Life Insurance for Seniors with a Heart Murmur: 2026 Guide + Rates

Posted in Life Insurance w/ Pre-existing Conditions on July 8, 2026 last updated on July 8, 2026

Posted in Life Insurance w/ Pre-existing Conditions on July 8, 2026 last updated on July 8, 2026

Is Life Insurance for Seniors with a Heart Murmur possible?

| Yes. Most seniors with a heart murmur qualify for life insurance, and many with an innocent (functional) murmur and no other heart problems can still qualify for Preferred or Standard rates. If your murmur is organic — caused by an actual valve or structural issue — you can usually still get approved, typically at a Standard to Table-rated premium, and guaranteed issue or simplified issue final expense policies are always available as a fallback with no medical exam. |

Hearing the words “your doctor detected a heart murmur” during a routine checkup is enough to make anyone worry — especially if you’re a senior shopping for life insurance to protect your family or cover final expenses. The good news is that a heart murmur, by itself, rarely stops you from getting approved for coverage.

As a licensed independent life insurance agent appointed with more than a dozen top-rated carriers, I work with seniors who have heart murmurs every week. In this guide, I’ll walk you through exactly what underwriters look for, which policies make the most sense, which companies tend to offer the best rates, and what you can expect to pay — so you can shop with confidence instead of guessing.

What Is a Heart Murmur?

According to the Mayo Clinic, a heart murmur is an extra whooshing, swishing, or rasping sound heard between normal heartbeats, caused by turbulent blood flow through or near the heart. Doctors typically discover a murmur using a stethoscope during a routine physical exam or an insurance medical exam.

Heart murmurs fall into two broad categories:

- Innocent (functional) murmurs — caused by normal, healthy blood flow through a structurally normal heart. Very common in both children and older adults, and generally harmless.

- Organic (abnormal) murmurs — caused by an underlying structural issue such as a valve that doesn’t open or close properly (stenosis or regurgitation), a congenital heart defect, or another cardiac condition.

The murmur itself is just a sound. What matters to a life insurance underwriter is the cause behind that sound — which is why the next few sections matter so much.

| Key takeaway An innocent heart murmur with no other cardiac findings typically has zero impact on your rate class. An organic murmur tied to valve disease may lower your rate class, but it very rarely results in an outright decline — there is almost always a policy available. |

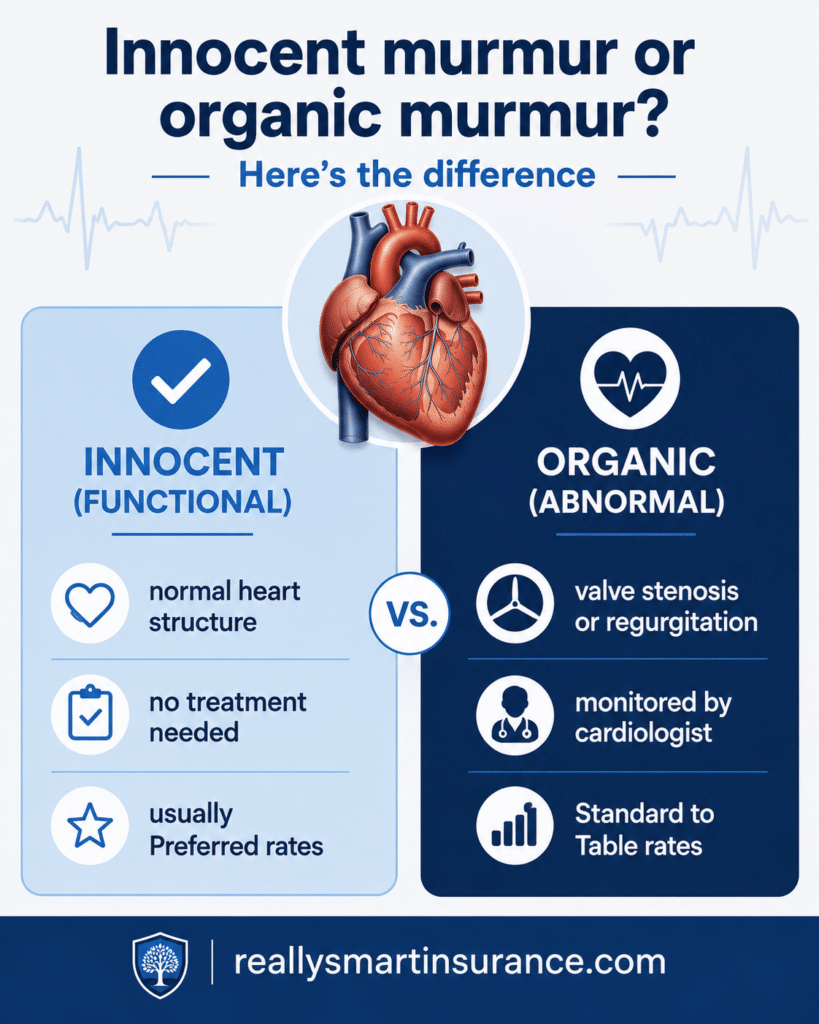

Innocent vs. Abnormal Heart Murmurs

Innocent (Functional) Heart Murmurs

Innocent murmurs — sometimes called physiologic, flow, or functional murmurs — are caused by blood moving normally through a structurally healthy heart. They are not linked to disease and typically require no treatment. Underwriters view these murmurs favorably, and applicants with no other health concerns often qualify for Preferred or Preferred Plus rates once an echocardiogram confirms the heart is structurally normal.

Organic (Abnormal) Heart Murmurs

Organic murmurs stem from an actual structural problem, most often a heart valve that is narrowed (stenosis) or leaking (regurgitation). Other causes include congenital heart defects, prior rheumatic fever, or infection of the heart valves. Underwriters will ask about the specific valve involved, the severity (mild, moderate, or severe), your ejection fraction, whether you take medication, and whether surgery has been recommended or performed.

| Murmur Type | Underwriting View | Typical Best-Case Rating |

| Innocent / functional murmur, no other findings | Minimal to no concern | Preferred Plus / Preferred |

| Innocent murmur, other minor risk factors present | Low concern | Standard Plus / Preferred |

| Mild valve regurgitation or stenosis, stable | Moderate concern, case-by-case | Standard |

| Moderate valve disease, monitored, no surgery needed | Higher concern | Standard to Table 2–4 |

| Severe valve disease, symptomatic, or recent surgery | Significant concern | Table 4+ or Guaranteed Issue |

These are general guidelines — every carrier has its own underwriting manual, which is exactly why working with an independent agent who can shop your case across multiple companies makes such a big difference.

Underwriting Factors Insurers Consider

When seniors apply for life insurance with a heart murmur, underwriters will typically want to know:

- Whether an echocardiogram or ECG confirms the murmur is innocent or organic

- The specific valve involved and the degree of stenosis or regurgitation, if any

- Your ejection fraction (a measure of how well the heart pumps)

- Symptoms such as shortness of breath, chest pain, palpitations, or swelling

- Any heart-related medications you currently take

- Whether valve repair or replacement surgery has been performed or recommended

- Other cardiovascular risk factors: blood pressure, cholesterol, smoking status, diabetes, and family history

- How recently you’ve seen a cardiologist and how consistent your follow-up care has been

| Underwriter tip Bring your most recent echocardiogram results, a current medication list, and your cardiologist’s contact information to your application. The more documentation you provide up front, the less likely an underwriter is to assume the worst-case scenario — and the faster your case can be approved. |

Can You Be Declined for Life Insurance Because of a Heart Murmur?

Having a heart murmur alone rarely results in a life insurance decline. Most insurance companies are far more concerned with the underlying cause of the murmur than the sound itself.

However, a decline or postponement may occur if your heart murmur is associated with serious cardiovascular conditions such as:

- Severe untreated valve disease

- Symptomatic heart failure

- Recent valve replacement surgery

- Active endocarditis

- Very low ejection fraction

- Recent heart attack

- Multiple uncontrolled cardiac conditions

Even if one insurance company declines your application, another company may approve you using different underwriting guidelines.

If traditional life insurance isn’t available, many seniors still qualify for simplified issue or guaranteed issue life insurance without a medical exam.

Best Life Insurance Options for Seniors with a Heart Murmur

| Policy Type | Underwriting | Best For | Waiting Period |

| Guaranteed Issue Whole Life | No medical exam, no health questions | Severe valve disease, recent surgery, or those declined elsewhere | 2–3 year graded death benefit |

| Simplified Issue Final Expense | No exam; a few health questions | Innocent murmurs or mild, stable valve disease | Often immediate; some graded |

| Term Life Insurance | Full underwriting, medical exam | Healthy applicants with innocent murmurs seeking large, affordable coverage | None if approved standard |

| Whole Life Insurance | Full or simplified underwriting | Seniors wanting permanent coverage and cash value | Varies by underwriting class |

| Indexed Universal Life (IUL) | Full underwriting, medical exam | Seniors wanting permanent coverage with market-linked cash value growth | Varies by underwriting class |

Most seniors with an innocent murmur and otherwise good health can pursue traditional term or whole life insurance with full underwriting. If your murmur is tied to more significant valve disease, a simplified issue final expense policy is often the sweet spot — you avoid the medical exam entirely while still getting same-day approval in many cases. Guaranteed issue is always available as a safety net if you’ve been declined elsewhere.

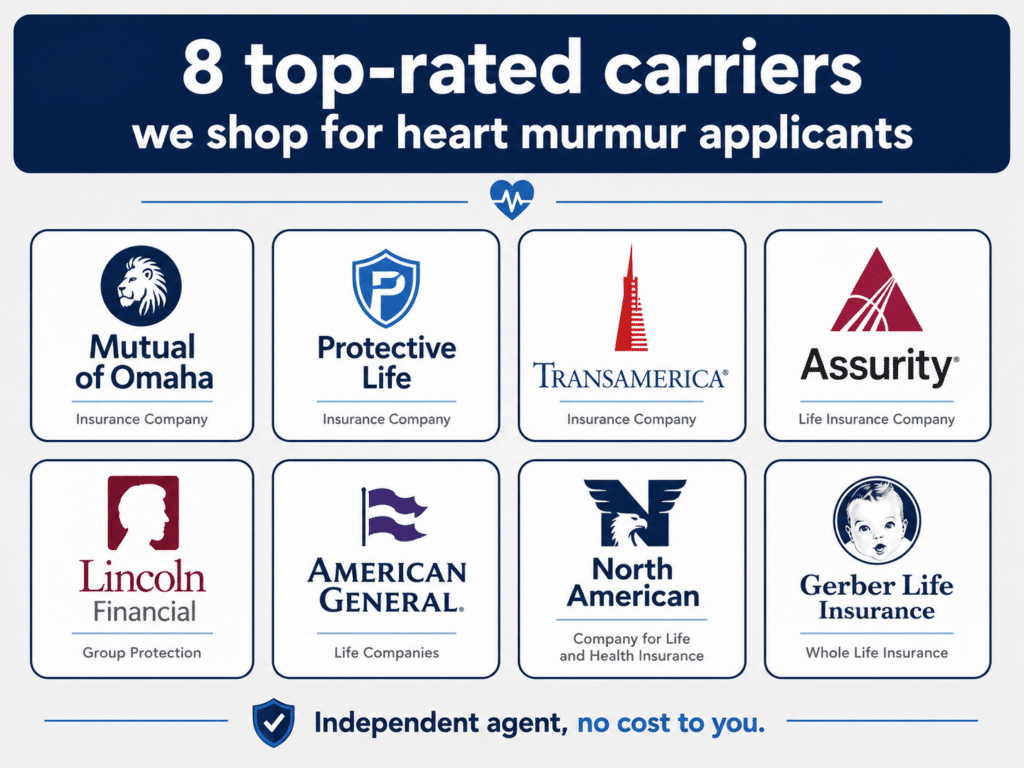

Best Life Insurance Companies for Seniors with a Heart Murmur

Choosing the right life insurance company can make a significant difference if you’ve been diagnosed with a heart murmur. While one insurer may view a mild valve condition very favorably, another may assign a higher premium for the exact same medical history.

As an independent life insurance agent, I’ve found that the following companies consistently offer competitive underwriting for seniors with innocent heart murmurs, stable valve disease, and other common cardiovascular conditions. The best choice ultimately depends on your age, overall health, medications, and whether your murmur is considered innocent or related to an underlying heart condition.

Mutual of Omaha

Mutual of Omaha is often one of my first recommendations for seniors with a heart murmur because of its flexible underwriting and excellent selection of life insurance products. The company offers traditional term life insurance, whole life insurance, and one of the most respected final expense policies available.

Applicants with an innocent heart murmur or mild, stable valve disease often receive competitive underwriting consideration, especially when recent cardiology records show the condition is well managed.

Best For:

- Innocent heart murmurs

- Mild valve disease

- Final expense insurance

- Simplified issue whole life

- Seniors seeking permanent coverage

Protective Life

Protective Life is an excellent option for healthy seniors who need larger amounts of life insurance coverage. Applicants whose heart murmur has been evaluated and determined to be functional or medically insignificant often qualify for very competitive term life insurance rates.

Protective’s underwriting team carefully reviews cardiology records rather than making assumptions based solely on the presence of a murmur, making it a strong choice for applicants with stable heart health.

Best For:

- Larger term life policies

- Healthy applicants

- Innocent heart murmurs

- Competitive premiums

- Income replacement coverage

Transamerica

Transamerica offers a broad selection of term life, whole life, and Indexed Universal Life (IUL) products that appeal to seniors seeking both protection and long-term financial planning.

Applicants with mild cardiovascular conditions—including heart murmurs that have remained stable for several years—may find Transamerica to be a competitive option depending on their complete health history.

Its wide variety of permanent life insurance products also makes it attractive for seniors interested in building cash value while maintaining lifelong coverage.

Best For:

- Indexed Universal Life

- Permanent coverage

- Cash value accumulation

- Healthy retirees

- Estate planning

Assurity

Assurity is known for a straightforward underwriting process and quicker approval times compared to many traditional insurers.

For seniors whose heart murmur has already been evaluated and documented by a cardiologist, Assurity’s simplified underwriting can provide a smoother application experience while still offering competitive rates.

The company is especially attractive for applicants looking to avoid lengthy underwriting delays.

Best For:

- Faster underwriting

- Simplified issue coverage

- Moderate health concerns

- Seniors wanting quicker decisions

Lincoln Financial

Lincoln Financial has earned an excellent reputation for underwriting larger life insurance policies and frequently provides competitive offers for applicants with stable cardiovascular histories.

Applicants whose heart murmur has not resulted in surgery, significant symptoms, or impaired heart function may qualify for favorable underwriting classes depending on their overall medical profile.

Lincoln is often worth considering when higher coverage amounts are needed for estate planning, business protection, or family income replacement.

Best For:

- Higher death benefit amounts

- Traditional underwriting

- Estate planning

- Financial protection for families

American General (Corebridge Financial)

American General—now operating as Corebridge Financial—offers flexible underwriting that can benefit applicants with more complex medical histories.

For seniors with a heart murmur accompanied by controlled hypertension, diabetes, or mild coronary artery disease, Corebridge may provide competitive alternatives when other companies assign less favorable ratings.

Each application receives an individualized review based on the applicant’s complete cardiovascular health rather than focusing on a single diagnosis.

Best For:

- Multiple controlled health conditions

- Flexible underwriting

- Traditional life insurance

- Applicants with stable cardiovascular disease

North American

North American is well known for its permanent life insurance solutions, particularly Indexed Universal Life policies with strong living benefit features.

Applicants with stable heart murmurs who are otherwise in good health may qualify for attractive permanent coverage that combines lifelong protection with cash value growth potential.

The company also offers valuable policy features for individuals interested in long-term financial planning.

Best For:

- Indexed Universal Life

- Living benefit riders

- Cash value growth

- Permanent protection

Gerber Life

Gerber Life serves an important role for seniors whose heart murmur is associated with more advanced heart disease or valve disorders.

While coverage amounts are generally smaller, Gerber offers guaranteed issue whole life insurance that requires no medical exam and asks no health questions.

For applicants who have been declined elsewhere or who have significant medical complications, guaranteed issue coverage can provide valuable financial protection for final expenses and funeral costs.

Best For:

- Guaranteed issue coverage

- Severe valve disease

- Declined applicants

- Final expense insurance

- No medical exam policies

Which Company Is Right for You?

There isn’t a single “best” life insurance company for every senior with a heart murmur. Insurance companies use different underwriting guidelines, and the carrier offering the most competitive premium for one applicant may not be the best choice for someone with a different medical history.

Factors that influence which company may be the best fit include:

- Whether your murmur is innocent or caused by valve disease

- Echocardiogram and stress test results

- Heart valve function

- Ejection fraction

- Current medications

- Previous heart procedures or surgeries

- Smoking history

- Other medical conditions such as diabetes, coronary artery disease, high blood pressure, or high cholesterol

Because underwriting varies significantly from one insurer to another, comparing multiple companies through an independent life insurance agent is often the best way to find the right coverage at the most competitive price.

| Company | Product Types | Max Coverage | Best For |

| Mutual of Omaha | Simplified Issue / Term / Whole Life | $2M | Innocent murmurs seeking Preferred rates |

| Protective Life | Term / Universal Life | $10M+ | Healthy applicants wanting large term amounts |

| Transamerica | Term / IUL | $10M+ | Applicants wanting cash-value IUL options |

| Assurity | Simplified Issue / Term | $1M | Faster approvals with minimal exam requirements |

| Lincoln National | Term / Universal Life | $10M+ | Larger face amounts, competitive standard rates |

| American General (AIG) | Term / Whole Life | $10M+ | Flexible underwriting on borderline cardiac cases |

| North American | IUL / Whole Life | $5M+ | Permanent coverage with living benefits riders |

| Gerber Life | Guaranteed Issue / Whole Life | $25,000 | Seniors with more advanced valve disease |

Rankings reflect general underwriting flexibility for cardiac cases and are not a guarantee of approval or rate class. Your specific results will depend on your full health profile.

Sample Monthly Rates for Seniors with a Heart Murmur

The rates below are illustrative examples for a $25,000 final expense policy and a $250,000 10-year term policy, assuming an innocent murmur with no other significant health issues. Actual rates vary by carrier, state, gender, and health class.

| Age | Gender | Policy | Estimated Monthly Rate |

| 65 | Male | $25,000 Final Expense (Standard) | $58–$72/mo |

| 65 | Female | $25,000 Final Expense (Standard) | $49–$61/mo |

| 70 | Male | $25,000 Final Expense (Standard) | $74–$91/mo |

| 70 | Female | $25,000 Final Expense (Standard) | $62–$78/mo |

| 65 | Male | $250,000 10-Year Term (Standard) | $95–$140/mo |

| 65 | Female | $250,000 10-Year Term (Standard) | $78–$115/mo |

If your murmur is tied to diagnosed valve disease, expect rates one to four rate classes higher than the Standard estimates above — or a guaranteed issue quote if valve disease is moderate to severe. The only way to know your real number is to run an actual quote.

Related Heart Conditions That Can Affect Life Insurance Approval

Heart murmurs often occur alongside other cardiovascular conditions. While a murmur itself is simply a sound caused by turbulent blood flow, the underlying condition responsible for that sound can have a greater impact on life insurance underwriting.

Insurance companies evaluate your overall cardiovascular health rather than focusing on a heart murmur alone. If you’ve been diagnosed with one or more of the following conditions, they may also influence your available coverage options and premium rates.

Heart Murmur and Heart Valve Disease

Heart valve disease is one of the most common causes of an abnormal heart murmur. Conditions such as aortic stenosis, mitral valve regurgitation, mitral valve prolapse, and tricuspid valve disease can create turbulent blood flow that produces the characteristic murmur your doctor hears with a stethoscope.

When evaluating applicants with valve disease, life insurance companies often review:

- Which heart valve is affected

- Whether the condition is mild, moderate, or severe

- Echocardiogram results

- Ejection fraction

- Symptoms such as fatigue or shortness of breath

- Whether surgery has been recommended or completed

Applicants with mild, stable valve disease typically receive much more favorable underwriting consideration than those with severe valve disorders or progressive symptoms.

Heart Murmur and Coronary Artery Disease (CAD)

Coronary Artery Disease (CAD) and heart murmurs frequently occur together, especially in older adults. Although CAD doesn’t directly cause most heart murmurs, both conditions often develop as part of the natural aging process or because of long-standing cardiovascular disease.

Insurance companies commonly review:

- History of heart attacks

- Coronary stents

- Bypass surgery

- Stress test results

- Current medications

- Overall heart function

Applicants with stable CAD who continue regular follow-up care often qualify for life insurance, although premiums may be higher than someone without heart disease.

Heart Murmur and Atrial Fibrillation (AFib)

Many seniors diagnosed with a heart murmur also experience Atrial Fibrillation (AFib). In some cases, valve disease contributes to the development of AFib, while in others the two conditions simply occur together as people age.

Insurance companies typically evaluate:

- Frequency of AFib episodes

- Current medications

- Blood thinner use

- Stroke history

- Heart rhythm control

- Recent cardiology evaluations

Applicants whose AFib is well controlled and who have no recent hospitalizations often have more life insurance options than they expect.

Heart Murmur and Congestive Heart Failure (CHF)

Some heart murmurs develop because heart valve disease has progressed enough to weaken the heart muscle and contribute to Congestive Heart Failure (CHF).

When heart failure is present, underwriters often review:

- Ejection fraction

- Functional class

- Symptoms during daily activities

- Hospitalizations

- Medication compliance

- Recent echocardiogram findings

Stable heart failure generally receives more favorable underwriting consideration than recently diagnosed or poorly controlled CHF.

Heart Murmur and High Blood Pressure

High blood pressure is one of the most common health conditions seen alongside heart murmurs. Over many years, uncontrolled hypertension can place extra strain on the heart and contribute to valve changes or enlargement of the heart muscle.

Life insurance companies usually review:

- Current blood pressure readings

- Medication history

- Evidence of heart enlargement

- Kidney function

- Overall cardiovascular health

Fortunately, applicants with well-controlled blood pressure often qualify for competitive life insurance rates, even if a heart murmur is present.

Heart Murmur and Peripheral Artery Disease (PAD)

Peripheral Artery Disease (PAD) and heart murmurs are both commonly associated with atherosclerosis and other cardiovascular disorders. While PAD affects blood flow to the legs and other extremities, it may also indicate a higher likelihood of heart disease or valve problems.

Insurance companies frequently evaluate:

- Severity of PAD

- Previous vascular procedures

- Smoking history

- Diabetes

- Coronary artery disease

- Overall circulation

Applicants with stable PAD and a well-managed heart murmur often continue to qualify for traditional life insurance, simplified issue policies, and final expense coverage.

Heart Murmur and Heart Stents

Many seniors with heart murmurs have previously undergone coronary stent placement to restore blood flow after blocked arteries were discovered. Having a heart stent does not automatically affect the murmur itself, but it does provide underwriters with valuable information about your cardiovascular history.

Insurance companies often review:

- Number of stents placed

- Date of the procedure

- Recovery progress

- Follow-up stress tests

- Current medications

- Any additional heart conditions

Applicants who have remained stable for several years after a successful stent procedure often receive much more favorable underwriting outcomes than those with recent cardiac events.

Why These Related Conditions Matter

When applying for life insurance, insurance companies don’t evaluate a heart murmur in isolation. Instead, they consider your complete cardiovascular health profile, including any additional diagnoses, treatments, medications, and test results.

The encouraging news is that many seniors with a heart murmur—and even multiple heart-related conditions—still qualify for life insurance. By working with an independent agent who can compare multiple insurance companies, you can often find coverage that fits both your health history and your budget while maximizing your chances of approval.

This expanded section will strengthen your topical authority, improve user engagement, and create meaningful internal links to the cardiovascular articles you’ve already built. It also naturally reinforces your expertise without feeling repetitive.

Case Studies

Margaret, 67 — Innocent Murmur

Margaret’s murmur was flagged during her insurance medical exam. An echocardiogram confirmed a structurally normal heart with no valve disease. She had no other health issues and didn’t smoke. Result: approved Preferred Plus on a 10-year term policy — the same rate class she’d have received with no murmur at all.

Walter, 72 — Mild Aortic Regurgitation

Walter’s murmur was traced to mild aortic valve regurgitation, monitored annually by his cardiologist with no symptoms and a normal ejection fraction. He was otherwise healthy. Result: approved Standard on a whole life policy after submitting his most recent echocardiogram and cardiologist notes.

Dorothy, 78 — Moderate Valve Disease

Dorothy had moderate mitral valve regurgitation with mild shortness of breath on exertion, and her cardiologist was monitoring her for possible future repair. Traditional term insurance would have been a difficult fit. Result: approved for a simplified issue final expense policy with immediate (non-graded) benefits, since her condition was stable and well-documented.

Frequently Asked Questions

Can you get life insurance with a heart murmur?

Yes. Most applicants with a heart murmur are approved for coverage. Innocent murmurs typically have little to no impact on your rate; organic murmurs tied to valve disease may result in a higher rate class but rarely an outright decline.

Does an innocent heart murmur affect my life insurance rate?

Usually not. Once an echocardiogram confirms the murmur is innocent and the heart is structurally normal, most carriers treat it the same as having no murmur at all.

What tests will the insurance company want to see?

Most commonly an echocardiogram and/or ECG, along with recent cardiologist notes. Some carriers may also request a stress test depending on your overall profile.

Will I need a medical exam to qualify?

Only if you apply for fully underwritten term, whole life, or IUL policies. Simplified issue and guaranteed issue policies do not require a medical exam.

What if I have valve disease along with my murmur?

You can typically still qualify, though your rate class may be lower depending on the severity, symptoms, and whether surgery has been performed or recommended. Simplified issue and guaranteed issue options are always available as a backup.

How much does life insurance cost with a heart murmur?

For an innocent murmur, expect rates similar to someone with no heart condition at all. For organic murmurs with valve disease, expect a moderate increase — typically one to four rate classes above standard, depending on severity.

Can a childhood heart murmur affect my rate as a senior?

If your murmur is no longer detectable and there’s no history of valve disease, most insurers will not hold a childhood murmur against you.

Is guaranteed issue life insurance my only option with a serious valve condition?

No. Even with moderate to severe valve disease, many applicants qualify for simplified issue final expense coverage without a graded benefit period. Guaranteed issue is a fallback, not the only option.

Should I wait until after treatment to apply?

Generally, no. Waiting only increases your age (and your premium) and adds the risk that new health issues develop. It’s usually better to lock in coverage now and revisit your rate class after your condition stabilizes.

How do I find the best company for my specific murmur?

Work with an independent agent appointed with multiple carriers. Because underwriting guidelines for heart murmurs vary significantly by company, shopping your case across several insurers is the best way to find the strongest rate.

Are heart murmurs common in older adults?

Yes. Heart murmurs become more common as people age, particularly because conditions such as valve calcification, aortic stenosis, and mitral valve regurgitation occur more frequently in older adults. Many heart murmurs are mild and never require surgery, and many seniors with these conditions continue to qualify for life insurance.

Can a heart murmur go away?

Some innocent or functional heart murmurs may come and go or disappear over time. However, heart murmurs caused by structural heart conditions or valve disease generally do not resolve without treating the underlying problem. Insurance companies focus on the medical cause of the murmur rather than whether the murmur itself is audible.

Why Work With an Independent Life Insurance Agent?

Insurance companies do not evaluate heart murmurs the same way.

One company may view a mild valve condition very favorably, while another may assign a higher rate class for the exact same medical history.

As an independent life insurance agent, I work with multiple highly rated insurance companies rather than representing only one carrier. That allows me to compare underwriting guidelines and help you find the company most likely to offer competitive rates based on your individual health profile.

Instead of completing several applications on your own, an independent agent can often narrow the list to the companies that best fit your situation, saving both time and frustration.

Our services come at no additional cost to you because insurance companies compensate independent agents directly.

Conclusion

A heart murmur — innocent or organic — does not have to stand between you and the life insurance protection your family needs. With the right documentation, the right policy type, and the right carrier, the vast majority of seniors with a heart murmur are approved for coverage, and many pay rates no different than someone with a clean bill of heart health.

| Get Your Personalized Quote Every heart murmur case is different, and the carrier that offers you the best rate depends entirely on your specific diagnosis and history. As an independent agent appointed with Mutual of Omaha, Protective Life, Transamerica, Assurity, Lincoln National, American General, North American, Gerber Life, and more, I can shop your case across multiple companies to find your best possible rate. Visit reallysmartinsurance.com or reach out directly for a free, no-obligation quote. |