Life Insurance for Seniors With Congestive Heart Failure (CHF): Rates, Approval Tips & Best Companies (2026 Guide)

Posted in Uncategorized on June 9, 2026 last updated on June 9, 2026

Posted in Uncategorized on June 9, 2026 last updated on June 9, 2026

Is Life Insurance for Seniors with Congestive Heart Failure possible?

Yes, many seniors with congestive heart failure (CHF) can still qualify for life insurance.

However, approval depends on several important factors, including the severity of the condition, how well it is controlled, current symptoms, medications, hospitalizations, and overall health.

A diagnosis of congestive heart failure does not automatically mean you will be declined.

In fact, many seniors with mild or stable CHF qualify for life insurance every year. The key is understanding which companies are more favorable toward heart conditions and choosing the right type of policy.

Coverage options may include:

- Traditional life insurance

- Simplified issue life insurance

- No medical exam life insurance

- Final expense insurance

- Guaranteed issue life insurance

The best option depends on your age, health history, and the severity of your CHF.

Quick Answer

If you’re looking for the short version:

- Many seniors with CHF can still get life insurance.

- Mild or stable CHF generally has the best approval opportunities.

- Recent hospitalizations may limit options.

- Ejection fraction (EF) often plays an important role in underwriting.

- Final expense insurance is commonly available.

- Comparing multiple companies is essential.

- A decline from one company does not mean you cannot qualify elsewhere.

What Is Congestive Heart Failure?

The American Heart Association defines congestive heart failure, often called CHF, is a condition in which the heart cannot pump blood as efficiently as it should.

Despite the name, heart failure does not mean the heart has stopped working.

Instead, it means the heart’s pumping ability has weakened.

This can cause symptoms such as:

- Shortness of breath

- Fatigue

- Swelling in the legs and ankles

- Rapid heartbeat

- Difficulty exercising

- Fluid retention

CHF is common among older adults and often occurs alongside other medical conditions such as:

- High blood pressure

- Coronary artery disease

- Diabetes

- Kidney disease

- Obesity

- Sleep apnea

- High cholesterol

Because CHF affects life expectancy, insurance companies evaluate the condition carefully during underwriting.

How Life Insurance Companies Evaluate CHF

Every insurance company uses different underwriting guidelines.

However, most carriers will review several key factors.

Age at Diagnosis

When were you first diagnosed?

Applicants who were diagnosed many years ago and have remained stable often receive more favorable consideration than those with a recent diagnosis.

Severity of CHF

The severity of congestive heart failure plays a major role in approval decisions.

Insurance companies often review:

- NYHA Classification

- Symptom severity

- Exercise tolerance

- Hospitalizations

Ejection Fraction (EF)

One of the most important factors is ejection fraction.

Ejection fraction is commonly used by physicians to evaluate heart function.

Ejection fraction measures how effectively the heart pumps blood.

Typical guidelines include:

| Ejection Fraction | General Underwriting Outlook |

|---|---|

| 55%+ | Most Favorable |

| 45%-54% | Moderate Risk |

| 35%-44% | Higher Risk |

| Below 35% | Significant Underwriting Concerns |

A higher ejection fraction generally improves approval opportunities.

Hospitalizations

Insurance companies often ask:

- Have you been hospitalized?

- How recently?

- How many times?

Recent CHF-related hospitalizations usually increase underwriting scrutiny.

Medications

Insurance companies commonly review medications such as:

- Entresto

- Carvedilol

- Metoprolol

- Lisinopril

- Furosemide (Lasix)

- Spironolactone

Stable medication use can demonstrate good disease management.

Other Health Conditions

Insurance companies also review:

- Diabetes

- Kidney disease

- Obesity

- Sleep apnea

- High blood pressure

- Prior heart attacks

- Stents

- Bypass surgery

The overall health picture matters.

Why Some Seniors With CHF Get Better Rates Than Others

Many people assume all CHF diagnoses are treated the same.

That is not true.

Consider these examples:

Applicant A

- Diagnosed 8 years ago

- Ejection fraction 55%

- No recent hospitalizations

- Controlled blood pressure

- Active lifestyle

Applicant B

- Diagnosed 6 months ago

- Ejection fraction 30%

- Multiple hospitalizations

- Diabetes

- Kidney disease

Both applicants have CHF.

However, their underwriting outcomes may be dramatically different.

Insurance companies evaluate the stability and severity of the condition rather than simply checking a box that says “heart failure.”

Can You Be Denied Life Insurance Because of CHF?

The most common question seniors ask is can you be denied.

The answer is yes—but not always.

Some factors that increase the likelihood of a decline include:

- Severe CHF

- Ejection fraction below 30%

- Recent hospitalization

- Oxygen dependency

- Multiple serious health conditions

- Advanced kidney disease

- Frequent fluid retention episodes

Even when traditional life insurance is unavailable, many seniors still qualify for:

- Final expense insurance

- Simplified issue life insurance

- Guaranteed issue life insurance

A decline from one company should never be considered the final answer.

Different carriers evaluate CHF very differently.

CHF Severity Levels and Life Insurance Approval Chances

One of the most important factors in life insurance underwriting is the severity of congestive heart failure.

Insurance companies often use the New York Heart Association (NYHA) classification system to help evaluate how CHF affects daily activities and overall heart function.

NYHA Class I

Class I is considered the mildest form of CHF.

Characteristics include:

- No significant limitations during normal activities

- No shortness of breath during routine exercise

- Stable symptoms

- Good quality of life

Life Insurance Outlook:

This group generally has the best approval opportunities. Some applicants may qualify for traditionally underwritten policies depending on age and overall health.

NYHA Class II

Class II heart failure causes mild limitations during physical activity.

Characteristics include:

- Comfortable at rest

- Symptoms during moderate activity

- Occasional fatigue or shortness of breath

Life Insurance Outlook:

Coverage is often available, although premiums may be higher than applicants without heart disease.

NYHA Class III

Class III heart failure causes more noticeable limitations.

Characteristics include:

- Symptoms with everyday activities

- Reduced exercise tolerance

- Increased fatigue

Life Insurance Outlook:

Traditional underwriting becomes more challenging. Many applicants explore final expense, simplified issue, or no medical exam options.

NYHA Class IV

Class IV is considered severe heart failure.

Characteristics include:

- Symptoms at rest

- Significant limitations

- Frequent medical management

Life Insurance Outlook:

Traditional life insurance approval becomes difficult. Guaranteed issue and final expense policies are often the most realistic options.

| CHF Severity | Typical Approval Outlook | Common Coverage Options |

|---|---|---|

| NYHA Class I | Most Favorable | Traditional, No Exam, Simplified Issue |

| NYHA Class II | Good | Traditional, No Exam, Simplified Issue |

| NYHA Class III | Moderate | Simplified Issue, Final Expense |

| NYHA Class IV | Limited | Final Expense, Guaranteed Issue |

What Underwriting Class Can You Qualify For With CHF?

Many seniors want to know how congestive heart failure affects rates.

The answer depends on overall health, ejection fraction, hospital history, and symptom severity.

Standard

Possible for:

- Mild CHF

- Stable symptoms

- Strong ejection fraction

- No recent hospitalizations

Table Rated

Common for:

- Moderate CHF

- Controlled symptoms

- Additional risk factors

Simplified Issue

Common for:

- Moderate to severe CHF

- Multiple health conditions

- Older applicants

Guaranteed Issue

Often considered when:

- Traditional underwriting is unavailable

- Advanced CHF exists

- Significant health concerns are present

Best Life Insurance Options for Seniors With CHF

Traditional Life Insurance

Traditional underwriting may still be available for some applicants with mild or stable CHF.

Advantages:

- Higher coverage amounts

- Lower premiums

- More policy choices

Disadvantages:

- Medical records review

- Longer underwriting process

- Greater scrutiny of heart function

No Medical Exam Life Insurance

Some insurers rely on prescription histories and electronic medical records.

Advantages:

- Faster approval

- No bloodwork

- Simplified process

Best For:

- Stable CHF

- Seniors seeking convenience

Simplified Issue Life Insurance

These policies use health questions but no medical exam.

Advantages:

- Easier qualification

- Faster approval

- Permanent coverage options

Final Expense Insurance

Final expense insurance is often one of the most realistic options for seniors with CHF.

Advantages:

- Easier approval

- Permanent coverage

- Fixed premiums

- Coverage for funeral expenses

Guaranteed Issue Life Insurance

Guaranteed issue coverage accepts nearly everyone.

Advantages:

- No medical questions

- No medical exam

- Guaranteed acceptance

Disadvantages:

- Higher premiums

- Lower coverage amounts

- Waiting periods may apply

Best Life Insurance Companies for Seniors With CHF

Not all insurance companies view congestive heart failure the same way.

Mutual of Omaha

Best For:

- Final expense insurance

- Seniors ages 50-85

- Mild to moderate CHF

Foresters Financial

Best For:

- Simplified issue coverage

- Faster approvals

- Applicants with controlled CHF

Americo

Best For:

- Heart conditions

- Multiple health conditions

- Final expense products

AIG

Best For:

- Guaranteed issue coverage

- Advanced CHF

- Applicants declined elsewhere

Prudential

Best For:

- Mild CHF

- Larger coverage amounts

- Traditional underwriting

Protective

Best For:

- Stable heart conditions

- Term life insurance

- Higher face amounts

Best Companies Based on CHF Severity

| CHF Situation | Companies Worth Considering |

|---|---|

| Mild CHF | Prudential, Protective |

| Moderate CHF | Foresters, Americo |

| Severe CHF | Mutual of Omaha |

| Advanced CHF | Guaranteed Issue Carriers |

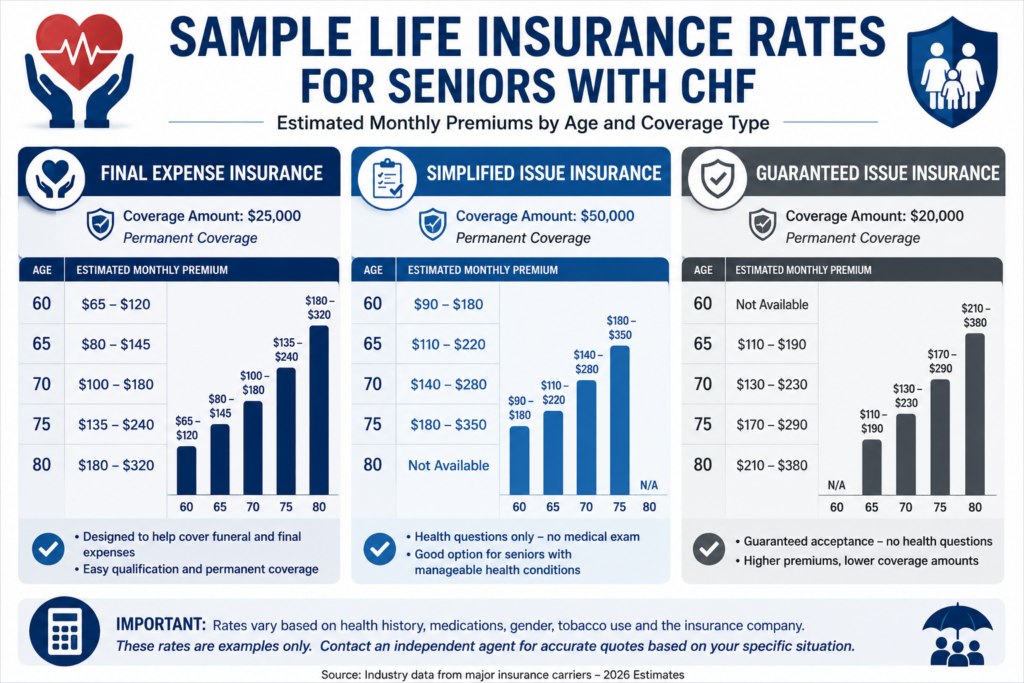

Sample Monthly Life Insurance Rates for Seniors With CHF

The examples below are illustrations only.

Actual rates vary based on age, gender, severity of CHF, tobacco use, medications, and overall health.

Sample Final Expense Rates

| Age | Coverage | Estimated Monthly Premium |

|---|---|---|

| 60 | $25,000 | $65-$120 |

| 65 | $25,000 | $80-$145 |

| 70 | $25,000 | $100-$180 |

| 75 | $25,000 | $135-$240 |

| 80 | $25,000 | $180-$320 |

Sample Simplified Issue Rates

| Age | Coverage | Estimated Monthly Premium |

|---|---|---|

| 60 | $50,000 | $90-$180 |

| 65 | $50,000 | $110-$220 |

| 70 | $50,000 | $140-$280 |

| 75 | $50,000 | $180-$350 |

Sample Guaranteed Issue Rates

| Age | Coverage | Estimated Monthly Premium |

|---|---|---|

| 65 | $20,000 | $110-$190 |

| 70 | $20,000 | $130-$230 |

| 75 | $20,000 | $170-$290 |

| 80 | $20,000 | $210-$380 |

CHF and Diabetes

Diabetes is one of the most common conditions that occurs alongside congestive heart failure.

Insurance companies frequently review:

- A1C levels

- Medication usage

- Kidney function

- Neuropathy

- Cardiovascular history

Well-controlled diabetes generally results in more favorable underwriting outcomes than uncontrolled diabetes.

CHF and Kidney Disease

Congestive heart failure and kidney disease frequently occur together.

Insurance companies may review:

- eGFR

- Creatinine levels

- Dialysis history

- Fluid retention

- Hospitalizations

Because both conditions affect long-term health outcomes, insurers evaluate them carefully during underwriting.

CHF and Sleep Apnea

Sleep apnea is another common condition among seniors with heart disease.

Insurance companies often ask:

- Is sleep apnea being treated?

- Are you using a CPAP machine?

- Is treatment compliant?

Applicants who actively manage sleep apnea often receive better underwriting consideration.

Real-Life Example: How One Senior With CHF Was Able to Get Approved

A 72-year-old applicant contacted us after being told by another agent that congestive heart failure would prevent him from qualifying for life insurance.

Like many seniors, he assumed that a CHF diagnosis automatically meant he would either be declined or forced to purchase an expensive guaranteed issue policy.

His health profile included:

- CHF diagnosis 6 years earlier

- Ejection fraction of approximately 50%

- Controlled blood pressure

- Type 2 diabetes

- No CHF-related hospitalizations in more than 3 years

- Consistent medication compliance

- Non-smoker

Although his condition had remained stable for several years, several insurance companies were unwilling to offer favorable underwriting decisions because of the combination of CHF and diabetes.

At first glance, his application appeared challenging.

Many insurance companies view congestive heart failure as a significant risk factor because it can increase the likelihood of future cardiovascular complications. When diabetes is added to the picture, some carriers become even more cautious.

Fortunately, not every company evaluates heart conditions the same way.

Rather than submitting an application to a single carrier, we compared multiple insurance companies that have historically been more favorable toward applicants with stable heart conditions.

During the underwriting process, several factors worked in his favor:

- His CHF had remained stable for years.

- He had not experienced recent hospitalizations.

- His ejection fraction remained relatively strong.

- His diabetes was being actively managed.

- He followed his physician’s treatment recommendations.

- He maintained regular medical follow-up appointments.

Because of these positive factors, he was eventually approved for coverage that provided meaningful financial protection for his family.

Even better, the premium was significantly lower than he expected.

The experience reinforced an important lesson that we see regularly:

A diagnosis alone does not determine your life insurance outcome.

Two applicants may both have congestive heart failure, but their approval opportunities can be dramatically different depending on factors such as:

- Ejection fraction

- Symptom severity

- Hospitalization history

- Medication compliance

- Diabetes control

- Kidney function

- Overall cardiovascular health

This is one reason why comparing multiple companies is so important.

A carrier that is highly competitive for one applicant may not be the best choice for another.

If you have been told that your CHF diagnosis makes life insurance impossible, don’t assume the first answer is the final answer. Many seniors are surprised to discover that affordable coverage options remain available when the right company is selected.

Helpful Resources

You may also find these guides helpful:

Frequently Asked Questions

Can you get life insurance with congestive heart failure?

Yes. Many seniors with congestive heart failure can still qualify for life insurance. Approval depends on factors such as severity, ejection fraction, hospitalizations, medications, and overall health.

Will CHF automatically disqualify me from life insurance?

No. While severe CHF may limit some options, many applicants still qualify for traditional, simplified issue, final expense, or guaranteed issue coverage.

What is the easiest life insurance policy to qualify for with CHF?

Final expense insurance and guaranteed issue life insurance are often the easiest options for seniors with congestive heart failure.

Does ejection fraction affect life insurance approval?

Yes. Ejection fraction is one of the most important underwriting factors for heart failure applicants. Higher ejection fractions generally create more favorable underwriting opportunities.

Can I get life insurance if I have CHF and diabetes?

Yes. Many applicants with both CHF and diabetes qualify for coverage. Insurance companies will evaluate diabetes control, A1C levels, kidney function, and overall cardiovascular health.

Can I get life insurance if I have CHF and kidney disease?

Possibly. Approval depends on the severity of both conditions, kidney function, dialysis history, and overall stability.

Do I need a medical exam?

Not always. Many companies offer no medical exam, simplified issue, and final expense options.

What if I was declined before?

A previous decline does not necessarily mean you cannot qualify elsewhere. Different insurance companies use different underwriting guidelines.

Get Personalized Life Insurance Quotes — Even With Congestive Heart Failure

A diagnosis of congestive heart failure does not automatically mean life insurance is out of reach.

Many seniors are surprised to learn they still qualify for coverage—even with CHF, diabetes, kidney disease, sleep apnea, high blood pressure, or multiple health conditions.

The challenge is finding the right insurance company.

Every insurer evaluates heart conditions differently. One company may decline an application while another may offer affordable coverage.

That’s why Rob and Tracy Pinner compare multiple life insurance companies on your behalf.

We Can Help You Compare:

✅ Traditional Life Insurance

✅ No Medical Exam Life Insurance

✅ Simplified Issue Life Insurance

✅ Final Expense Insurance

✅ Guaranteed Issue Life Insurance

Get Help If You Have:

- Congestive Heart Failure (CHF)

- Heart Disease

- Previous Heart Attack

- High Blood Pressure

- Diabetes

- Sleep Apnea

- Kidney Disease

- Multiple Health Conditions

Don’t assume you will be declined or forced to overpay.

Request a personalized quote today and discover which companies may offer the best approval opportunities and rates for your specific health profile.

Get Your Free Life Insurance Quote Today

Why Trust Really Smart Insurance?

Really Smart Insurance specializes in helping seniors compare life insurance options across multiple insurance companies.

We regularly assist applicants with:

- Congestive Heart Failure

- Heart Disease

- Previous Heart Attacks

- Diabetes

- High Blood Pressure

- Kidney Disease

- Sleep Apnea

- Multiple Health Conditions

Because we are independent agents, we can compare multiple carriers to help identify companies that may offer better rates and approval opportunities based on your unique health history.

Final Thoughts

Being diagnosed with congestive heart failure can make shopping for life insurance feel overwhelming.

The good news is that many seniors with CHF still qualify for coverage every year.

The key is understanding how insurance companies evaluate heart failure, knowing which policy types may be available, and comparing multiple carriers rather than relying on a single company.

Whether you are looking for term life insurance, final expense insurance, no medical exam coverage, or guaranteed issue protection, there are often more options available than you might expect.

Seniors should continue following treatment recommendations from their healthcare providers.

By working with an independent agency and comparing multiple insurers, you can improve your chances of finding affordable coverage that helps protect your loved ones and your legacy.