expires

- May have a 2-year graded death benefit period for guaranteed issue policies

Example: William, age 75 with diabetes, buys a $15,000 final expense policy for $89/month. No medical exam required. His policy covers his funeral costs and leaves a small legacy for his grandchildren.

Pros:

- Easy qualification

- No medical exam required

- Affordable small coverage amounts

- Available at older ages (up to 85+)

Cons:

- Limited coverage amounts

- Higher cost per $1,000 of coverage than larger policies

- Graded benefit policies have waiting periods

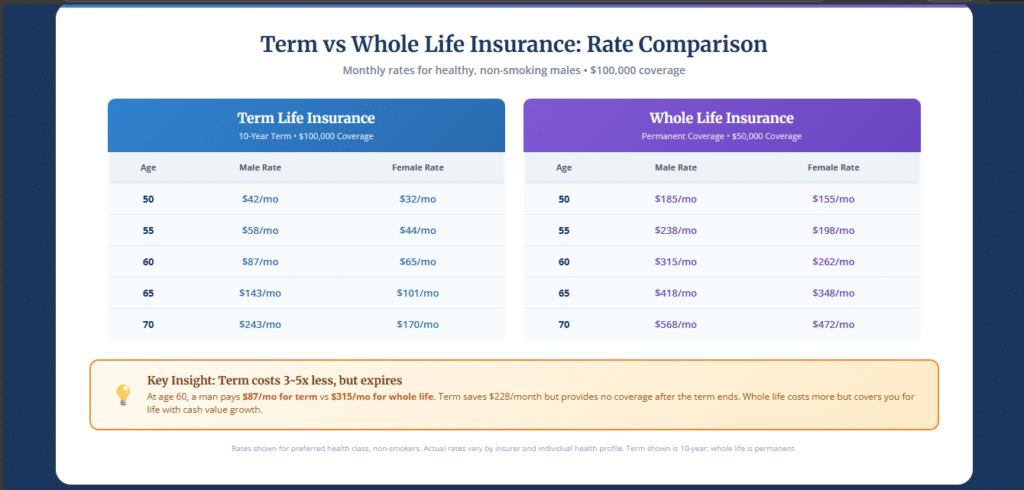

Term Life Insurance Rates for Seniors

Understanding what you’ll actually pay helps you budget and compare options. Here are current average rates for healthy, non-smoking seniors.

10-Year Term Life Insurance Rates ($100,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate | Annual Cost Range |

|---|---|---|---|

| 50 | $42 | $32 | $384 – $504 |

| 55 | $58 | $44 | $528 – $696 |

| 60 | $87 | $65 | $780 – $1,044 |

| 65 | $143 | $101 | $1,212 – $1,716 |

| 70 | $243 | $170 | $2,040 – $2,916 |

10-Year Term Life Insurance Rates ($250,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate |

|---|---|---|

| 50 | $78 | $58 |

| 55 | $115 | $85 |

| 60 | $185 | $138 |

| 65 | $315 | $225 |

| 70 | $565 | $398 |

20-Year Term Life Insurance Rates ($100,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate |

|---|---|---|

| 50 | $58 | $45 |

| 55 | $89 | $67 |

| 60 | $145 | $108 |

| 65 | $248 | $178 |

| 70 | Limited availability | Limited availability |

Note: 20-year terms are often not available for seniors over 65-70 due to age restrictions.

Key takeaway: Term life insurance rates increase approximately 8-12% for each year you wait. A 60-year-old pays roughly 50% more than a 55-year-old for the same coverage.

Whole Life Insurance Rates for Seniors

Whole life insurance costs significantly more than term because it covers you for life and includes cash value accumulation.

Traditional Whole Life Insurance Rates ($25,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate | Annual Cost |

|---|---|---|---|

| 50 | $98 | $82 | $984 – $1,176 |

| 55 | $125 | $105 | $1,260 – $1,500 |

| 60 | $165 | $138 | $1,656 – $1,980 |

| 65 | $218 | $182 | $2,184 – $2,616 |

| 70 | $295 | $245 | $2,940 – $3,540 |

| 75 | $398 | $328 | $3,936 – $4,776 |

Traditional Whole Life Insurance Rates ($50,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate |

|---|---|---|

| 50 | $185 | $155 |

| 55 | $238 | $198 |

| 60 | $315 | $262 |

| 65 | $418 | $348 |

| 70 | $568 | $472 |

| 75 | $765 | $635 |

Final Expense / Burial Insurance Rates ($10,000 Coverage)

| Age | Male Monthly Rate | Female Monthly Rate |

|---|---|---|

| 50 | $38 | $32 |

| 55 | $48 | $40 |

| 60 | $62 | $52 |

| 65 | $82 | $68 |

| 70 | $108 | $89 |

| 75 | $145 | $118 |

| 80 | $198 | $162 |

Note: These rates are for healthy non-smokers in preferred or standard health classes. Rates vary significantly based on health conditions, tobacco use, and the specific insurance company.

Term Life vs Whole Life Insurance: Key Differences

Now that you understand both types, let’s compare them directly.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Period | Specific term (10-30 years) | Entire lifetime |

| Premium Cost | Lower (5-10x cheaper) | Higher |

| Premium Changes | Fixed during term | Fixed for life |

| Cash Value | None | Yes, grows over time |

| Death Benefit | Fixed | Fixed or increasing |

| Flexibility | Limited | Can borrow/withdraw cash value |

| Best For | Temporary needs, budget-conscious | Permanent needs, estate planning |

| Complexity | Simple | More complex |

| Investment Component | No | Yes |

| Available Ages | Up to 75-80 | Up to 85+ |

Cost Comparison Example

Let’s compare what a 60-year-old male would pay for $100,000 of coverage:

Term Life (20-Year):

- Monthly premium: $145

- Total paid over 20 years: $34,800

- Cash value at end: $0

- Coverage at age 80: None (policy expired)

Whole Life:

- Monthly premium: $485

- Total paid over 20 years: $116,400

- Cash value at age 80: ~$45,000

- Coverage at age 80: $100,000 (still active)

The difference: Whole life costs $81,600 more over 20 years, but you have $45,000 in accessible cash value and permanent $100,000 coverage. Term life saves money but leaves you without coverage at age 80.

How to Choose: Term Life vs Whole Life for Seniors

Use this decision framework to determine which type is the right life insurance for seniors.

Choose Term Life Insurance If:

✓ You need coverage for a specific period (mortgage payoff, until spouse reaches retirement age, etc.)

✓ You’re on a limited budget and need maximum coverage for the lowest cost

✓ You have other retirement savings and investments

✓ You don’t need cash value accumulation

✓ You want the simplest possible policy

✓ You’re primarily concerned with income replacement or debt protection

✓ You’re under 70 and can qualify for competitive rates

Choose Whole Life Insurance If:

✓ You want coverage that lasts your entire life, no matter how long you live

✓ You need guaranteed final expense coverage for funeral costs

✓ You want to build cash value you can access in emergencies

✓ You’re using life insurance as part of an estate plan

✓ You want fixed premiums that will never increase

✓ You’ve been declined for term insurance due to health issues

✓ You want to leave a guaranteed inheritance for your heirs

Consider Both (Hybrid Approach) If:

✓ You have both temporary and permanent insurance needs

✓ You want maximum coverage now with some guaranteed coverage forever

Example hybrid strategy: A 60-year-old buys a $200,000, 15-year term policy ($175/month) to cover their mortgage and provide income replacement, PLUS a $25,000 whole life policy ($165/month) to permanently cover final expenses. Total: $340/month for $225,000 of coverage with $25,000 guaranteed for life.

Common Mistakes to Avoid

Mistake #1: Buying Only Term Life and Having No Coverage at 75+

Many seniors buy 20-year term policies in their 50s, then have no coverage at age 70+ when they actually need it. If you go this route, consider also purchasing a small whole life policy for final expenses.

Mistake #2: Buying Whole Life When Term Would Suffice

If you just need to cover a mortgage for 15 more years, whole life insurance is overkill. You’ll pay 3-5 times more for coverage you don’t need permanently.

Mistake #3: Not Shopping Multiple Companies

Rates vary 30-50% between insurance companies for the exact same coverage. Always get at least 3-5 quotes before buying.

Mistake #4: Waiting Too Long to Apply

Every year you wait, premiums increase 8-12%. A 60-year-old pays significantly more than a 58-year-old. If you need coverage, apply now.

Mistake #5: Letting Health Conditions Stop You

Many seniors assume they can’t get coverage due to diabetes, heart disease, or other conditions. In reality, many companies specialize in covering seniors with health issues. Work with an independent agent who can shop multiple carriers.

Frequently Asked Questions

Is term or whole life insurance better for seniors?

It depends on your specific needs. Term life insurance is better if you need temporary coverage at the lowest cost—like protecting a mortgage or providing income replacement for a specific period. Whole life insurance is better if you need permanent coverage that lasts your entire life, want to build cash value, or need guaranteed final expense coverage. Many seniors benefit from a combination of both.

Can I get term life insurance at age 70?

Yes, but your options become more limited. Most insurance companies offer 10-year term policies to age 70-75. Longer terms (20-30 years) are typically not available past age 65. At 70+, you may want to consider guaranteed universal life or whole life insurance for permanent coverage.

Is whole life insurance worth it for seniors over 60?

Whole life insurance can be worth it for seniors over 60 who want guaranteed lifetime coverage, need final expense protection, or want to leave a guaranteed inheritance. It’s particularly valuable if you’re concerned about outliving a term policy or want the cash value component. However, if you only need temporary coverage, term life remains more cost-effective.

What happens when my term life insurance expires?

When your term expires, you typically have three options: (1) Let the coverage end if you no longer need it, (2) Renew year-to-year at significantly higher rates, or (3) Convert to a permanent whole life policy without a medical exam if your policy includes a conversion rider. Option 3 is valuable if your health has declined since you originally purchased the policy.

How much life insurance do seniors actually need?

Most financial advisors recommend coverage of 5-10 times your annual income, but seniors often have different needs. Consider: final expenses ($10,000-$25,000), outstanding debts (mortgage, car loans), income replacement for a surviving spouse (3-5 years of expenses), and any legacy you want to leave. Many seniors find $50,000-$250,000 provides adequate protection.

Can I have both term and whole life insurance at the same time?

Absolutely. Many seniors use a “laddering” strategy with both types. For example, you might carry a $200,000 term policy to cover your mortgage and income replacement needs, plus a $25,000 whole life policy to guarantee final expense coverage forever. This gives you maximum flexibility at a reasonable cost.

Is whole life insurance a good investment for seniors?

Whole life insurance should not be viewed primarily as an investment—it’s life insurance first. The cash value grows slowly (typically 2-4% annually), which is lower than many other investment options. However, the cash value grows tax-deferred, and the death benefit passes to beneficiaries tax-free. For seniors who want guaranteed growth with no market risk, the cash value component can be a conservative part of an overall financial plan.

What is the best age to buy whole life insurance?

The best age is as young as possible, since premiums are based on your age at purchase and remain fixed for life. However, if you’re 50, 60, or even 70, you can still benefit from whole life insurance—you’ll just pay more than if you’d purchased it earlier. The second-best time to buy is today, as premiums only increase with age.

Do I need a medical exam for life insurance after 60?

Not necessarily. Many term and whole life policies are available with no medical exam (simplified issue). Final expense and burial insurance almost never require exams. However, policies with medical exams typically offer 20-40% lower premiums. If you’re in good health, taking the exam can save you significant money over the life of the policy.

Can seniors with pre-existing conditions get life insurance?

Yes, seniors can qualify for life insurance with pre-existing conditions. Many insurance companies specialize in covering seniors with conditions like diabetes, heart disease, COPD, cancer history, and more. Guaranteed issue whole life policies accept everyone regardless of health (though they may have graded benefit periods). Work with an independent agent who can shop multiple carriers to find the best rates for your specific pre-existing condition.

Taking the Next Step

Choosing between term life insurance and whole life insurance is a personal decision that depends on your unique financial situation, health, age, and goals. Here’s a quick summary:

Choose Term Life If: You need affordable, temporary coverage for a specific period and have other savings for retirement and final expenses.

Choose Whole Life If: You want guaranteed permanent coverage, cash value accumulation, or need to ensure final expenses are always covered.

Consider Both If: You have both temporary needs (mortgage, income replacement) and permanent needs (final expenses, inheritance).

The most important step is taking action. Every year you wait, premiums increase 8-12%, and your health may change. Request quotes from multiple insurance companies, compare your options, and secure the coverage your family needs.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Life insurance rates vary based on individual factors including age, health, tobacco use, and the insurance company. The rates shown are estimates for healthy, non-smoking individuals and may not reflect your actual costs. Always consult with a licensed insurance professional before purchasing any life insurance policy. Policies and rates may have changed since publication.