Guaranteed Issue vs Simplified Issue Life Insurance-2026 Guide

Posted in Senior Life Insurance on January 7, 2026 last updated on June 2, 2026

Posted in Senior Life Insurance on January 7, 2026 last updated on June 2, 2026

Choosing life insurance as a senior can feel confusing, frustrating, and sometimes discouraging—especially if health issues have made traditional policies difficult or impossible to obtain. That’s why understanding guaranteed issue vs simplified issue life insurance for seniors is so important.

Both options eliminate the need for a medical exam, making them attractive to older adults. However, they differ significantly in cost, coverage amount, approval requirements, waiting periods, and long-term value. Choosing the wrong one can result in overpaying for limited coverage or being declined when approval certainty is critical.

This guide walks you through everything you need to know so you can make a confident, informed decision.

Why Seniors Often Choose No-Medical-Exam Life Insurance

Many seniors turn to guaranteed issue or simplified issue life insurance because:

- Medical exams feel invasive or stressful

- Health conditions limit traditional eligibility

- Coverage is needed quickly

- They want predictable premiums

- They want to protect family from final expenses

No-exam life insurance removes many barriers—but not all policies are created equal.

What Is Simplified Issue Life Insurance for Seniors?

Simplified issue life insurance is designed for seniors who want faster approval without undergoing a medical exam but are still willing to answer basic health questions.

Instead of lab work or doctor visits, insurers rely on:

- Yes/no health questions

- Prescription history checks

- Database reviews

Key Features of Simplified Issue Life Insurance

- No medical exam

- Health questionnaire required

- Approval in days (sometimes same day)

- Higher coverage limits than guaranteed issue

- Lower premiums than guaranteed issue

- Available as whole life or term life

This option rewards relatively stable health—even with conditions like diabetes or high blood pressure—by offering better pricing and more coverage.

Who Simplified Issue Life Insurance Is Best For

Simplified issue life insurance for seniors works best if you:

- Are generally stable health-wise

- Manage chronic conditions with medication

- Want coverage above final expenses

- Want lifetime coverage without exams

- Prefer lower premiums than guaranteed issue

Many seniors who assume they’ll be declined are surprised to qualify for simplified issue policies.

What Is Guaranteed Issue Life Insurance for Seniors?

Guaranteed issue life insurance offers approval with no health questions and no medical exam. If you meet the age requirements, you are approved—period.

This makes it the final safety net for seniors who cannot qualify for any other type of life insurance.

Key Features of Guaranteed Issue Life Insurance

- Guaranteed approval

- No health questions

- No medical exam

- Lower coverage limits

- Higher premiums

- Waiting period before full payout

Guaranteed issue policies are usually whole life insurance designed to cover final expenses only.

Who Guaranteed Issue Life Insurance Is Best For

Guaranteed issue life insurance for seniors is best if you:

- Have serious or multiple health conditions

- Were declined for simplified issue or traditional coverage

- Need guaranteed approval

- Want coverage strictly for funeral costs

- Are comfortable with smaller death benefits

While more expensive per dollar of coverage, guaranteed issue policies provide certainty when no other option exists.

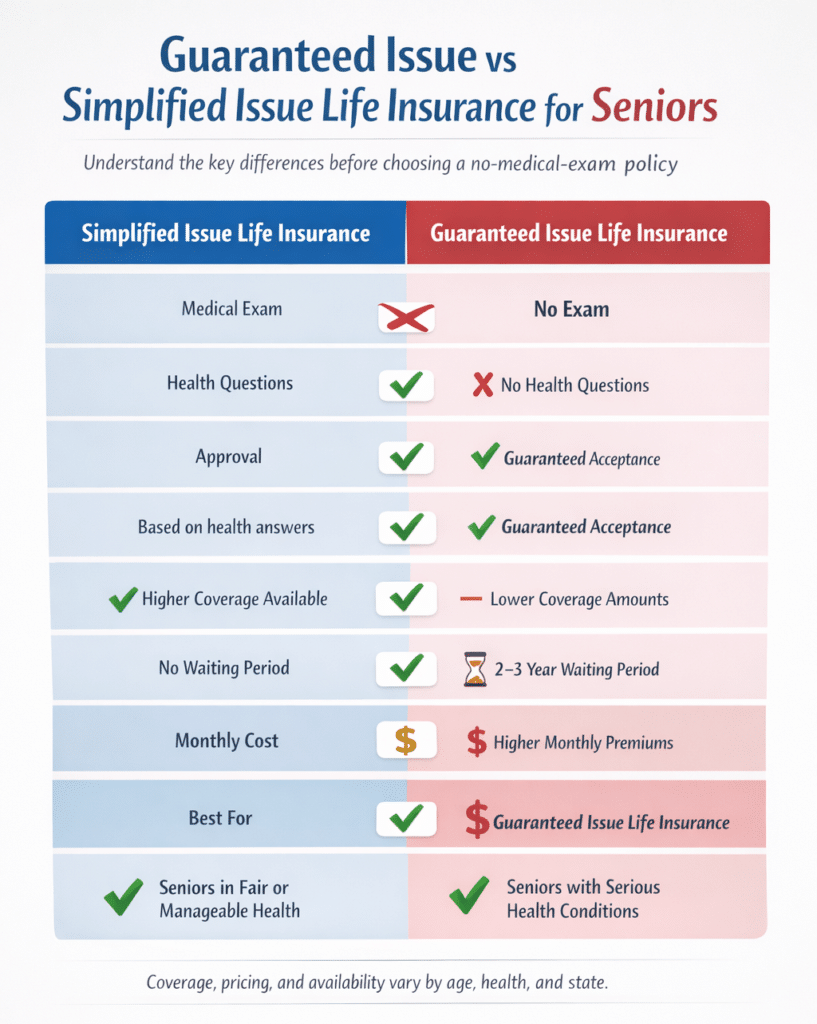

Guaranteed Issue vs Simplified Issue Life Insurance: Detailed Comparison

| Feature | Simplified Issue | Guaranteed Issue |

|---|---|---|

| Medical exam | ❌ | ❌ |

| Health questions | ✔️ | ❌ |

| Approval certainty | Moderate | Guaranteed |

| Coverage amounts | $25,000–$300,000+ | $5,000–$25,000 |

| Waiting period | None | Usually 2–3 years |

| Cost | Moderate | Higher |

| Policy type | Term or whole life | Whole life only |

| Best use | Family protection, legacy | Final expenses |

Guaranteed Issue vs Simplified Issue Life Insurance for Seniors with Multiple Health Conditions

Many seniors are not dealing with a single diagnosis.

Common combinations include:

- Diabetes and high blood pressure

- Heart disease and high cholesterol

- COPD and smoking history

- Sleep apnea and obesity

- Stroke history and past heart attacks

In many cases, seniors with stable, well-managed conditions still qualify for simplified issue life insurance.

However, applicants with severe medical histories, recent hospitalizations, oxygen use, advanced heart disease, or multiple serious conditions may find guaranteed issue life insurance to be the more realistic option.

Because underwriting guidelines vary from one company to another, comparing multiple insurers is often the best way to determine which policy type makes the most sense.

Understanding Waiting Periods (Critical Difference)

One of the most misunderstood differences in guaranteed issue vs simplified issue life insurance for seniors is the waiting period.

Simplified Issue Waiting Period

- Typically none

- Full death benefit paid immediately upon approval

Guaranteed Issue Waiting Period

- Usually 2–3 years

- If death occurs during waiting period:

- Premiums are refunded

- Plus interest (varies by insurer)

This waiting period is the tradeoff for guaranteed acceptance.

Average Monthly Rate Charts (2026 Estimates)

We have comprised some average life insurance rates for you to review.

| Age | Simplified Issue $25,000 | Guaranteed Issue $25,000 |

|---|---|---|

| 60 | $55–$75 | $95–$140 |

| 65 | $75–$95 | $120–$175 |

| 70 | $95–$120 | $150–$225 |

| 75 | $120–$150 | $190–$285 |

Key takeaway: Simplified issue coverage is often substantially less expensive than guaranteed issue coverage when an applicant qualifies. These are averages for non-smokers. Health, gender, and state will affect pricing.

Best Simplified Issue Life Insurance Companies for Seniors

These companies are well-known for competitive pricing, solid underwriting, and strong senior programs:

- Mutual of Omaha – Excellent simplified underwriting for seniors

- AIG (Corebridge Financial) – Strong whole life options

- Fidelity Life – High coverage limits with simplified approval

- Royal Neighbors of America – Popular for senior-friendly policies

- Foresters Financial – Member benefits and simplified underwriting

Simplified issue policies vary significantly by company, making comparisons essential.

Best Guaranteed Issue Life Insurance Companies

These insurers are widely recognized for reliable guaranteed issue coverage:

- Mutual of Omaha – Industry leader in guaranteed issue

- AIG – Strong brand and policy clarity

- AMERICO – Affordable final expense solutions

- Gerber Life – Simple, widely accessible coverage

- Transamerica – Competitive guaranteed issue options

These policies prioritize approval certainty and stability.

What If You’ve Been Denied Life Insurance?

Many seniors assume a life insurance denial means coverage is no longer possible.

That is often not the case.

Applicants who are declined for traditional life insurance frequently explore:

In many situations, guaranteed issue coverage provides a path to protection even after multiple insurance denials.

The key is understanding which options remain available and choosing a policy that fits your health profile and financial goals.

Real-Life Experiences

Linda, Age 68 – Simplified Issue Success

Linda had high blood pressure and arthritis and assumed life insurance was no longer an option. After answering a short health questionnaire, she qualified for a simplified issue whole life policy with $50,000 in coverage. Approval came within two days, and the premiums fit her fixed retirement income.

Robert, Age 79 – Guaranteed Issue Peace of Mind

Robert had heart failure and COPD and was declined elsewhere. A guaranteed issue life insurance policy gave him immediate approval. While the coverage amount was modest and included a waiting period, it ensured his children wouldn’t face funeral expenses alone.

These experiences highlight why understanding your options matters.

Common Mistakes Seniors Make

- Choosing guaranteed issue too early

- Overpaying for coverage they don’t need

- Underestimating simplified issue eligibility

- Ignoring waiting periods

- Not comparing companies

Avoiding these mistakes can save thousands over time.

Frequently Asked Questions

Is simplified issue better than guaranteed issue life insurance?

Simplified issue is usually better if you qualify because it offers higher coverage, lower premiums, and no waiting period.

Can I be declined for simplified issue life insurance?

Yes. Approval depends on health answers, but many seniors still qualify even with chronic conditions.

Is guaranteed issue life insurance worth it?

Yes, when it’s your only option and you need guaranteed acceptance for final expenses.

Can these policies be canceled?

Yes. Both are permanent policies that can be canceled at any time.

No. Premiums are fixed for life in both policy types.

Is Guaranteed Issue or Simplified Issue Better for Seniors with Health Problems?

Many seniors with manageable health conditions still qualify for simplified issue life insurance, which often offers lower premiums and higher coverage amounts. Seniors with severe medical conditions or previous denials may find guaranteed issue life insurance to be the better option because approval is guaranteed regardless of health history.

Which Policy Costs Less: Guaranteed Issue or Simplified Issue?

In most cases, simplified issue life insurance costs significantly less than guaranteed issue life insurance. Because insurers evaluate health information during the application process, they can often offer higher coverage amounts and lower premiums to qualified applicants. Guaranteed issue policies typically have higher costs because approval is guaranteed regardless of health history.

Which Policy Should You Choose?

The best choice depends on your health, budget, and coverage goals.

Choose Simplified Issue Life Insurance If:

- You can answer health questions honestly

- Your health conditions are stable

- You want higher coverage amounts

- You want lower monthly premiums

- You want immediate full coverage without a waiting period

Many seniors with diabetes, high blood pressure, sleep apnea, or controlled heart conditions qualify for simplified issue life insurance and may be surprised by how affordable coverage can be.

Choose Guaranteed Issue Life Insurance If:

- You have been declined for other policies

- You have serious or multiple health conditions

- You need guaranteed approval

- You only need coverage for funeral expenses

- You are comfortable with a waiting period

Guaranteed issue life insurance often serves as a valuable safety net for seniors who have limited alternatives.

Quick Verdict

Choose Simplified Issue Life Insurance if:

✓ You can qualify medically

✓ You want lower premiums

✓ You need higher coverage amounts

✓ You want immediate coverage

Choose Guaranteed Issue Life Insurance if:

✓ You’ve been declined elsewhere

✓ You have serious health conditions

✓ You need guaranteed approval

✓ You only need funeral expense coverage

Final Thoughts

Choosing between guaranteed issue vs simplified issue life insurance for seniors comes down to health, budget, and coverage goals. Simplified issue policies offer better value when you qualify, while guaranteed issue policies provide certainty when no other options exist.

Understanding the differences—especially waiting periods, costs, and coverage limits—ensures you choose protection that truly supports your family when it matters most.