10-Year vs 20-Year Term Life Insurance: What Seniors Should Choose

Posted in Types of Life Insurance on December 17, 2025 last updated on December 17, 2025

Posted in Types of Life Insurance on December 17, 2025 last updated on December 17, 2025

Choosing between a 10-year vs 20-year term life insurance policy is one of the most important decisions seniors face when shopping for coverage. The right choice depends on your age, your financial obligations, and how long you need protection.

Get it right, and you’ll have affordable coverage that lasts exactly as long as you need it. Get it wrong, and you could pay for coverage you don’t need—or worse, find yourself without protection when you need it most.

In this comprehensive guide, we’ll compare 10-year vs 20-year term life insurance for seniors, show you real rates at every age, and give you a clear framework for making the best decision for your situation.

In This Guide:

- 10-year vs 20-year term: Key differences

- Current rates by age for both term lengths

- Which term length is best at each age

- Types of term and whole life insurance available

- Real-world examples and scenarios

- How to decide which term is right for you

- Frequently asked questions

The Quick Answer: 10-Year vs 20-Year Term Life Insurance

Before we dive deep, here’s a quick comparison:

| Factor | 10-Year Term | 20-Year Term |

|---|---|---|

| Monthly Cost | Lower (30-40% less) | Higher |

| Coverage Period | 10 years | 20 years |

| Best Ages | 60-75 | 50-65 |

| Availability | Up to age 75-80 | Up to age 60-65 |

| Best For | Short-term needs, older seniors | Long-term needs, younger seniors |

| Flexibility | Expires sooner | Longer protection window |

General Rule:

- Ages 50-60: 20-year term is usually the better choice

- Ages 60-70: 10-year term is often more practical

- Ages 70+: 10-year term may be your only option

Understanding Term Life Insurance for Seniors

Before comparing term lengths, let’s make sure we understand how term life insurance for seniors works.

What Is Term Life Insurance?

Term life insurance provides coverage for a specific period (the “term”). If you die during that term, your beneficiaries receive the death benefit. If you outlive the term, coverage ends and you receive nothing back (unless you have a return of premium policy).

How Term Life Insurance Works for Seniors

- You choose a coverage amount (death benefit): $50,000 to $500,000+

- You select a term length: 10, 15, 20, or 30 years

- You pay fixed monthly premiums that never increase during the term

- If you die during the term: Beneficiaries receive the full tax-free death benefit

- If you outlive the term: Coverage ends (with options to renew or convert)

Why Term Length Matters

The term length you choose affects:

- Your monthly premium: Longer terms cost more

- How long you’re protected: Shorter terms expire sooner

- Your options at the end: What happens when coverage expires

- Your availability: Longer terms may not be available at older ages

10-Year Term Life Insurance: Pros, Cons, and Best Uses

A 10-year term policy provides coverage for exactly one decade. It’s the most affordable term length and the most widely available for seniors.

Pros of 10-Year Term Life Insurance

✓ Lowest premiums: 30-40% cheaper than 20-year term for the same coverage

✓ Widely available: Most companies offer 10-year terms up to age 75-80

✓ Perfect for specific needs: Ideal when you know exactly how long you need coverage

✓ Lower total cost: Pay premiums for only 10 years instead of 20

✓ Easier to qualify: Underwriting may be more lenient for shorter terms

Cons of 10-Year Term Life Insurance

✗ Coverage ends sooner: You’re unprotected after 10 years

✗ Renewal is expensive: Renewing at age 70+ costs significantly more

✗ May outlive your coverage: If your needs extend beyond 10 years, you’re stuck

✗ Less flexibility: Harder to extend if circumstances change

Best Uses for 10-Year Term

A 10-year term makes sense when:

- You’re 65-75 years old: 20-year terms may not be available or affordable

- Your mortgage has 10 years or less remaining: Match coverage to your debt

- You need coverage until a specific age: Like until your spouse turns 65 and qualifies for Medicare

- You’re covering a specific financial obligation: Business loan, helping adult children, etc.

- You want the lowest possible premium: Budget is a primary concern

- You have other coverage for later: Whole life policy for final expenses after term expires

10-Year Term Availability by Age

| Your Age | 10-Year Term | Policy Expires At |

|---|---|---|

| 50 | ✅ Widely available | Age 60 |

| 55 | ✅ Widely available | Age 65 |

| 60 | ✅ Widely available | Age 70 |

| 65 | ✅ Available | Age 75 |

| 70 | ✅ Available (limited) | Age 80 |

| 75 | ⚠️ Limited availability | Age 85 |

| 80 | ❌ Rarely available | N/A |

20-Year Term Life Insurance: Pros, Cons, and Best Uses

A 20-year term policy provides coverage for two full decades. It costs more than a 10-year term but offers longer protection.

Pros of 20-Year Term Life Insurance

✓ Longer protection: Coverage lasts twice as long as a 10-year term

✓ Locked-in rates: Premiums stay fixed for 20 full years

✓ More flexibility: Better if your needs might extend beyond 10 years

✓ Better value long-term: If you need 15+ years of coverage, 20-year is often cheaper than buying two consecutive 10-year policies

✓ Peace of mind: Don’t have to worry about reapplying in 10 years when you’re older and possibly less healthy

Cons of 20-Year Term Life Insurance

✗ Higher monthly premiums: 30-40% more expensive than 10-year term

✗ Limited availability for seniors: Most companies cap 20-year terms at age 60-65

✗ May pay for coverage you don’t need: If your obligations end before 20 years

✗ Harder to qualify: More stringent underwriting for longer terms

✗ Higher total cost: More premium payments over the life of the policy

Best Uses for 20-Year Term

A 20-year term makes sense when:

- You’re 50-60 years old: Still young enough to qualify and get good rates

- Your mortgage has 15-20 years remaining: Match coverage to your debt

- You want income replacement for your spouse: Provide security for two decades

- You’re uncertain about future needs: Prefer the safety of longer coverage

- You want to avoid reapplying at an older age: Lock in coverage now while healthy

- Your health might decline: Secure long-term coverage while you can qualify

20-Year Term Availability by Age

| Your Age | 20-Year Term | Policy Expires At |

|---|---|---|

| 50 | ✅ Widely available | Age 70 |

| 55 | ✅ Widely available | Age 75 |

| 60 | ✅ Available | Age 80 |

| 65 | ⚠️ Limited availability | Age 85 |

| 70 | ❌ Rarely available | N/A |

| 75 | ❌ Not available | N/A |

Term Life Insurance Rates: 10-Year vs 20-Year Comparison

Understanding the cost difference helps you make an informed decision. Here are current rates for healthy, non-smoking seniors.

10-Year Term Life Insurance Rates

$100,000 Coverage – 10-Year Term

| Age | Male Monthly | Female Monthly | Annual Cost |

|---|---|---|---|

| 50 | $42 | $32 | $384 – $504 |

| 55 | $58 | $44 | $528 – $696 |

| 60 | $87 | $65 | $780 – $1,044 |

| 65 | $143 | $101 | $1,212 – $1,716 |

| 70 | $243 | $170 | $2,040 – $2,916 |

| 75 | $425 | $298 | $3,576 – $5,100 |

$250,000 Coverage – 10-Year Term

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $78 | $58 |

| 55 | $115 | $85 |

| 60 | $185 | $138 |

| 65 | $315 | $225 |

| 70 | $565 | $398 |

20-Year Term Life Insurance Rates

$100,000 Coverage – 20-Year Term

| Age | Male Monthly | Female Monthly | Annual Cost |

|---|---|---|---|

| 50 | $58 | $45 | $540 – $696 |

| 55 | $89 | $67 | $804 – $1,068 |

| 60 | $145 | $108 | $1,296 – $1,740 |

| 65 | $248 | $178 | $2,136 – $2,976 |

$250,000 Coverage – 20-Year Term

| Age | Male Monthly | Female Monthly |

|---|---|---|

| 50 | $118 | $88 |

| 55 | $185 | $138 |

| 60 | $318 | $238 |

| 65 | $565 | $408 |

Cost Comparison: 10-Year vs 20-Year

Let’s compare the total cost for a 60-year-old male with $100,000 coverage:

10-Year Term:

- Monthly premium: $87

- Total cost over 10 years: $10,440

- Coverage ends at age 70

20-Year Term:

- Monthly premium: $145

- Total cost over 20 years: $34,800

- Coverage ends at age 80

The 20-year term costs $24,360 more but provides coverage for an additional 10 years (ages 70-80).

If you only need 10 years of coverage: The 10-year term saves you significant money.

If you need 20 years of coverage: The 20-year term is cheaper than buying two consecutive 10-year policies (the second policy at age 70 would be extremely expensive).

What Happens When Your Term Expires?

Understanding your options at the end of the term is crucial for planning.

Option 1: Let Coverage Expire

If you no longer need life insurance (mortgage paid off, spouse has sufficient retirement income, children are independent), you can simply let the policy expire. You stop paying premiums and coverage ends.

Option 2: Renew Year-to-Year (Annual Renewable)

Most term policies allow you to renew annually without a medical exam after the initial term expires. However, premiums increase significantly each year based on your current age.

Example: A 60-year-old with a 10-year term paying $87/month would see renewal rates at age 70 jump to $400-600+/month for the same coverage.

Option 3: Convert to Permanent Insurance

Many term policies include a “conversion privilege” that allows you to convert to a permanent whole life policy without a medical exam. This is valuable if your health has declined since you originally purchased the policy.

Conversion deadlines vary: Some policies allow conversion anytime during the term; others only during the first 5-10 years. Check your policy details.

Option 4: Purchase a New Policy

You can apply for a new term policy, but you’ll face:

- Higher premiums due to older age

- New medical underwriting (health questions, possible exam)

- Potential denial if health has declined

Types of Term Life Insurance for Seniors

Beyond just the term length, you have several types of term insurance to choose from.

1. Level Term Life Insurance (Most Common)

What it is: Fixed premium and death benefit for the entire term.

Best for: Most seniors—simple, predictable, and best value.

Available terms: 10, 15, 20, 25, 30 years (shorter terms more available for seniors)

2. Annual Renewable Term (ART)

What it is: One-year term that automatically renews each year. Premiums start low but increase annually.

Best for: Short-term needs (1-5 years), uncertain coverage duration.

Pros: No long-term commitment, easy to cancel Cons: Becomes very expensive over time

3. Decreasing Term Life Insurance

What it is: Death benefit decreases over time while premium stays level. Often called “mortgage protection insurance.”

Best for: Covering a mortgage or debt that decreases over time.

Pros: 20-40% cheaper than level term Cons: Coverage decreases even if your needs don’t

4. Return of Premium (ROP) Term

What it is: If you outlive the term, you get all your premiums back.

Best for: Those who don’t want to “lose” money if they survive the term.

Pros: Get your money back if you live Cons: Premiums are 2-4x higher than regular term

When to Consider Whole Life Instead

Sometimes, neither 10-year nor 20-year term is the right answer. Here’s when whole life insurance might be better for seniors. Check out our article on term life vs whole life insurance.

Consider Whole Life Insurance If:

✓ You’re over 70: Term insurance becomes very expensive or unavailable

✓ You want permanent coverage: Protection that never expires

✓ You need final expense coverage: Guaranteed funeral cost protection

✓ You’ve been declined for term: Health issues prevent term approval

✓ You want cash value accumulation: Build equity in your policy

✓ You’re concerned about outliving term coverage: Want certainty

Types of Whole Life Insurance for Seniors

1. Traditional Whole Life

- Permanent coverage, fixed premiums, cash value growth

- Best for: Maximum guarantees and predictability

- Cost: $165-$500+/month for $25,000-$100,000 coverage at age 60

2. Guaranteed Universal Life (GUL)

- Permanent coverage with lower premiums, minimal cash value

- Best for: Affordable lifetime coverage

- Cost: 20-30% less than traditional whole life

3. Final Expense / Burial Insurance

- Small policies ($5,000-$25,000) for funeral costs

- Best for: Guaranteed final expense coverage

- Cost: $50-$150/month for $10,000-$25,000 coverage

4. Simplified/Guaranteed Issue Whole Life

- No medical exam, guaranteed acceptance options

- Best for: Seniors with health issues

- Cost: Higher than medically underwritten policies

Whole Life Rates for Comparison

Whole Life Insurance at Age 60 (for comparison)

| Coverage | Male Monthly | Female Monthly | Type |

|---|---|---|---|

| $10,000 | $62 | $52 | Final Expense |

| $25,000 | $138 | $115 | Final Expense |

| $50,000 | $262 | $218 | Traditional |

| $100,000 | $498 | $415 | Traditional |

Key Insight: A $25,000 whole life policy at $138/month provides permanent coverage. Compare this to a 10-year, $100,000 term at $87/month that expires. Many seniors benefit from combining both: term for temporary needs, whole life for permanent final expense coverage.

How to Choose: Decision Framework for Seniors

Use this framework to decide between 10-year and 20-year term (or whether whole life is better).

Step 1: Determine How Long You Need Coverage

Ask yourself:

- How many years until my mortgage is paid off?

- How many years until my spouse reaches full retirement age?

- How many years until my children are financially independent?

- Do I have any debts with specific payoff timelines?

- Do I need permanent coverage for final expenses?

If your answer is 10 years or less → 10-year term If your answer is 11-20 years → 20-year term If your answer is “forever” or “I’m not sure” → Consider whole life

Step 2: Check Availability at Your Age

| Your Age | 10-Year Term | 20-Year Term | Recommendation |

|---|---|---|---|

| 50-55 | ✅ Available | ✅ Available | Either—based on needs |

| 56-60 | ✅ Available | ✅ Available | 20-year if you need 15+ years |

| 61-65 | ✅ Available | ⚠️ Limited | 10-year + whole life combo |

| 66-70 | ✅ Available | ❌ Unlikely | 10-year term |

| 71-75 | ⚠️ Limited | ❌ Not available | 10-year or whole life only |

Step 3: Compare Total Costs

Calculate the total cost for your coverage period:

Example: 55-year-old needing coverage to age 75

Option A: 20-year term

- $89/month × 240 months = $21,360 total

Option B: Two consecutive 10-year terms

- First 10-year (age 55-65): $58/month × 120 = $6,960

- Second 10-year (age 65-75): $143/month × 120 = $17,160

- Total: $24,120

Result: The single 20-year term saves $2,760 AND you don’t have to requalify medically at age 65.

Step 4: Consider the Hybrid Approach

Many financial advisors recommend combining term and whole life:

Example Hybrid Strategy for a 60-year-old:

- $200,000 10-year term ($152/month) → Covers mortgage and income replacement

- $25,000 whole life ($138/month) → Permanent final expense coverage

- Total: $290/month

At age 70, the term expires but you still have $25,000 permanent coverage for final expenses—exactly when you need it most.

Real-World Examples

Let’s see how different seniors made their term length decisions.

Example 1: Robert, Age 55 – Chose 20-Year Term

Situation: Robert has a $180,000 mortgage with 18 years remaining. His wife Sarah doesn’t work and depends on his income.

Decision: 20-year, $250,000 term life insurance at $185/month.

Reasoning: The 20-year term covers his mortgage payoff timeline and provides income replacement for Sarah until she reaches full Social Security retirement age at 67. A 10-year term would leave 8 years of mortgage payments unprotected.

Total cost: $44,400 over 20 years for complete protection.

Example 2: Margaret, Age 62 – Chose 10-Year Term

Situation: Margaret’s mortgage is paid off. She wants coverage until her husband Tom turns 70 and their pension benefits maximize.

Decision: 10-year, $150,000 term life insurance at $130/month, plus $15,000 whole life at $89/month for final expenses.

Reasoning: She only needs 8 years of significant coverage, making the 10-year term perfect. The whole life policy ensures final expenses are covered permanently after the term expires.

Total cost: $219/month for $165,000 total coverage, with $15,000 permanent.

Example 3: James, Age 58 – Chose 20-Year Term Over Two 10-Year Policies

Situation: James needs coverage until age 78 when his pension survivor benefits fully kick in for his wife.

Decision: 20-year, $200,000 term life insurance at $245/month.

Reasoning: James compared:

- Single 20-year term: $245/month × 240 months = $58,800

- Two 10-year terms: ($95 × 120) + ($248 × 120) = $41,160

Wait—the two 10-year terms seem cheaper! But James chose the 20-year because:

- He’d have to medically qualify again at age 68

- His Type 2 diabetes might worsen, causing denial or much higher rates

- The 20-year rate is guaranteed for 20 years

Smart move: Locking in the rate now protects against future health changes.

Example 4: Dorothy, Age 68 – Only Option Was 10-Year Term

Situation: Dorothy wants life insurance to help her daughter pay off student loans if something happens. Her daughter will finish paying loans in about 8 years.

Decision: 10-year, $75,000 term life insurance at $165/month.

Reasoning: At 68, 20-year terms weren’t available from any carrier Dorothy applied to. The 10-year term perfectly matches her daughter’s loan payoff timeline. Dorothy also purchased a $10,000 final expense whole life policy to ensure burial costs are always covered.

Example 5: William, Age 72 – Chose Whole Life Over Term

Situation: William wants to leave money for his grandchildren’s education. He’s not sure when he’ll pass away.

Decision: $50,000 whole life insurance at $568/month instead of term.

Reasoning: At 72, a 10-year term would cost $350+/month and expire at age 82. There’s no guarantee William will pass away before 82. With whole life, his grandchildren are guaranteed to receive $50,000 whenever he dies—whether at 75 or 95. The permanent nature of whole life made more sense for his legacy goal.

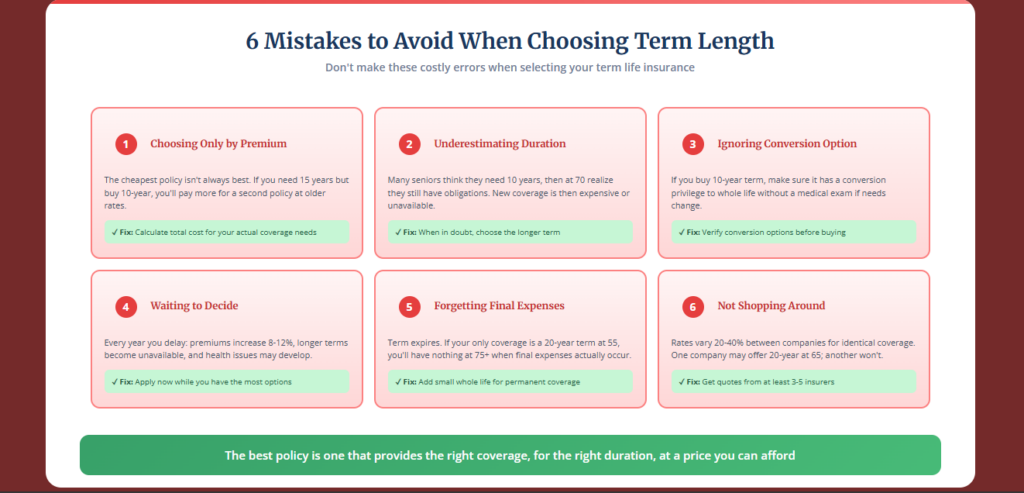

Common Mistakes to Avoid

Mistake #1: Choosing Based Only on Monthly Premium

The cheapest policy isn’t always the best value. A 10-year term might cost less per month, but if you need 15 years of coverage, you’ll end up paying more for a second policy (at higher rates with older age).

Mistake #2: Underestimating How Long You Need Coverage

Many seniors think they only need 10 years of coverage, then realize at age 70 that they still have financial obligations. By then, new coverage is expensive or unavailable. When in doubt, choose the longer term.

Mistake #3: Ignoring the Conversion Option

If you buy a 10-year term, make sure it has a conversion privilege. This allows you to convert to whole life without a medical exam if your needs change or your health declines.

Mistake #4: Waiting to Decide

Every year you delay:

- Premiums increase 8-12%

- Longer terms become unavailable

- Health issues may develop

If you’re 58 debating between 10-year and 20-year, don’t wait until 60 when the 20-year is harder to get.

Mistake #5: Forgetting About Final Expenses

Term insurance expires. If your entire life insurance strategy is a 20-year term purchased at age 55, you’ll have no coverage at age 75+ when final expenses actually occur. Consider a small whole life policy alongside your term coverage.

Mistake #6: Not Shopping Multiple Companies

Rates vary 20-40% between insurance companies for identical coverage. Always get quotes from at least 3-5 insurers before purchasing.

Frequently Asked Questions

Is 10-year or 20-year term life insurance better for seniors?

It depends on your age and needs. For seniors aged 50-60, a 20-year term often makes sense if you have long-term obligations like a mortgage or need income replacement for a spouse. For seniors 65 and older, 10-year terms are usually more practical because 20-year terms may not be available or affordable. The key is matching your term length to how long you actually need coverage.

How much more expensive is 20-year term than 10-year?

A 20-year term typically costs 30-50% more per month than a 10-year term for the same coverage amount. For example, a healthy 60-year-old male might pay $87/month for a 10-year, $100,000 policy versus $145/month for a 20-year policy—a difference of about 67%. However, the 20-year provides double the coverage duration.

Can I get a 20-year term life insurance policy at age 65?

It’s possible but limited. Some insurance companies offer 20-year terms to applicants up to age 65, but many cap it at age 60. At 65, you’ll face fewer options, higher premiums, and stricter underwriting. If you’re 63-65 and think you might need a 20-year term, apply immediately before turning 65 when options become even more limited.

What happens at the end of a 10-year or 20-year term policy?

When your term expires, you typically have three options: (1) Let coverage end if you no longer need it, (2) Renew year-to-year at much higher rates without a medical exam, or (3) Convert to a permanent whole life policy without a medical exam if your policy has a conversion privilege. Option 3 is especially valuable if your health has declined.

Should I buy two 10-year policies instead of one 20-year?

Usually no. While two consecutive 10-year policies might seem flexible, you’ll face medical underwriting again at age 65 or 70 when you apply for the second policy. If your health has declined, you could be denied or pay much higher rates. A single 20-year policy locks in your rate and eliminates requalification risk.

What’s the oldest age I can buy term life insurance?

For 10-year terms, most companies accept applicants up to age 70-75. For 20-year terms, the cutoff is usually age 60-65. Some companies have lower or higher limits. After age 75, term insurance becomes very limited, and most seniors turn to whole life insurance (which is available up to age 85+).

Is term life insurance worth it for seniors over 60?

Yes, term life insurance can be very worthwhile for seniors over 60 who have specific financial obligations like a mortgage, want income replacement for a surviving spouse, or need coverage for a defined period. It’s significantly cheaper than whole life for the same coverage amount. However, seniors over 70 should consider whole life insurance as well, since term coverage becomes expensive and expires when you may still need protection.

Can I convert my term policy to whole life later?

Most term policies include a conversion privilege that allows you to convert to permanent whole life insurance without a medical exam. This is valuable if your health declines during the term. However, conversion windows vary—some allow conversion anytime, others only during the first 5-10 years or before age 65-70. Check your policy for specific conversion rules.

What if I outlive my term life insurance policy?

If you outlive your term policy, coverage ends and you receive nothing back (unless you have a return of premium policy). This is normal—term insurance is designed to protect against premature death, not as a savings vehicle. If you still need coverage, you can renew year-to-year at higher rates, convert to whole life, or apply for a new policy (with new medical underwriting).

Should seniors combine term and whole life insurance?

Yes, combining term and whole life is often the smartest strategy for seniors. For example: a 10-year or 20-year term policy covers your mortgage and income replacement needs, while a smaller whole life policy ($15,000-$25,000) provides permanent coverage for final expenses. This way, you’re protected during your peak financial obligation years AND guaranteed coverage for funeral costs no matter when you pass away.

Taking the Next Step

Choosing between 10-year and 20-year term life insurance comes down to three factors:

- How long do you need coverage?

- What’s available at your age?

- What fits your budget?

Quick Decision Guide:

| Your Age | Primary Need | Best Choice |

|---|---|---|

| 50-60 | Mortgage/income 15+ years | 20-year term |

| 50-60 | Mortgage/income 10 years or less | 10-year term |

| 60-65 | Any duration | 10-year + whole life combo |

| 65-70 | Any duration | 10-year term (+ whole life for permanence) |

| 70+ | Any duration | 10-year term or whole life only |

Remember:

- Don’t wait—premiums increase every year

- Consider a hybrid approach: term for temporary needs, whole life for permanent coverage

- Make sure your term policy has a conversion privilege

- Shop multiple companies for the best rates

The best policy is the one that provides the right coverage for the right duration at a price you can afford. Get quotes today while you have the most options available.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Life insurance rates and availability vary based on individual factors including age, health, tobacco use, and the insurance company. The rates shown are estimates for healthy, non-smoking individuals and may not reflect your actual costs. Term availability varies by company and may be different from the age ranges shown. Always consult with a licensed insurance professional for personalized recommendations.