Life Insurance for Seniors with Peripheral Artery Disease (PAD): What You Need to Know

Posted in Life Insurance w/ Pre-existing Conditions on June 23, 2026 last updated on June 23, 2026

Posted in Life Insurance w/ Pre-existing Conditions on June 23, 2026 last updated on June 23, 2026

Is Life Insurance for Seniors with Peripheral Artery Disease Possible?

Yes, seniors with Peripheral Artery Disease (PAD) can often qualify for life insurance. While PAD is considered a cardiovascular condition and may affect premiums, many applicants are approved for traditional life insurance, simplified issue policies, final expense coverage, and guaranteed issue life insurance.

Approval depends on the severity of the disease, overall cardiovascular health, and whether other medical conditions are present.

Receiving a diagnosis of Peripheral Artery Disease can be concerning, especially when applying for life insurance. Many seniors assume that because PAD affects circulation and is linked to heart disease, they will automatically be declined.

Fortunately, that is rarely the case.

Many insurance companies routinely approve applicants with PAD. The key factors are how severe the condition is, whether it is stable, and what other health conditions are present.

Insurance companies understand that PAD is common among older adults and often develops gradually over many years. While it is considered a cardiovascular risk factor, it does not automatically prevent someone from obtaining life insurance coverage.

The challenge is finding the insurance company whose underwriting guidelines are most favorable toward cardiovascular conditions.

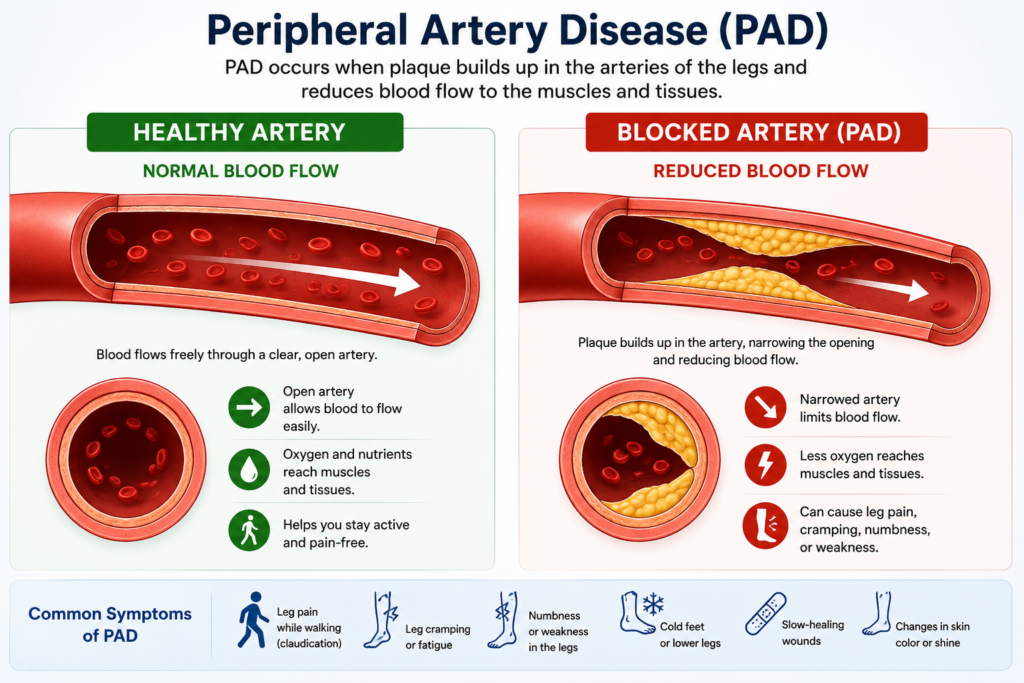

What Is Peripheral Artery Disease?

Peripheral Artery Disease occurs when plaque accumulates inside arteries outside of the heart and brain, most commonly affecting the legs.

As plaque builds up, blood flow becomes restricted, reducing oxygen delivery to muscles and tissues.

Many seniors first notice symptoms when walking.

Common symptoms include:

- Leg pain while walking (claudication)

- Leg cramping

- Fatigue in the legs

- Numbness

- Weakness

- Cold feet or lower legs

- Slow-healing wounds

- Changes in skin color

Some people have no symptoms at all and discover the condition during routine medical testing.

PAD is most commonly caused by atherosclerosis, the same disease process responsible for:

- Coronary artery disease

- Heart attacks

- Stroke

- Carotid artery disease

Because of this connection, insurance companies frequently evaluate PAD alongside other cardiovascular conditions.

Why Does Peripheral Artery Disease Matter to Life Insurance Companies?

Insurance companies are not necessarily worried about PAD itself.

Instead, they are evaluating what PAD may indicate about your overall cardiovascular health.

Studies have shown that PAD can increase the likelihood of:

- Heart attacks

- Stroke

- Coronary artery disease

- Future vascular procedures

- Cardiovascular complications

For this reason, underwriters often view PAD as part of a larger cardiovascular picture.

When reviewing an application, insurers typically ask:

- How severe is the PAD?

- Has the condition progressed?

- Have vascular procedures been required?

- Are symptoms stable?

- Are additional cardiovascular diseases present?

Applicants with mild, stable PAD generally receive better consideration than those with severe disease progression or multiple recent procedures.

The good news is that many applicants with PAD continue to qualify for life insurance coverage because insurers focus heavily on stability and treatment success.

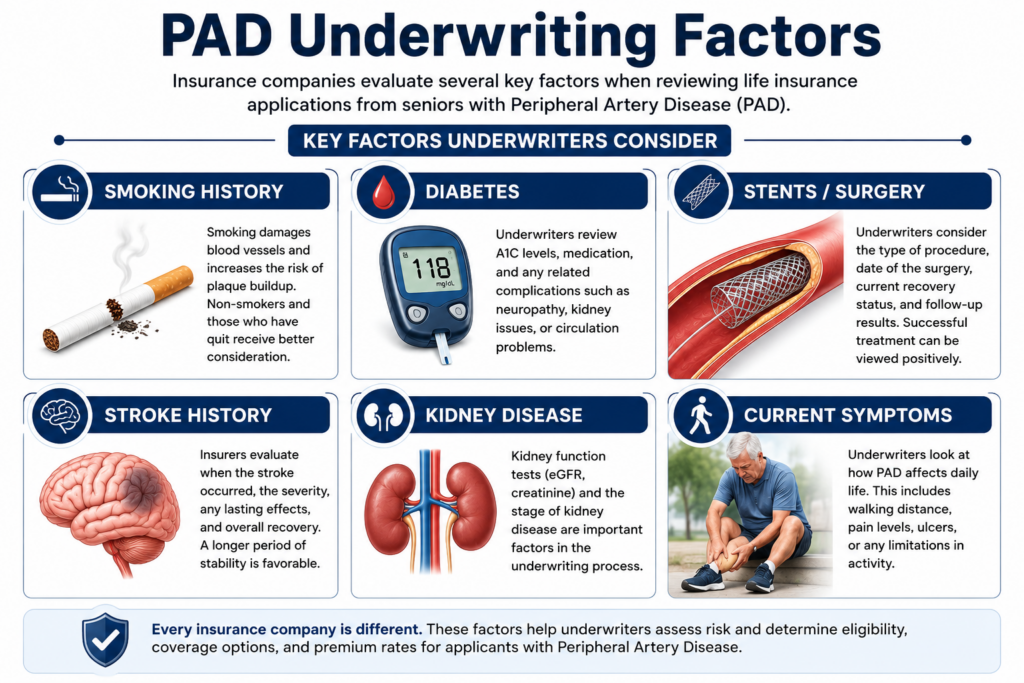

How Insurance Companies Evaluate PAD

Every life insurance company uses its own underwriting guidelines, but most carriers evaluate similar factors.

Date of Diagnosis

Insurance companies generally prefer conditions that have remained stable over time.

A diagnosis made several years ago with little progression often receives more favorable consideration than a recent diagnosis with rapidly worsening symptoms.

Severity of Symptoms

Underwriters want to know how PAD affects your daily life.

Questions often include:

- Can you walk normally?

- How far can you walk before symptoms occur?

- Are symptoms improving or worsening?

- Have ulcers developed?

Mild symptoms generally produce more favorable underwriting outcomes.

Vascular Procedures

Many PAD patients eventually undergo procedures designed to improve circulation.

Common procedures include:

- Angioplasty

- Peripheral artery stents

- Atherectomy

- Bypass surgery

Insurance companies often view successful treatment positively because it demonstrates active medical management.

Smoking History

Smoking remains one of the most significant risk factors associated with PAD.

Applicants who currently smoke often face higher premiums than non-smokers.

Former smokers who have quit for several years may receive substantially better consideration.

Medications

Underwriters review medications to understand how the condition is being managed.

Common medications include:

- Statins

- Blood thinners

- Aspirin therapy

- Blood pressure medications

- Cholesterol medications

Medication compliance is generally viewed positively.

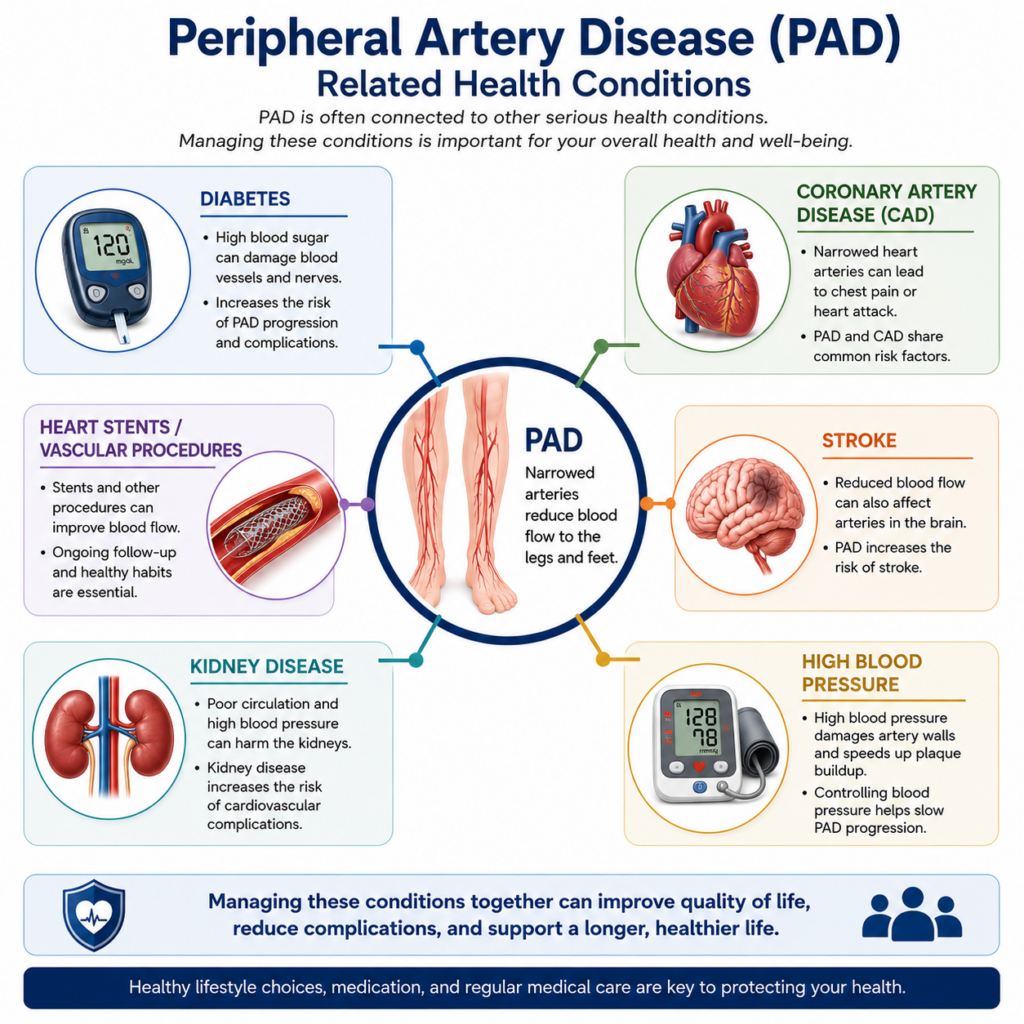

Other Medical Conditions

This is frequently the most important underwriting factor.

Insurance companies often evaluate whether PAD exists alongside:

- Coronary artery disease

- Heart attack history

- Stroke history

- Diabetes

- Kidney disease

- Congestive heart failure

- High blood pressure

The overall health picture typically matters more than PAD alone.

Can You Be Declined for Life Insurance with Peripheral Artery Disease?

Yes.

However, PAD itself is rarely the sole reason for a decline.

Insurance companies are more likely to decline applicants when severe PAD is accompanied by significant cardiovascular complications or evidence of advanced disease progression.

Potential concerns include:

- Multiple vascular surgeries

- Active smoking

- Recent stroke

- Severe coronary artery disease

- Congestive heart failure

- Recent amputations

- Dialysis

- Progressive circulation problems

Even when traditional life insurance is unavailable, other options often remain.

Many seniors who are declined for traditional coverage successfully obtain:

- Simplified issue life insurance

- Final expense insurance

- Guaranteed issue life insurance

A decline from one company should never be viewed as a final answer because different insurers evaluate cardiovascular risk differently.

Best Life Insurance Options for Seniors with Peripheral Artery Disease

Traditional Term Life Insurance

Term life insurance provides coverage for a specific period, such as 10, 15, or 20 years.

Coverage amounts may range from $100,000 to over $1 million depending on age and health.

Traditional term life insurance generally works best for:

- Mild PAD

- Stable cardiovascular health

- No recent vascular procedures

- Good overall health

Because full underwriting is required, insurance companies will carefully review medical records and cardiovascular history.

Term life insurance often provides the largest death benefit for the lowest premium when applicants qualify.

Traditional Whole Life Insurance

Whole life insurance provides permanent coverage that never expires as long as premiums are paid.

In addition to the death benefit, whole life policies build cash value over time.

Whole life insurance may be attractive for seniors who:

- Want lifelong protection

- Need estate planning solutions

- Prefer guaranteed coverage

- Value cash value accumulation

Although premiums are higher than term insurance, coverage remains permanent.

Universal Life Insurance

Universal life insurance provides flexibility in both premium payments and death benefits.

Many seniors use universal life policies when seeking permanent coverage with additional financial planning opportunities.

Applicants with stable PAD and favorable overall health may qualify for universal life insurance, although underwriting requirements can be more extensive.

Simplified Issue Life Insurance

Simplified issue policies require health questions but no medical exam.

Coverage amounts typically range from:

- $5,000

- $10,000

- $25,000

- $50,000

These policies often appeal to seniors who want:

- Faster approval

- No blood work

- No medical exam

- Permanent coverage

Many PAD applicants find simplified issue coverage easier to obtain than fully underwritten policies.

Final Expense Insurance

Final expense insurance is designed to help cover:

- Funeral costs

- Burial expenses

- Final medical bills

- Outstanding debts

Coverage amounts generally range from $5,000 to $50,000.

Many final expense companies are comfortable working with seniors who have cardiovascular conditions, making these policies a popular choice among PAD applicants.

Guaranteed Issue Life Insurance

Guaranteed issue life insurance is the easiest policy type to qualify for.

There are:

- No health questions

- No medical exams

- No underwriting interviews

Approval is virtually guaranteed for all applicants.

While premiums are higher and death benefits are usually smaller, guaranteed issue coverage can provide an important safety net for seniors with severe health concerns.

Guaranteed Issue vs. Simplified Issue Life Insurance

Many seniors with PAD are unsure whether guaranteed issue or simplified issue life insurance is the better option.

Simplified issue policies ask health questions but typically do not require a medical exam. Because underwriting is still involved, premiums are usually lower and coverage amounts are often higher.

Guaranteed issue policies do not ask health questions and do not require a medical exam. Approval is virtually guaranteed, but premiums are generally higher and death benefits are often smaller.

For most seniors with stable PAD, simplified issue coverage is usually the better option if they can qualify. Guaranteed issue coverage is often best reserved for applicants with severe health concerns or prior declines.

| Feature | Simplified Issue | Guaranteed Issue |

|---|---|---|

| Health Questions | Yes | No |

| Medical Exam | No | No |

| Approval Speed | Fast | Immediate |

| Coverage Amounts | Higher | Lower |

| Premiums | Lower | Higher |

| Best For | Moderate Health Issues | Severe Health Issues |

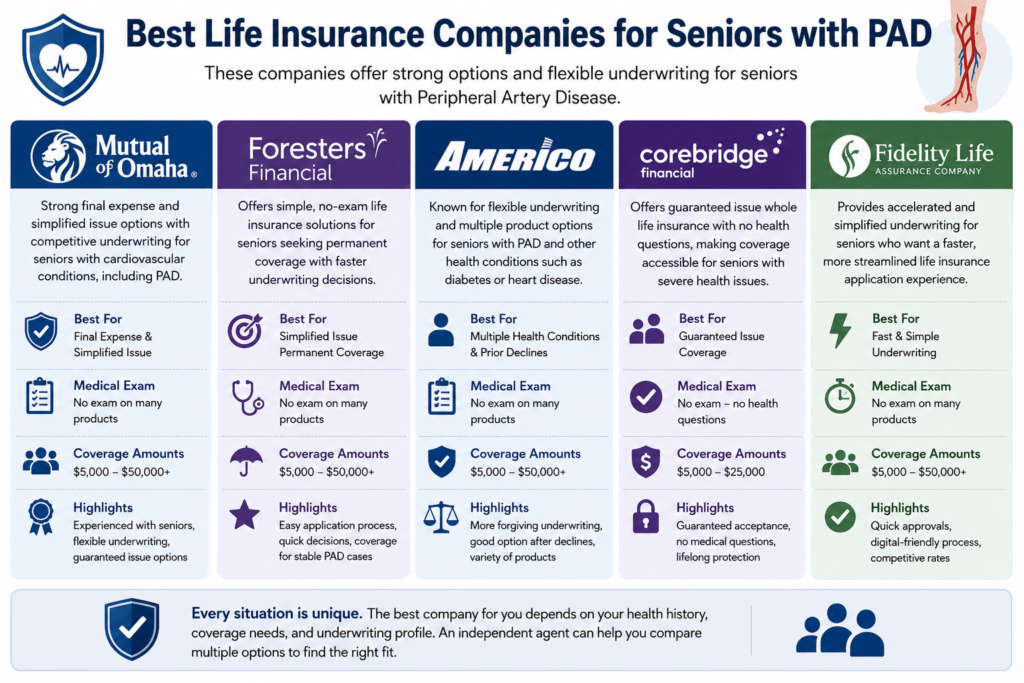

Best Life Insurance Companies for Seniors with Peripheral Artery Disease

Not all life insurance companies evaluate Peripheral Artery Disease the same way. Some carriers are more comfortable with cardiovascular conditions and vascular procedures, while others apply stricter underwriting guidelines.

Finding the right company can make a significant difference in both approval opportunities and premium costs.

Mutual of Omaha

Mutual of Omaha remains one of the strongest choices for seniors seeking final expense insurance and simplified issue coverage.

The company has extensive experience working with older adults who have common cardiovascular conditions, including PAD, diabetes, high blood pressure, and coronary artery disease.

Many seniors appreciate Mutual of Omaha because:

- Simplified application process

- Strong final expense products

- Guaranteed issue options available

- Competitive underwriting for stable health conditions

For applicants seeking smaller coverage amounts and permanent protection, Mutual of Omaha is often one of the first companies worth considering.

Foresters Financial

Foresters Financial offers several simplified issue products that can be attractive for seniors who want to avoid a medical exam.

Applicants with stable PAD and no recent major cardiovascular events may find Foresters to be a competitive option.

Benefits include:

- No medical exam on many products

- Faster underwriting decisions

- Permanent life insurance options

- Competitive rates for certain health profiles

Foresters can be especially appealing for seniors seeking straightforward coverage with less underwriting complexity.

Americo

Americo is frequently considered when applicants have multiple health conditions in addition to PAD.

Because many seniors with PAD also manage diabetes, hypertension, heart disease, or previous vascular procedures, Americo’s underwriting flexibility can be valuable.

The company offers:

- Final expense coverage

- Simplified issue products

- Coverage for moderate health impairments

- Flexible underwriting options

Applicants who have been declined elsewhere may still find opportunities through Americo’s product lineup.

Corebridge Financial

Corebridge Financial is well known for guaranteed issue life insurance.

For seniors with severe PAD, previous declines, multiple surgeries, or significant cardiovascular complications, guaranteed issue coverage may be one of the most accessible options available.

Benefits include:

- No health questions

- No medical exam

- Guaranteed acceptance for eligible ages

- Permanent whole life protection

Although premiums are higher, guaranteed issue coverage can provide valuable financial protection when other options are unavailable.

Fidelity Life

Fidelity Life focuses on accelerated underwriting and simplified approval processes.

Applicants with stable PAD who want a quicker application experience may find Fidelity Life attractive.

The company often appeals to seniors who:

- Prefer avoiding medical exams

- Need coverage quickly

- Have relatively stable health histories

- Want streamlined underwriting

Which Company Is Best?

There is no single best company for every senior with PAD.

Insurance companies often evaluate:

- Severity of PAD

- Smoking history

- Diabetes

- Coronary artery disease

- Stroke history

- Kidney disease

- Vascular procedures

- Overall cardiovascular health

The best company for one applicant may not be the best company for another.

This is one reason why comparing multiple carriers through an independent agent often produces better results than applying directly with a single company.

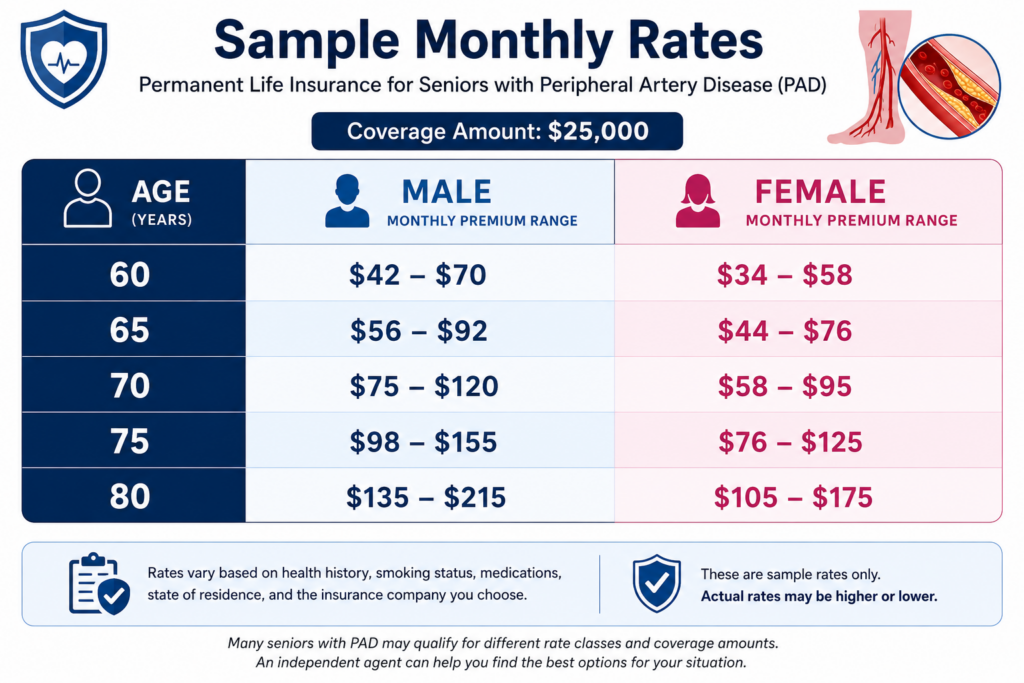

Sample Monthly Rates for Seniors with Peripheral Artery Disease

The following examples illustrate approximate monthly premiums for seniors seeking $25,000 of permanent life insurance coverage.

Actual rates vary based on:

- Age

- Gender

- State

- Smoking status

- Severity of PAD

- Other health conditions

- Insurance company selected

| Age | Male | Female |

|---|---|---|

| 60 | $42–$70 | $34–$58 |

| 65 | $56–$92 | $44–$76 |

| 70 | $75–$120 | $58–$95 |

| 75 | $98–$155 | $76–$125 |

| 80 | $135–$215 | $105–$175 |

Applicants who qualify for traditional underwriting may obtain larger coverage amounts at different premium levels.

Peripheral Artery Disease and Diabetes

Diabetes and Peripheral Artery Disease frequently occur together. In fact, diabetes is one of the leading contributors to PAD because elevated blood sugar levels can damage blood vessels and accelerate plaque buildup.

When insurance companies evaluate applicants with both conditions, they often review:

- A1C levels

- Current medications

- Neuropathy

- Kidney function

- Diabetic ulcers

- Circulation problems

Applicants whose diabetes is well controlled generally receive more favorable underwriting consideration than those experiencing significant complications.

The encouraging news is that many seniors with both diabetes and PAD successfully qualify for life insurance coverage every year.

While premiums may be higher than average, coverage is often available through traditional underwriting, simplified issue policies, and final expense insurance.

Peripheral Artery Disease and Coronary Artery Disease

PAD and Coronary Artery Disease are closely connected because both conditions are caused by atherosclerosis.

Many seniors diagnosed with PAD also have some degree of coronary artery disease.

Insurance companies often evaluate:

- Number of blocked arteries

- Previous stents

- Bypass surgery history

- Heart attack history

- Current symptoms

- Stress test results

Stable coronary artery disease generally receives more favorable underwriting consideration than recent cardiac events.

Many applicants with both PAD and CAD continue to qualify for life insurance, particularly when both conditions have remained stable for several years.

Peripheral Artery Disease and Heart Stents

Many seniors with PAD undergo stent procedures designed to improve circulation.

Insurance companies often evaluate:

- Number of stents

- Date of procedure

- Recovery progress

- Follow-up testing

- Additional cardiovascular conditions

Successful stent placement can actually improve underwriting outcomes because it demonstrates that circulation problems have been identified and treated.

Applicants who have remained stable after a stent procedure frequently receive better consideration than those with untreated circulation issues.

Peripheral Artery Disease and Stroke

Because PAD is considered a systemic vascular disease, underwriters often review stroke history carefully.

Questions frequently include:

- When did the stroke occur?

- Were there lasting neurological effects?

- Has recovery been successful?

- Have additional strokes occurred?

Applicants who experienced a stroke several years ago and have remained medically stable generally receive better consideration than those with recent events.

Many seniors with both PAD and stroke history still qualify for life insurance, although premiums may be higher.

Peripheral Artery Disease and Kidney Disease

PAD and kidney disease often occur together because both conditions share common risk factors such as diabetes, hypertension, and vascular disease.

Insurance companies frequently review:

- eGFR results

- Creatinine levels

- Dialysis history

- Progression of kidney disease

- Overall cardiovascular health

Mild to moderate kidney disease generally receives more favorable consideration than advanced kidney failure.

Many seniors with stable kidney disease and PAD continue to qualify for life insurance coverage.

Peripheral Artery Disease and High Blood Pressure

High blood pressure is one of the most common risk factors associated with PAD.

Over time, uncontrolled hypertension can damage artery walls and accelerate plaque buildup.

Insurance companies often review:

- Current blood pressure readings

- Medication compliance

- Evidence of organ damage

- Overall cardiovascular health

Applicants whose blood pressure remains well controlled generally receive more favorable underwriting outcomes.

Stable hypertension by itself rarely prevents life insurance approval.

Peripheral Artery Disease and Smoking

Smoking is one of the strongest risk factors associated with Peripheral Artery Disease. In fact, many PAD diagnoses are directly linked to long-term tobacco use because smoking damages blood vessels, accelerates plaque buildup, and reduces circulation throughout the body.

Because of this connection, insurance companies pay close attention to an applicant’s smoking history.

Underwriters often review:

- Whether you currently smoke

- How long ago you quit

- Amount previously smoked

- Use of cigars, vaping products, or smokeless tobacco

- Progression of PAD since quitting

Current smokers with PAD typically receive higher premiums than non-smokers because the combination significantly increases cardiovascular risk.

The good news is that many insurance companies reward former smokers. Applicants who have successfully quit smoking and remained tobacco-free for several years often receive substantially better underwriting consideration than current smokers.

If you have PAD and a smoking history, working with an independent agent can help identify carriers that are more favorable toward former tobacco users.

Underwriting Severity Table

The following table illustrates how life insurance underwriters may view various PAD-related situations.

| Situation | Typical Underwriting Outlook |

|---|---|

| Mild PAD, No Symptoms | Favorable |

| PAD Controlled with Medication | Favorable |

| PAD + Diabetes | Moderate |

| PAD + Coronary Artery Disease | Moderate |

| PAD + Heart Stents | Moderate |

| PAD + Previous Stroke | Challenging |

| Multiple Vascular Procedures | Challenging |

| Recent Amputation | Often Postponed or Declined |

| Severe PAD with Ongoing Complications | High Risk |

This table is intended for educational purposes only. Every insurance company evaluates risk differently, and individual underwriting decisions vary.

Real-Life Examples

Approved with Mild Peripheral Artery Disease

Susan was diagnosed with mild PAD at age 68 after mentioning occasional leg discomfort during her annual physical. Further testing revealed reduced circulation in her legs, but she remained active, exercised regularly, and followed her physician’s recommendations.

Because her symptoms were mild and she had no history of heart attack, stroke, or major vascular procedures, she qualified for a traditional whole life insurance policy with a moderate health rating.

Her experience demonstrates that many seniors with stable PAD can still qualify for traditional life insurance coverage.

Approved After Peripheral Stent Placement

Robert, age 73, underwent a peripheral artery stent procedure after a blockage was discovered in one of the arteries supplying blood to his leg. Following treatment, his circulation improved significantly and he experienced no additional complications.

Two years later, he applied for life insurance and was approved for a simplified issue whole life policy. Because his condition had remained stable and his physician records showed positive follow-up results, the insurance company viewed his situation favorably.

His case highlights an important point: successful treatment can sometimes improve underwriting outcomes compared to untreated disease.

Declined Traditional Coverage but Approved for Final Expense

James, age 81, had advanced PAD, diabetes, coronary artery disease, and a previous stroke. Because of his overall health profile, he was declined for a traditional life insurance policy.

Rather than giving up, he applied for final expense insurance and secured coverage designed specifically for seniors with health concerns.

Although the death benefit was smaller than a traditional policy, it provided meaningful financial protection to help his family cover funeral costs, final medical expenses, and other end-of-life obligations.

His experience illustrates that a decline from one type of policy does not mean coverage is unavailable.

Why Work With an Independent Life Insurance Agent?

One of the biggest mistakes seniors make after being diagnosed with PAD is applying directly with a single insurance company.

The challenge is that every insurer evaluates cardiovascular conditions differently. One company may be cautious about a previous vascular procedure, while another may focus primarily on your current health and stability.

Independent life insurance agents work with multiple insurance carriers rather than representing only one company.

Benefits of working with an independent agent include:

- Access to multiple insurance companies

- Guidance on carrier underwriting preferences

- Help comparing rates and coverage options

- Assistance navigating medical questions

- Better opportunities for approval

- No additional cost for professional assistance

For seniors with PAD, choosing the right company can be just as important as choosing the right policy.

An experienced independent agent can often identify opportunities that applicants may overlook when applying on their own.

Frequently Asked Questions

Can I get life insurance with Peripheral Artery Disease?

Yes. Many seniors with PAD successfully qualify for life insurance. Approval depends on the severity of the condition, overall cardiovascular health, smoking history, and the presence of additional medical conditions.

Not always. Mild, stable PAD may have only a moderate impact on premiums. More severe cases typically receive higher rates because of increased cardiovascular risk.

Can I qualify for life insurance after a peripheral artery stent?

Yes. Many applicants obtain coverage after a successful stent procedure. Insurance companies generally want to see a stable recovery and no significant complications following treatment.

Can smokers with PAD get life insurance?

Yes, but premiums are often substantially higher. Smoking remains one of the largest risk factors associated with PAD and cardiovascular disease.

What if I’ve already been declined?

A decline from one company does not mean every company will decline you. Different insurers use different underwriting guidelines. Final expense and guaranteed issue life insurance may also be available.

What is the easiest life insurance policy to qualify for?

Guaranteed issue whole life insurance is typically the easiest policy to obtain because there are no health questions and no medical exams.

Can I get life insurance with PAD and diabetes?

Yes. Many seniors with both PAD and diabetes qualify for life insurance. Underwriters often focus on A1C levels, medication compliance, kidney function, and whether complications have developed.

Does PAD mean I have heart disease?

Not necessarily. However, PAD and heart disease often share the same underlying cause: atherosclerosis. Because of this connection, insurance companies frequently evaluate both conditions together.

Can you be declined because of Peripheral Artery Disease?

Yes. Severe PAD involving amputations, recent strokes, advanced cardiovascular disease, or ongoing complications may result in a decline. However, alternative coverage options are often available.

How much life insurance can I get with PAD?

Coverage amounts vary based on age, health history, and policy type. Some applicants qualify for $25,000 final expense policies, while others qualify for several hundred thousand dollars in traditional coverage.

Is PAD considered a serious medical condition by life insurance companies?

PAD is generally viewed as a significant cardiovascular risk factor because it may indicate plaque buildup throughout the body. However, insurance companies place substantial emphasis on stability, treatment success, and overall health.

Can I get life insurance if I have PAD and a history of heart attack?

Yes. Many applicants with both PAD and previous heart attacks qualify for coverage. Insurance companies typically evaluate how long ago the heart attack occurred, recovery progress, and current cardiovascular health.

Can I Get Life Insurance If I Have PAD in Both Legs?

Yes. Insurance companies focus less on the location of PAD and more on its severity, treatment history, symptoms, and overall cardiovascular health. Many seniors with PAD affecting both legs still qualify for life insurance coverage.

Ready to Explore Your Options?

Many seniors are surprised to learn that Peripheral Artery Disease does not automatically prevent them from obtaining life insurance.

Even if you have:

- Diabetes

- Coronary artery disease

- Heart stents

- Previous stroke

- Kidney disease

- High blood pressure

- Multiple cardiovascular conditions

there may still be several coverage options available.

Because underwriting guidelines vary significantly from one company to another, comparing multiple insurers often produces better approval opportunities and more competitive rates.

Speaking with an independent life insurance agent can help you understand your options before submitting an application and potentially improve your chances of finding the right policy for your situation.

Bottom Line: You Have Options

Peripheral Artery Disease can make life insurance more challenging, but it does not automatically prevent approval.

Many seniors with PAD successfully qualify for traditional life insurance, simplified issue coverage, final expense insurance, and guaranteed issue policies every year.

The most important factors are the severity of the condition, overall cardiovascular health, smoking history, and whether other medical conditions are present.

By understanding how insurance companies evaluate PAD and working with carriers that are comfortable underwriting cardiovascular risks, many seniors discover they have more options than they expected.

Whether you need coverage to protect your family, cover final expenses, or leave a financial legacy, there may be a life insurance solution that fits your needs.