How Much Life Insurance Do I Need at 60? (Calculator + Guide)

Posted in Senior Life Insurance on December 11, 2025 last updated on December 11, 2025

Posted in Senior Life Insurance on December 11, 2025 last updated on December 11, 2025

If you are asking how much life insurance do I need at 60, you’re asking one of the most important financial questions of your retirement years. The answer isn’t one-size-fits-all—it depends on your debts, your spouse’s financial security, your final expense wishes, and the legacy you want to leave behind.

The good news? Figuring out exactly how much life insurance you need at 60 is simpler than you might think. In this guide, we’ll walk you through a straightforward calculator, show you real examples of coverage amounts for people just like you, and help you understand the true cost of life insurance at age 60.

In This Guide:

- Simple life insurance calculator for 60-year-olds

- Step-by-step coverage calculation worksheet

- Real-world examples of coverage needs

- Current life insurance rates at age 60

- Types of term and whole life insurance available

- How to choose the right amount of coverage

- Frequently asked questions

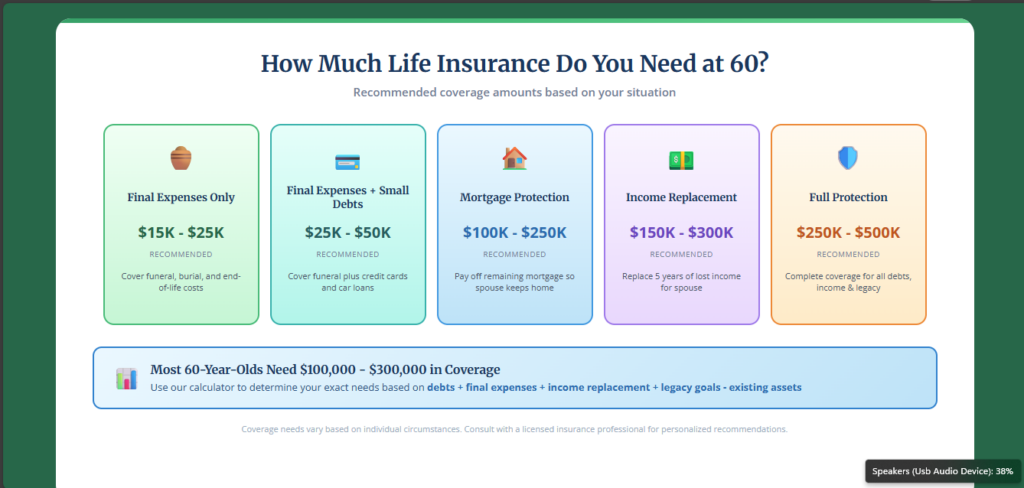

The Quick Answer: How Much Life Insurance do I need at 60?

Before we dive into the details, here’s a quick reference for how much life insurance most 60-year-olds need:

Most 60-year-olds need between $100,000 and $300,000 in life insurance coverage. However, your specific needs may be higher or lower depending on your individual circumstances.

| Situation | Recommended Coverage |

|---|---|

| Final expenses only | $15,000 – $25,000 |

| Final expenses + small debts | $25,000 – $50,000 |

| Mortgage protection | $100,000 – $250,000 |

| Income replacement (5 years) | $150,000 – $300,000 |

| Full financial protection | $250,000 – $500,000 |

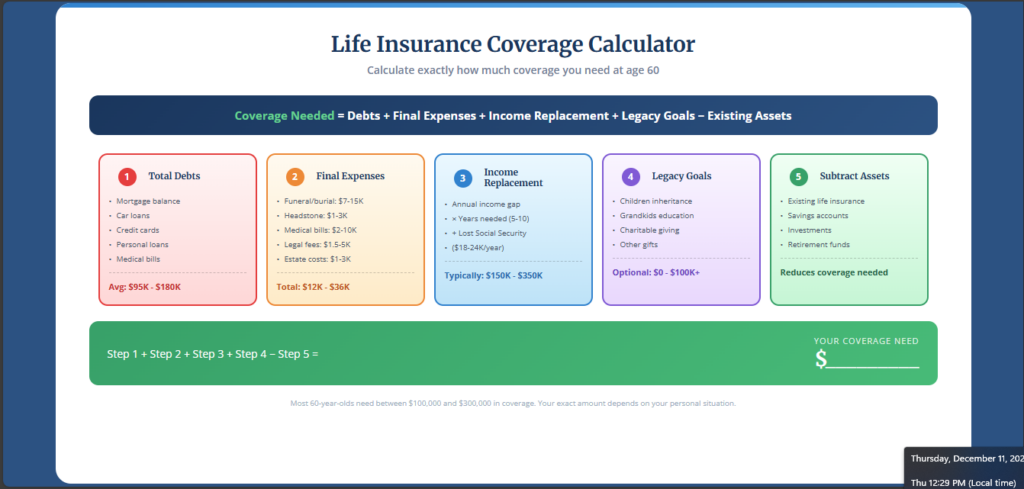

Life Insurance Calculator for 60-Year-Olds

Use this simple formula to calculate exactly how much life insurance you need at 60:

The Coverage Formula

Total Coverage Needed = Debts + Final Expenses + Income Replacement + Legacy Goals – Existing Assets

Let’s break down each component:

Step 1: Calculate Your Total Debts

Add up everything you owe:

| Debt Type | Your Amount |

|---|---|

| Remaining mortgage balance | $________ |

| Car loans | $________ |

| Credit card debt | $________ |

| Personal loans | $________ |

| Medical bills | $________ |

| Other debts | $________ |

| Total Debts | $________ |

Average for 60-year-olds: $95,000 – $180,000 (primarily mortgage)

Step 2: Add Final Expenses

These costs hit your family immediately after your passing:

| Expense Type | Estimated Cost |

|---|---|

| Funeral and burial | $7,000 – $15,000 |

| Headstone/memorial | $1,000 – $3,000 |

| Outstanding medical bills | $2,000 – $10,000 |

| Legal/probate fees | $1,500 – $5,000 |

| Estate settlement costs | $1,000 – $3,000 |

| Total Final Expenses | $12,500 – $36,000 |

Recommended amount: $25,000 covers most final expense needs comfortably.

Step 3: Calculate Income Replacement

If your spouse depends on your income or Social Security benefits, calculate how much they’d need:

Income Replacement Formula:

- Annual household income: $________

- Minus spouse’s income: $________

- Income gap: $________ per year

- Multiply by years needed (typically 5-10 years): × ________

- Total income replacement: $________

Example: If your household has $80,000 annual income and your spouse earns $30,000, the gap is $50,000/year. For 5 years of replacement: $50,000 × 5 = $250,000

Don’t forget Social Security: When one spouse dies, the household loses the smaller of the two Social Security checks—often $1,500-$2,000/month ($18,000-$24,000/year).

Step 4: Add Legacy Goals (Optional)

What do you want to leave behind?

| Legacy Goal | Amount |

|---|---|

| Children’s inheritance | $________ |

| Grandchildren’s education | $________ |

| Charitable donations | $________ |

| Other gifts | $________ |

| Total Legacy Goals | $________ |

Step 5: Subtract Existing Assets

What resources does your family already have?

| Asset Type | Amount |

|---|---|

| Existing life insurance | $________ |

| Savings accounts | $________ |

| Investment accounts | $________ |

| Retirement funds (accessible) | $________ |

| Other liquid assets | $________ |

| Total Existing Assets | $________ |

Your Coverage Calculation

Total Debts: $________ + Final Expenses: $________ + Income Replacement: $________ + Legacy Goals: $________ – Existing Assets: $________ = COVERAGE NEEDED: $________

Real-World Examples: Coverage at Age 60

Let’s look at three realistic scenarios to see how the calculator works in practice.

Example 1: Margaret – Minimal Coverage Needs

Situation: Margaret, 60, is a widow with a paid-off home. Her children are financially independent. She has $150,000 in retirement savings and just wants to cover her final expenses.

Calculation:

- Debts: $0 (mortgage paid off)

- Final expenses: $25,000

- Income replacement: $0 (no dependents)

- Legacy goals: $10,000 (small gift to grandchildren)

- Existing assets: $150,000 retirement + $0 life insurance

Coverage needed: $25,000 + $10,000 = $35,000 Minus existing assets she wants to preserve: Prefers not to use retirement funds Recommended coverage: $35,000 – $50,000 (final expense/whole life policy)

Monthly cost: Approximately $62-$85/month for whole life coverage

Example 2: Robert – Moderate Coverage Needs

Situation: Robert, 60, is married with a $120,000 mortgage (12 years remaining). His wife Patricia doesn’t work and depends on his $65,000 annual income. They have $80,000 in savings.

Calculation:

- Debts: $120,000 (mortgage) + $8,000 (car loan) = $128,000

- Final expenses: $25,000

- Income replacement: $65,000 × 5 years = $325,000

- Legacy goals: $0

- Existing assets: $80,000 savings + $50,000 employer life insurance

Total needs: $128,000 + $25,000 + $325,000 = $478,000 Minus existing assets: $478,000 – $130,000 = $348,000 Recommended coverage: $350,000

Monthly cost: Approximately $285-$350/month for 15-year term

Example 3: James & Linda – Higher Coverage Needs

Situation: James, 60, and Linda, 58, both work. Combined income: $140,000. They have a $200,000 mortgage, want to leave $100,000 to their three children, and have $200,000 in retirement accounts.

Calculation:

- Debts: $200,000 (mortgage) + $15,000 (other) = $215,000

- Final expenses: $25,000 (each) = $50,000

- Income replacement: $70,000 × 7 years = $490,000 (if James dies)

- Legacy goals: $100,000

- Existing assets: $200,000 retirement + $100,000 employer coverage

Total needs: $215,000 + $50,000 + $490,000 + $100,000 = $855,000 Minus existing assets: $855,000 – $300,000 = $555,000 Recommended coverage: $500,000 – $600,000 (split between spouses)

Monthly cost: Approximately $380-$480/month for 20-year term

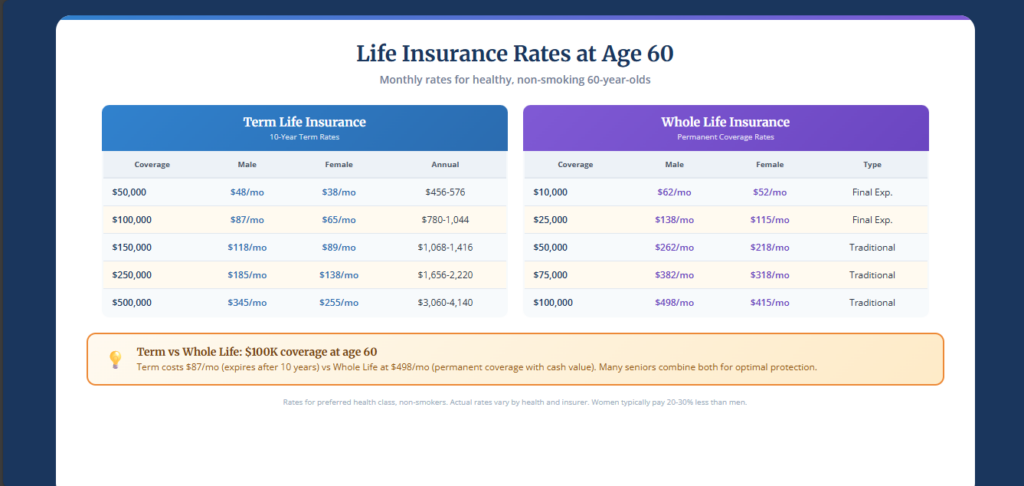

Life Insurance Rates at Age 60

Understanding what you’ll pay helps you budget and choose the right coverage amount. Here are current rates for healthy, non-smoking 60-year-olds.

Term Life Insurance Rates at Age 60

10-Year Term Life Insurance

| Coverage Amount | Male Monthly | Female Monthly | Annual Cost |

|---|---|---|---|

| $50,000 | $48 | $38 | $456 – $576 |

| $100,000 | $87 | $65 | $780 – $1,044 |

| $150,000 | $118 | $89 | $1,068 – $1,416 |

| $200,000 | $152 | $112 | $1,344 – $1,824 |

| $250,000 | $185 | $138 | $1,656 – $2,220 |

| $300,000 | $218 | $162 | $1,944 – $2,616 |

| $500,000 | $345 | $255 | $3,060 – $4,140 |

15-Year Term Life Insurance

| Coverage Amount | Male Monthly | Female Monthly |

|---|---|---|

| $100,000 | $112 | $84 |

| $200,000 | $198 | $148 |

| $250,000 | $238 | $178 |

| $300,000 | $278 | $208 |

| $500,000 | $445 | $332 |

20-Year Term Life Insurance

| Coverage Amount | Male Monthly | Female Monthly |

|---|---|---|

| $100,000 | $145 | $108 |

| $200,000 | $262 | $195 |

| $250,000 | $318 | $238 |

| $300,000 | $372 | $278 |

| $500,000 | $598 | $448 |

Note: 20-year terms may have limited availability at age 60 depending on the insurer.

Whole Life Insurance Rates at Age 60

Traditional Whole Life Insurance

| Coverage Amount | Male Monthly | Female Monthly |

|---|---|---|

| $10,000 | $62 | $52 |

| $15,000 | $89 | $75 |

| $25,000 | $138 | $115 |

| $50,000 | $262 | $218 |

| $75,000 | $382 | $318 |

| $100,000 | $498 | $415 |

Final Expense / Burial Insurance

| Coverage Amount | Male Monthly | Female Monthly |

|---|---|---|

| $5,000 | $35 | $29 |

| $10,000 | $62 | $52 |

| $15,000 | $89 | $75 |

| $20,000 | $115 | $96 |

| $25,000 | $138 | $115 |

Rates shown are for healthy non-smokers in preferred or standard health classes. Your actual rates may vary based on health conditions and the specific insurance company.

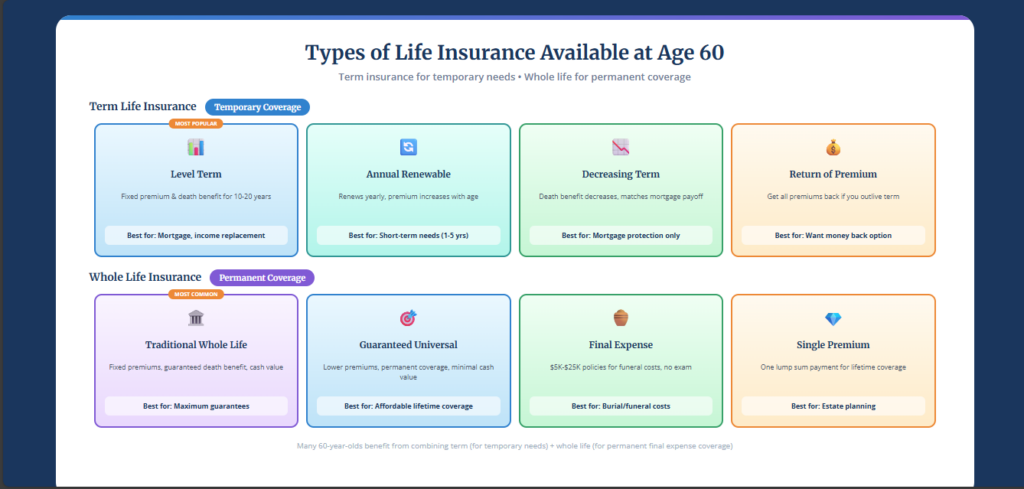

Types of Life Insurance for a 60-year-old

At age 60, you have access to both term and whole life insurance options. Understanding the differences between the types of life insurance available helps you choose the right type for your coverage needs.

Term Life Insurance Options at 60

Term life insurance provides coverage for a specific period. It’s ideal for temporary needs like mortgage protection or income replacement.

1. Level Term Life Insurance (Most Popular)

What it is: Fixed premium and death benefit for the entire term (10, 15, or 20 years).

Best for: Mortgage protection, income replacement, covering debts with a specific payoff date.

At age 60: You can typically get 10, 15, or 20-year terms, though 20-year terms may have limited availability or higher rates.

Pros:

- Lowest cost for maximum coverage

- Predictable premiums

- Simple to understand

Cons:

- Coverage ends when term expires

- No cash value

- Expensive to renew after term ends

2. Annual Renewable Term (ART)

What it is: Coverage that renews each year without a medical exam, but premiums increase annually.

Best for: Short-term needs (1-5 years), bridge coverage, uncertain timelines.

At age 60: Good option if you only need coverage for a few years or are unsure how long you’ll need protection.

Pros:

- Lower initial premiums

- Flexible—cancel anytime

- No long-term commitment

Cons:

- Premiums increase each year

- Becomes very expensive over time

- Not cost-effective for long-term needs

3. Decreasing Term Life Insurance

What it is: Death benefit decreases over time while premiums stay level. Often called “mortgage protection insurance.”

Best for: Covering a mortgage or debt that decreases over time.

At age 60: Excellent choice if your primary goal is mortgage protection and you have 10-15 years left on your loan.

Pros:

- 20-40% cheaper than level term

- Matches declining debt

- Fixed premiums

Cons:

- Coverage decreases even if needs don’t

- Less flexibility

- Not suitable for inheritance goals

4. Return of Premium (ROP) Term

What it is: If you outlive the term, you get all your premiums back.

Best for: Those who want coverage but don’t want to “lose” money if they survive.

At age 60: Available but premiums are 2-4 times higher. Consider carefully whether the return is worth the extra cost.

Pros:

- Get your money back if you survive

- Acts as forced savings

Cons:

- Much higher premiums

- Money returned has lost value to inflation

- Better returns possible by investing the difference

Whole Life Insurance Options at 60

Whole life insurance provides permanent coverage that lasts your entire life with cash value accumulation.

1. Traditional Whole Life Insurance

What it is: Permanent coverage with fixed premiums, guaranteed death benefit, and cash value growth.

Best for: Guaranteed lifetime coverage, estate planning, leaving an inheritance.

At age 60: Premiums are higher than term but lock in for life. Cash value grows slowly but steadily.

Pros:

- Coverage never expires

- Fixed premiums for life

- Builds cash value

- May pay dividends

Cons:

- Higher premiums than term

- Slow cash value growth

- Less flexibility

2. Guaranteed Universal Life (GUL)

What it is: Permanent coverage with lower premiums than traditional whole life but minimal cash value.

Best for: Affordable lifetime coverage without needing cash value.

At age 60: Excellent option if you want permanent coverage at the lowest cost and don’t care about cash value accumulation.

Pros:

- Lower premiums than traditional whole life

- Guaranteed coverage to age 90, 95, 100, or beyond

- Predictable costs

Cons:

- Little or no cash value

- Policy can lapse if premiums aren’t paid

- Less flexibility

3. Final Expense / Burial Insurance

What it is final expense or burial insurance: Small whole life policies ($5,000-$25,000) designed to cover funeral and burial costs.

Best for: Guaranteed issue coverage, seniors with health issues, easy qualification.

At age 60: Widely available with no medical exam required. Guaranteed acceptance options available.

Pros:

- Easy to qualify

- No medical exam

- Permanent coverage

- Available up to age 85+

Cons:

- Limited coverage amounts

- Higher cost per $1,000 of coverage

- Some policies have graded benefits (2-year waiting period)

4. Single Premium Whole Life

What it is: One lump sum payment buys lifetime coverage with no ongoing premiums.

Best for: Seniors with significant savings who want to convert cash into a larger death benefit.

At age 60: If you have $25,000-$100,000+ available, you can purchase $50,000-$200,000+ in death benefit coverage.

Pros:

- No ongoing premiums

- Immediate coverage

- Leverages money for larger death benefit

- Great for estate planning

Cons:

- Requires large upfront payment

- May be classified as MEC with tax implications

- Less flexible once purchased

How to Choose the Right Coverage Amount

Use this decision framework to determine your ideal coverage:

If Your Primary Goal is Final Expenses Only:

Recommended coverage: $15,000 – $35,000 Best policy type: Final expense whole life insurance Why: Permanent coverage ensures your funeral costs are always covered, regardless of when you pass away.

If You Need to Protect Your Mortgage:

Recommended coverage: Equal to your remaining mortgage balance Best policy type: Level term (matching your mortgage payoff timeline) OR decreasing term Why: Ensures your spouse can stay in the home without the burden of mortgage payments.

If You Need Income Replacement for Your Spouse:

Recommended coverage: 5-10 times your annual income contribution Best policy type: Level term life insurance (10-20 year term) Why: Provides your spouse time to adjust financially, pay off debts, and build their own retirement security.

If You Want Comprehensive Protection:

Recommended coverage: Use the calculator above for your exact needs Best policy type: Combination of term + whole life Why: Term covers your larger temporary needs (mortgage, income replacement) while whole life guarantees final expenses forever.

The Hybrid Strategy for 60-Year-Olds

Many financial advisors recommend combining term and whole life insurance at age 60:

Example Hybrid Approach:

- $250,000 15-year term ($185/month) → Covers mortgage + income replacement

- $25,000 whole life ($138/month) → Covers final expenses permanently

- Total: $323/month for $275,000 coverage

After 15 years (age 75), the term expires but you still have $25,000 whole life coverage for final expenses—exactly when you need it most.

Check out our post term life insurance vs whole life insurance to compare.

Common Mistakes to Avoid

Mistake #1: Underestimating Your Coverage Needs

Many 60-year-olds assume they need less coverage because they’re “older.” But if you have a mortgage, a spouse who depends on your income, or debts that would burden your family, you may need more coverage than you think.

Mistake #2: Overestimating Your Coverage Needs

On the flip side, don’t buy more than you need. If your mortgage is paid off, your children are independent, and you have substantial savings, you may only need final expense coverage.

Mistake #3: Waiting to Apply

Every year you wait, premiums increase 8-12%. At 60, you’re still young enough to qualify for competitive rates. By 65 or 70, your options become more limited and expensive. Also, you could be stuck buying life insurance with pre-existing conditions, such as diabetes, heart disease, or cancer.

Mistake #4: Not Considering Your Spouse

If you’re married, calculate coverage needs for both spouses. What happens if you die? What happens if your spouse dies? Both scenarios require planning.

Mistake #5: Forgetting About Social Security

When one spouse dies, the household loses the smaller Social Security check—often $1,500-$2,000/month. Factor this income loss into your coverage calculations.

Mistake #6: Buying Only Term Life

If you buy a 20-year term at 60, it expires at age 80. What then? Consider having at least some permanent whole life coverage for final expenses.

Mistake #7: Not Shopping Multiple Companies

Rates vary 30-50% between insurance companies. Always get quotes from at least 3-5 insurers before purchasing.

Frequently Asked Questions

How much life insurance does a 60-year-old need?

Most 60-year-olds need between $100,000 and $300,000 in life insurance coverage. However, your specific needs depend on your debts (especially mortgage), whether your spouse depends on your income, your final expense wishes, and any legacy goals. Use our calculator above to determine your exact coverage needs based on your personal situation.

What is the average life insurance payout for a 60-year-old?

The average life insurance policy for Americans aged 55-64 has a death benefit between $100,000 and $250,000. However, “average” doesn’t mean “right for you.” Your coverage should be based on your specific financial obligations, not what others have purchased.

Is it too late to get life insurance at 60?

Absolutely not. Age 60 is an excellent time to purchase life insurance. You can still qualify for term policies up to 20 years and have access to all types of whole life insurance. Rates are higher than at younger ages, but coverage is readily available for healthy 60-year-olds.

How much does $100,000 life insurance cost at 60?

For a healthy, non-smoking 60-year-old, a 10-year term policy with $100,000 coverage costs approximately $65-$87 per month ($780-$1,044 annually). Whole life insurance for the same coverage costs approximately $415-$498 per month. Women typically pay 20-30% less than men.

How much life insurance do I need if my house is paid off?

If your mortgage is paid off, your coverage needs are typically lower. Focus on: final expenses ($15,000-$25,000), income replacement for your spouse if applicable (3-5 years of expenses), any remaining debts, and legacy goals. Many seniors with paid-off homes need $50,000-$150,000 in coverage.

Do I need life insurance at 60 if I’m single with no dependents?

If no one depends on your income, your life insurance needs are minimal. Consider a small policy ($10,000-$25,000) to cover final expenses so family members don’t have to pay for your funeral. Beyond that, life insurance may not be necessary unless you want to leave a legacy to charity or loved ones.

What is the best life insurance for a 60-year-old?

The “best” life insurance depends on your needs. For most 60-year-olds, a combination approach works well: a level term policy for larger temporary needs (mortgage, income replacement) plus a small whole life policy for permanent final expense coverage. If you only need final expense coverage, a burial insurance policy is often the best choice.

Can I get life insurance at 60 with health problems?

Yes. Many insurance companies specialize in covering seniors with health conditions like diabetes, heart disease, high blood pressure, and more. Guaranteed issue whole life policies accept everyone regardless of health (though they may have 2-year graded benefit periods). Work with an independent agent who can shop multiple carriers for your specific health situation.

How much life insurance should a married couple have at 60?

Each spouse should have enough coverage to protect the other. Calculate separately: What debts would remain? What income would be lost? What final expenses would occur? Many married couples at 60 carry $200,000-$500,000 combined coverage, split based on each spouse’s income contribution and financial obligations.

Taking the Next Step

Determining how much life insurance you need at 60 comes down to a simple formula: add up your debts, final expenses, and income replacement needs, then subtract your existing assets. For most 60-year-olds, this results in a coverage need between $100,000 and $300,000.

Remember these key points:

- Use the calculator to determine your exact coverage needs

- Don’t wait—every year you delay, premiums increase 8-12%

- Consider a hybrid approach—term for temporary needs, whole life for permanent coverage

- Shop multiple companies—rates vary 30-50% between insurers

- Be honest about your health—work with an independent agent if you have health concerns

The most important step is taking action. Request quotes from multiple insurance companies, compare your options, and secure the coverage your family needs.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Life insurance rates vary based on individual factors including age, health, tobacco use, and the insurance company. The rates and coverage examples shown are estimates and may not reflect your actual costs or needs. Always consult with a licensed insurance professional before purchasing any life insurance policy. Calculator results are estimates only—work with a financial advisor for personalized recommendations.